AUSSIE BONDS: Slightly Richer With US Tsys, HH Spending data In Focus

ACGBs (YM +1.5 & XM +2.0) are slightly stronger after a modest rally by US tsys on Wednesday following a flurry of economic data.

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November, whilst the October increase was revised up from 42k to 47k.

- Charles Gasparino at Fox Business reports on X that there is a 'last-ditch' effort by Wall Street and corporate America insiders to caution President Donald Trump against nominating National Economic Council Director Kevin Hassett as Federal Reserve Chair.

- Cash ACGBs are 2-3bps richer with the AU-US 10-year yield differential at +56bps.

- The bills strip is flat to +2 across contracts.

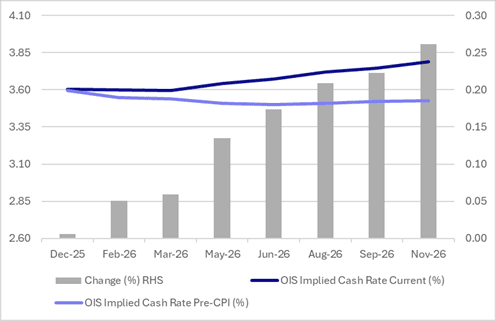

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 0% probability. Notably, the market has shifted to giving an 89% probability to a 25bps by December 2026.

- Today, the local calendar will see Trade Balance and Household Spending data.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong CPI

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.345 @ 16:07 GMT Nov 3

- SUP 1: 96.280 - Low May 15 (cont.)

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Having bounced well on the back of the mild US CPI print, Aussie 3-yr futures reversed course Wednesday on strong domestic inflation data containing RBA cut pricing through 2026. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 96.280 as the next major support.

AUSSIE BONDS: Slightly Cheaper Ahead Of RBA Policy Decision

ACGBs (YM x-1.5 & XM -1.5) are weaker after cash US tsys finish moderately weaker.

- Today is RBA Policy Decision day, with the Board likely to remain highly data-dependent and cautious given inflation's renewed shift higher and the emerging domestic recovery, but easing labour market conditions. (see MNI RBA Preview here)

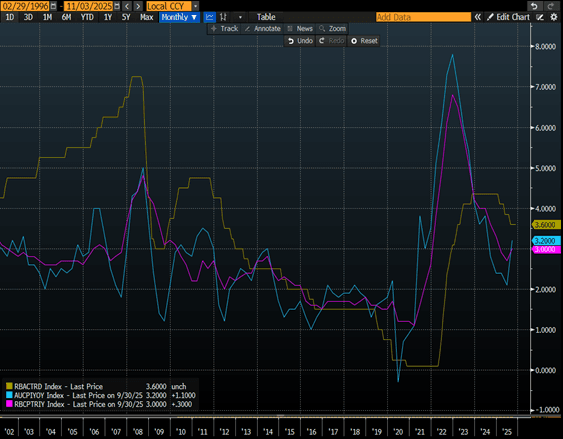

- Paul Bloxham (HSBC) argues that Australia’s labour market still appears tight, as inflation is rising even with unemployment at 4.3%. He questions whether the RBA may have already eased policy too much. Consequently, he does not expect further rate cuts and believes the next move in interest rates is more likely to be an increase. – AFR via BBG

- These thoughts appear consistent with the attached chart, which highlights that rising annual inflation tends to end easing cycles.

- Cash ACGBs are 1bp cheaper.

- The bills strip is flat to -2 across contracts.

- RBA-dated OIS pricing implies almost no chance of an easing, with just a 3% probability assigned. As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.

Bloomberg Finance LP

GOLD: Monday’s Fed Speak Keeps December Cut Open, Gold Range Traded

After an initial dip, gold looked through China’s decision to remove the retail tax exemption on gold and trended gradually higher before settling around $4010. It reached $4030.48/oz following disappointing US manufacturing ISM data. It printed at 48.7 in October down from 49.1 and below consensus. Bullion finished flat at $4001.42 as the US dollar was slightly stronger and yields higher.

- Fed Governor Cook said that she supported the October cut as she believed the risks to the labour market outweighed inflation. She also said the Fed is “not on a predetermined path … every meeting, including December’s, is a live meeting”.

- SF Fed President Daly also noted that the FOMC should “keep an open mind” about easing next month and that 50bp of cumulative easing would leave the Fed “better positioned”. Monetary easing is supportive of non-interest bearing gold.

- Gold fell to $3962.59 early in Monday’s trading, holding above initial support at $3886.6, 28 October low. At the other end, it was unable to return to $4046.2, 31 October high. Technicals suggest it remains in a corrective phase which has allowed an overbought condition to unwind. A break of the 50-day EMA at $3859.1 would strengthen a short-term bear theme.

- Silver continued its correction on Monday falling 1.3% to $48.078, close to the intraday low of $48.024. It reached $49.107 early in the European session. The trend in the metal remains bullish and declines considered corrective. A break of the 50-day EMA at $45.963 would signal scope for a deeper retracement.