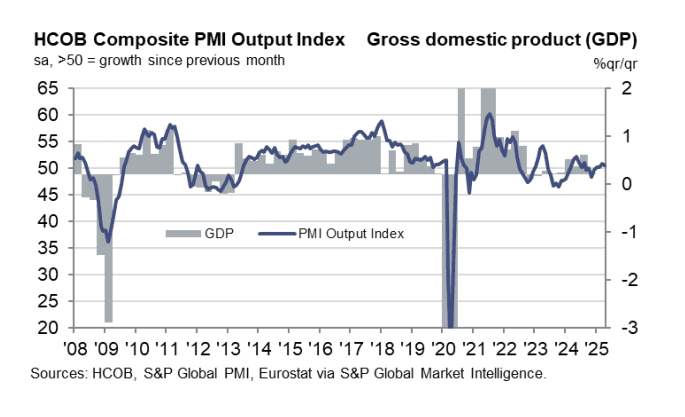

EUROZONE DATA: Similar Themes In April Services PMI To Manufacturing

The Eurozone April services PMI saw very similar themes to last week’s manufacturing PMI round: Spain weaker than expected, Italy stronger than expected and upward revisions in France/Germany. That sees the Eurozone-wide PMI inch back into expansionary territory to 50.1 (vs 49.7 flash, 51.0 prior). There has been little net impact on ECB implied rates, with OIS still pricing ~60bps of easing through year-end.

- Note: Little lasting reaction to headlines that incoming German Chancellor Merz failed to reach a majority in an initial vote to swear himself in as head of government. The base case is Merz will still become Chancellor.

- We estimate the services PMI excluding France and Germany at 53.2 (vs 53.4 prior), while the Germany/France measure fell back to 48.3 (vs 49.6 prior).

- The composite PMI was 50.4, above the 50.1 flash reading and 50.9 prior.

Key notes from the EZ-wide release:

- “A third successive monthly drop in the level of incoming new work was registered during April. The rate of decrease in new orders was the quickest since last November, albeit mild overall. A marginal reduction in new export business was also posted”.

- “Eurozone services companies made additional inroads into their incomplete business during the latest survey period, extending the depletion trend to exactly a year. That said, despite evidence of reduced capacity pressures, employment rose at a modest rate”.

- “Input costs increased at a sharp pace in April, although the rate of inflation cooled to a five-month low. Prices charged for the provision of euro area services meanwhile rose at the weakest pace since October 2024”.

- “Lastly, there was another deterioration in business confidence, marking a fourth straight month of easing expectations.”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (M5) Strong S/T Bounce

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.915 - High Apr 4

- PRICE: 95.860 @ 16:42 GMT Apr 04

- SUP 1: 95.420/95.300 - Low Feb 13 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.640 - 1.0% 10-dma envelope

Aussie 10-yr futures extended a recent strong bounce through to the Friday close, putting prices through the top end of the recent range. The confirmed breach of 95.851, the Dec 11 high on the continuation contract, reinstates a bull cycle and focuses attention on resistance at 96.207, a Fibonacci retracement point. A stronger bearish theme would expose 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

USDCAD TECHS: Bearish Structure

- RES 4: 1.4452/4543 High Mar 13 / 4 and a bull trigger

- RES 3: 1.4415 High Apr 1

- RES 2: 1.4308 50-day EMA

- RES 1: 1.4242 High Apr 4

- PRICE: 1.4196 @ 17:10 BST Apr 4

- SUP 1: 1.4028 Low Apr 3

- SUP 2: 1.3986 Low Dec 2 ‘24

- SUP 3: 1.3944 61.8% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 4: 1.3894 Low Nov 11 ‘24

USDCAD rallied Friday, but remains lower on the week after Thursday’s downleg. The move down has confirmed a clear reversal of the bull cycle between Sep 25 ‘24 and Feb 3. Price is through a key support at 1.4151, the Feb 14 low. This signals scope for an extension towards 1.3944, a Fibonacci retracement. On the upside, key short-term resistance is seen at 1.4308, the 50-day EMA.

CANADA DATA: Unexpected Jobs Contraction Boosts Implied April BOC Cut Chances

Canadian employment unexpectedly contracted in March, falling by the most since January 2022 at -32.6k (+10.0k expected, +1.1k prior) in a sign that the trade war with the US is spilling over increasingly into the "hard" data. The unemployment rate ticked up 0.1pp to 6.7%, in line with expectations and below the November 6.9% high, though unrounded it rose from 6.55% to 6.71% - the largest increase since November.

- The drop in employment was largely due to a 62.0k drop in full-time positions (after -19.7k, the 2nd straight drop), with part-time up for the 4th consecutive month at 29.5k (after 20.8k prior) - that mix is clearly indicative of hiring uncertainty among firms.

- The monthly full-time drop was the 2nd largest since the pandemic lows in the labour market (April 2020). Goods producing jobs fell by 12k (2nd consecutive decline), while services shed 21k (wholesale/retail trade and Information, culture and recreation led losses).

- The participation rate dipped 0.1pp to 65.2%.

- Wages were soft, dropping 0.2% M/M for the first drop since November, with the Y/Y rate slipping to 3.6% from 3.8% prior. The rise in permanent employees' wages of 3.5% Y/Y was well below the 4.1% expected (4.0% prior).

- Market-implied probability of an April BOC rate cut rose to as high as 68% after the data before settling the day at around 55%. That compares to 40% prior to Wednesday's US tariffs announcement.