AUSSIE BONDS: Slightly Stronger, PPI Beats, Trump In China, AU Consumer Inf Exp

ACGBs (YM +2.0 & XM +1.0) are stronger after US tsys finished Wednesday's session little changed but...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

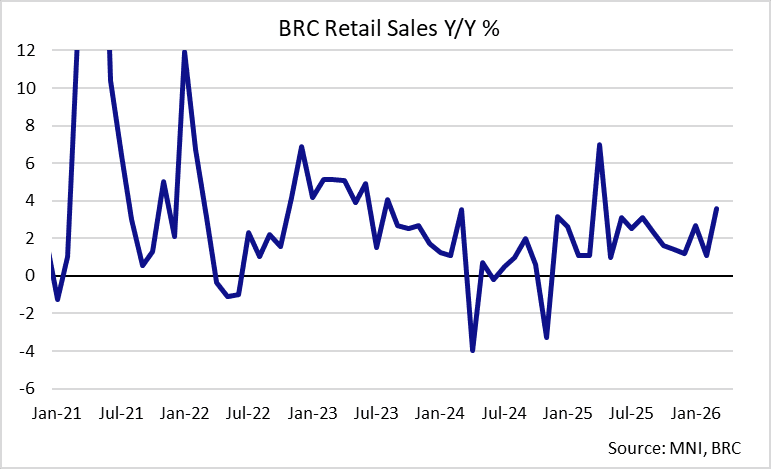

MNI: UK MAR BRC TOTAL RETAIL SALES 3.6% Y/Y (1.1% FEB)

- MNI: UK MAR BRC TOTAL RETAIL SALES 3.6% Y/Y (1.1% FEB)

UK DATA: Easter Timing Boosts BRC Retail Sales; Hard to Take Signal for ONS Data

BRC retail sales growth rose to 3.6% Y/Y in March (1.1% Feb, 2.7% Jan). Although the figure is the strongest since last April, it is distorted by the Easter weekend falling partly in March's reporting period this year (vs entirely in April last year). This follows similar moves in the BRC's footfall data (released last Friday, our write up here), and both are hard to interpret without waiting for April data.

- The reporting period covers the five weeks 1 Mar - 4 Apr 2026, meaning it includes the Easter weekend up to just before Easter Sunday, whereas last year Easter fell into April's reporting period. Note that ONS retail sales data (due 24 Apr) uses the same reporting period, although it will be seasonally adjusted for Easter (with some concerns about its effectiveness) and the M/M figures are more closely watched there.

- Back to the BRC release, the headline Y/Y growth is the strongest since April last year, where it's likely that Easter also provided a significant boost for around 7% Y/Y total sales growth - meaning it wouldn't be surprising to see a sharp reversal lower in next month's data, particularly if consumers remain cautious.

- On cost pressures and consumer sentiment, the press release comments: "The conflict in the Middle East is having an immediate impact on costs with petrol prices up by around 18% at the pump compared to before the conflict began. Expectations are that the conflict will continue to increase cost pressures, with rising risks to heating bills, food prices and interest rates."

- "As a result, shopper confidence has dropped to the lowest level since 2023. While occasions such as Mother’s Day and Eid provided moments of celebration, they were not enough to offset growing shopper concerns about rising costs."

- Looking at the details, food sales jumped 6.8% Y/Y (2.9% Feb, 3.8% Jan), as an "early Easter provided a much-needed boost". This jump was also helped by elevated food inflation (as in previous releases): "Food and drink continue to drive monthly retail sales growth, with inflation a key factor".

- Non-food sales rose 0.9% Y/Y (-0.4% Feb, 1.7% Jan), with mixed underlying moves: "demand was robust for computers, toys, and homeware, but clothing and footwear continued to struggle. The disruption to international travel caused by the Middle East conflict also hit sales of travel-related goods."

AUSSIE BONDS: Futures Follow US Lead Higher, Hauser Says Inflation Too High

Aussie bond futures are tracking higher, following the positive US Tsy futures lead from overnight. We are +4-4.5bps firmer across 3yr and 10yr futures. 10yr are back around 95.00, with upside focus likely around the 50-day EMA, near 95.09, while April to date lows rest at 94.92. 3yr futures sit at 95.33, also within recent ranges for April. For this benchmark, the 50-day EMA resistance point is near 95.50, while April lows rest at 95.24.

- The risk mood was better in US Monday trade, aided by US/Iran hopes, with oil prices finishing well off Monday highs, while US equities rose. Trump comments around scope for a US-Iran deal came even as the naval blockade came into affect, while BBG reports this morning further talks may take place between US and Iran ahead of next week (when the two week cease fire from Apr 7 is scheduled to end).

- Cash ACGB yields sit around 4bps lower for the benchmarks. The 3yr is back to 4.65%, the 10yr to 4.97%.

- The RBA's Hauser is participating in a Fireside chat in NY currently. He has noted that inflation is too high and that the central bank doesn't want medium term inflation expectations to pick up. They are also watching the demand side though, particularly consumption, which is growing from a low base, but not in recession territory.

- Today the April Westpac consumer confidence is published and is likely to decline given the sharp rise in petrol prices since the start of March and the RBA’s second straight rate hike. It has only broken above the breakeven 100-mark once in the last four years - November 2025.

- The March NAB business survey is also out today and is also likely to post a decline given higher costs and elevated uncertainty. The survey’s price/cost and employment components could provide important early information on how businesses are responding to recent events.