AUSSIE BONDS: Sharply Cheaper, Cut Chances Pared But Remain, How Much Longer?

ACGBs (YM -11.5 & XM -6.5) are sharply weaker after the release of stronger-than-expected October employment data.

- October labour market data normalised with the unemployment rate returning to 4.3%, where it was before September’s jump to 4.5%. Employment rose 42.2k after 12.8k with the growth all in full-time positions. The participation rate was stable at 67.0%. It is important to remember that the data are volatile and that as RBA Governor Bullock says to look at the 3-month averages.

- "Sean Crick, ABS head of labour statistics, said: ‘The unemployment rate dropped to 4.3 per cent after rising to 4.5 per cent in September. The October unemployment rate is in line with June, July, and August 2025.”

- Cash US tsys are little changed in today’s Asia-Pac session.

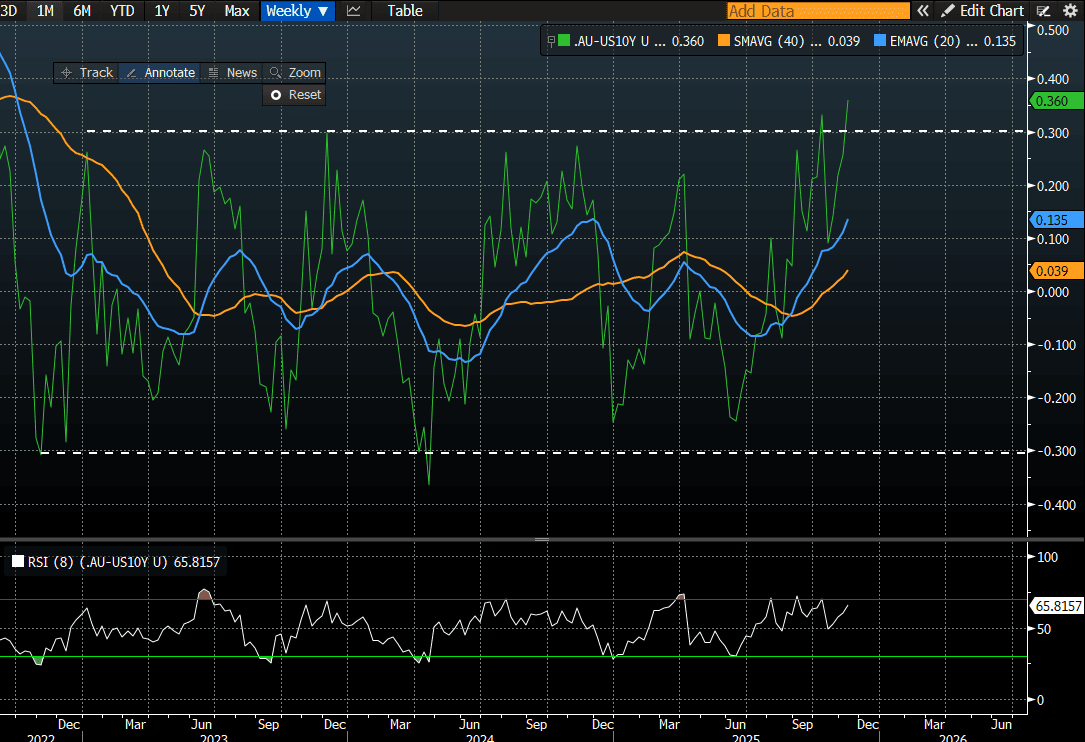

- Cash ACGBs are 7-12bps cheaper than pre-data levels, with the AU-US 10-year yield differential at +35bps. At this level, the differential is through the top of its well-defined +/- 30bps trading range (see chart).

- Swap rates are 6-11bps higher, with a flatter curve.

- The bills strip has shunted cheaper and steeper, with pricing -4 to -15.

- RBA-dated OIS pricing shows a 25bp rate cut in December at a 2% probability (9% pre-data), with a cumulative 6bps of easing priced (- 16bps pre-data) by mid-2026.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Steeper Curves As Mkts Re-open, Focus Remains On Politics

Cash JGB curves are biased steeper as markets re-open from the long weekend. Focus will remain on domestic politics, fresh uncertainty risks driving the curve higher, as speculation continues around how LDP leader Takaichi will form a governing coalition (or whether she will be elected PM). Such a backdrop pushes back BoJ hike timing all else equal, (aiding a steeper curve), but may also make it difficult to pass any meaningful fiscal stimulus.

- JGB futures sit off recent highs, last 136.10, +.20 versus settlement levels. The better risk tone, along with US Tsy futures maintaining a modest offered tone is weighing on JGBs. US Tsy yields have re-opened with a firmer bias and a steeper curve as well, the 10yr yield up 3bps to 4.06%.

- In the cash JGB space, the bias is for a steeper curve. The softest part in yield terms is the 3y to 7y, down around 1-2bps, led by the 7yr. The 10yr is down a touch to 1.68%. The 20-40yr tenors are firmer, led by the 30yr (+4bps to 3.245%).

- The 2/30s curve is steeper by +5bps to +233bps. Focus on the upside will be the +240bps region, which we haven't been able to sustain in recent months.

OIL: : Crude Continues Recovery Watching Supply/Demand Outlook Key Though

After sinking around 5% on Friday driven by energy demand concerns in the face of renewed US-China trade tensions, oil prices recovered slightly on Monday following President Trump taking a step back and the associated improvement in risk appetite. There had also been a Ukrainian strike on a major Russian refinery on the weekend. The market watches these developments closely as they risk refined product supplies and may have contributed to an increase in Russian crude exports.

- WTI rose 1.1% to $59.56/bbl after reaching $60.17 and has started Tuesday around $59.76. Moves above $60 were brief. It is down 4.4% this month. Initial support is at $58.22, 10 October low, with resistance at $62.75, 50-day EMA.

- Brent is currently around $63.52/bbl after increasing 1.0% to $63.39. It was unable to break through $64 yesterday reaching $63.95. The benchmark is 4% lower in October with a bearish threat remaining. Initial support is at $62.00, 10 October low, while resistance is $66.31, 50-day EMA.

- OPEC published its October report on Monday keeping its oil demand forecasts unchanged at up 1.3mbd in 2025 and 1.4mbd in 2026. The group tends to be more optimistic than others. The IEA’s report is out Tuesday and it tends to be more cautious with it expecting a market surplus in 2026 for some time.

- Non-OPEC supply is forecast to rise 800kbd in 2025 and 600kbd in 2026 driven by US, Canada, Brazil & Argentina. Output from OPEC+ rose 630kbd in September according to the group’s report. It agreed to increase production by 137kbd in both October and November but most members are now facing capacity constraints which may impact its ability to lift supply and gain market share, except for Saudi Arabia.

JGBS: Focus On Whether Futures Bounce Can Be Sustained As Onshore Returns

JGB futures finished up at 136.42, +.52 versus settlement levels. Prices surged Monday, in sympathy with global bond markets, helping the price rally toward last week’s high. Sentiment was buoyed by the flight to bond markets, although with equity sentiment stabilizing focus will be on whether this is sustained. We will need to challenge resistance before signaling a broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high. The latest sell-off, however, resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection.

- Cash JGBs finished up last Friday at 1.69% for the 10yr (just off cycle highs), while the 2/30s curve was at +228bps, slightly steeper.

- Japan markets return today. Politics remains a focus point, with opposition parties set to meet today to discuss the collapse of the governing coalition last week. These meetings could help determine whether Takaichi goes ahead with a minority government, or looks to bring forward elections. Her odds of becoming the next PM have slid to 77, per Polymarket (down from post LDP leadership election highs near 100).

- Locally on the data front Sep money stock figures, not typically a market mover.

- Note tomorrow we have a 20yr debt auction.