LNG: Santos Expects First Production at Darwin LNG in Coming Weeks

Oct-17 10:47

Santos said on Oct. 16 that it had achieved first gas from the Barossa LNG project into the export pipeline, with first production at Australia’s Darwin LNG expected in the coming weeks, Platts reported.

- The offshore gas and condensate project will supply new feedstock to the Darwin facility in Australia’s Northern Territory.

- Barossa faced a two-week unplanned shutdown in September due to safety system issues on the BW Opal FPSO but has since resumed operations. The project holds an updated environmental licence, and first LNG cargo remains on track for Q4 2025.

- Santos reported quarterly production of 21.3m boe, bringing year-to-date output to 65.4m boe.

- PNG LNG maintained an 8.6m mtpa run rate, while GLNG output averaged 711 TJ/day.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

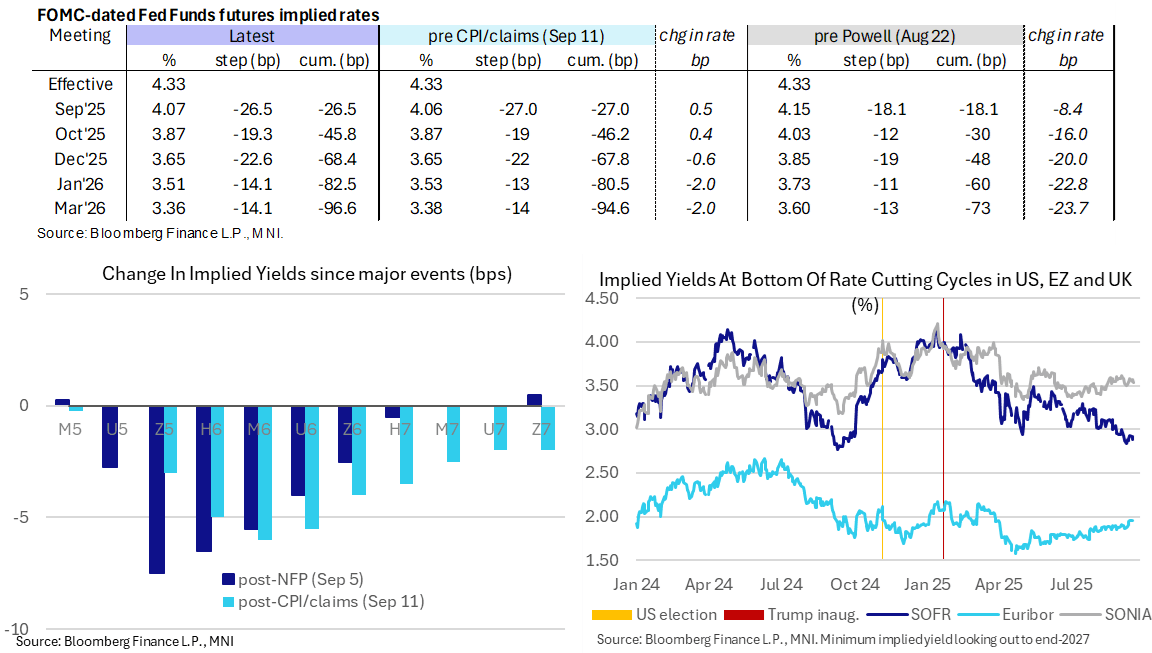

STIR: Fed Cut Pricing For Today Inches Higher But Still <10% Odds Of 50bp Cut

Sep-17 10:37

- Fed Funds implied rates have dipped 0.5bp for today’s decision in response to aforementioned flow (Ongoing trade in FFV5 with paper paying 95.945 on 7K, taken bid over), but it still points to less than 10% odds of a 50bp cut.

- It holds the broad paring in 50bp cut expectations having increased to ~20% after payrolls earlier in the month.

- Cumulative cuts from 4.33% effective: 26.5bp for today, 46bp Oct, 68.5bp Dec, 82.5bp Jan and 96.5bp Mar.

- SOFR futures are essentially unchanged on the day.

- That includes the implied terminal yield of 2.88% (SFRH7), eyeing 145bp of cuts ahead including fully priced cut. It’s within ranges for the past two weeks, including dovish extremes of ~150bp of cuts after payrolls.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Sep2025_With_Analysts_c3eababfe1.pdf

BUNDS: Looking to close the Gap

Sep-17 10:37

- The German curves are tilted to the flatter side in early trade, but the Schatz edges through the very tight intraday high with 5k lifted.

- This is underpinning Bund, albeit still just short of the earlier printed high.

- Initial area of interest in Bund, not a Tech level, is the 129.13 gap.

OUTLOOK: Price Signal Summary - Gold Bulls Remain In The Driver's Seat

Sep-17 10:31

- On the commodity front, Gold remains in a clear bull cycle and the yellow metal is trading closer to its recent highs. A fresh all-time high, once again this week, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3705.2, a 1.382 projection of the May 15 - Jun 16 - 30 price swing. Initial firm support lies at $3547.7, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible recent reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would open $57.71, the May 30 low.

Related bullets

Related by topic

Energy Data

G3

G7

G10

Natgas

Asia LNG

Asia

Gas Positioning

Australia