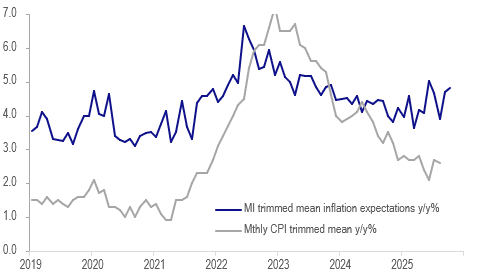

AUSTRALIA DATA: Rising Inflation Expectations Add To Rate Cut Uncertainty

Melbourne Institute consumer inflation expectations continued to trend higher in October rising 0.1pp to 4.8%, the highest in almost two years. This is consistent with the RBA’s more cautionary tone regarding the inflation outlook and Westpac saying that higher Q3 inflation prints weighed on October consumer confidence. Households appear to have ignored lower petrol prices in the first week of October. Q3 CPI is released on 29 October and is likely to shape sentiment and the rate outlook. The AUD OIS market now has only around a 40% chance of a rate cut in November.

Australia trimmed mean inflation y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYZ5 is trading 113-18, up 0-00+ from its close.

- The US 2-year yield opens around 3.488%, down 0.03 from its close.

- The US 10-year yield opens around 4.042%, down 0.01 from its close.

- MNI US DATA: NY Fed Consumer Survey: Inflation Expectations Looking Stubborn. The New York Fed's Survey of Consumer Expectations leaned in a stag-flationary direction in August, showing both an uptick in short-term inflation expectations and increasing pessimism on the labor market front. Overall the deterioration in the labor market outlook is likely to be the main takeaway from the FOMC going into its meeting next week, stubborn inflation expectations are unlikely to be ignored, illustrative of the Fed's current policy dilemma.

- Upcoming issuance: September’s issuance schedule is set to see $315B in nominal Treasury coupon sales (unch from the equivalent month in the previous quarter), in addition to $19B in 10Y TIPS (up $1B from prior) and $28B FRN (unch) for a total of $362B.

- Sales for the month start today with $58B of 3Y Note, Wednesday Sep 10 with $39B of 10Y Note reopen, and Thursday Sep 11 with $22B of 30Y Bond reopen.

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone between 4.15%-4.20%. First target the 4.00% zone then the 3.80% area.

- Data/Events: NFIB Small Business Optimism, Prelim. Benchmark Payrolls Revision

JGBS: Futures Higher, But JGB Curve Remains Steep, Bucking US Trend

JGB futures got to 138.17, +.13 versus settlement levels post the Tokyo close on Monday. The general positive tone to global futures helped sentiment in this space, although JGB futures remain off Friday highs from last week.

- From a technical standpoint, a bear threat in JGB futures remains present despite the recovery of recent lows, including the rally into the Friday close. A resumption of weakness would signal scope for an extension towards 136.57, a Fibonacci projection. Initial short-term resistance is 139.05, the Aug 4 high. A breach would be a positive development for bulls.

- Until we get greater clarity around the local political outlook, JGBs may lag US Tsy bond gains. The US-JP 10yr government bond yield spread is tracking lower, last at +247bps (although some catch up from 10yr JGB yields may be seen today). We were around +263bps at the end of Aug.

- Via BBG: " Sanae Takaichi, who is polling at 23% nationally according to a Nikkei survey but has weaker backing within the Liberal Democratic Party" is in favor fiscal and monetary policy easing, while "Shinjiro Koizumi is polling 22% nationally, but is the clear party favorite with support at 32% among LDP members. " (Koizumi sits more hawkish relative to Takaichi).

- In the cash JGB space, the 10yr yield finished up at 1.57% yesterday, while the 2/30s JGB curve finished up at +245bps, around the May highs.

- Todya on the data front, Aug money stock figures are out, along with Aug machine tool orders.

NEW ZEALAND: Q2 Data Suggesting Weak GDP Outcome

Q2 NZ business sales values rose 2.1% q/q with profits up 4.2%. Salaries and wages rose only 1.2% q/q. Manufacturing volumes fell 2.9% q/q after rising 2.4%. Q2 GDP is released on September 18 and the RBNZ is forecasting it to fall 0.3% q/q. Data has shown weak building, goods exports and manufacturing volumes. The RBNZ is expected to cut rates at its October and November meetings.

- 8 of the 14 industries recorded a rise in sales in Q2 with electricity & gas jumping 16% q/q, mining up 2.5% and information media & telecoms up 3.8% but manufacturing down 3%.

- 9 of the 13 manufacturing components posted a quarterly decline in volumes in Q2 suggesting the weakness was broad-based.

- On the positive side, Q2 real retail sales rose 0.5% q/q but merchandise export volumes fell 3.7% q/q and building volumes -1.8% q/q. Manufacturing inventory volumes rose 0.8% y/y.