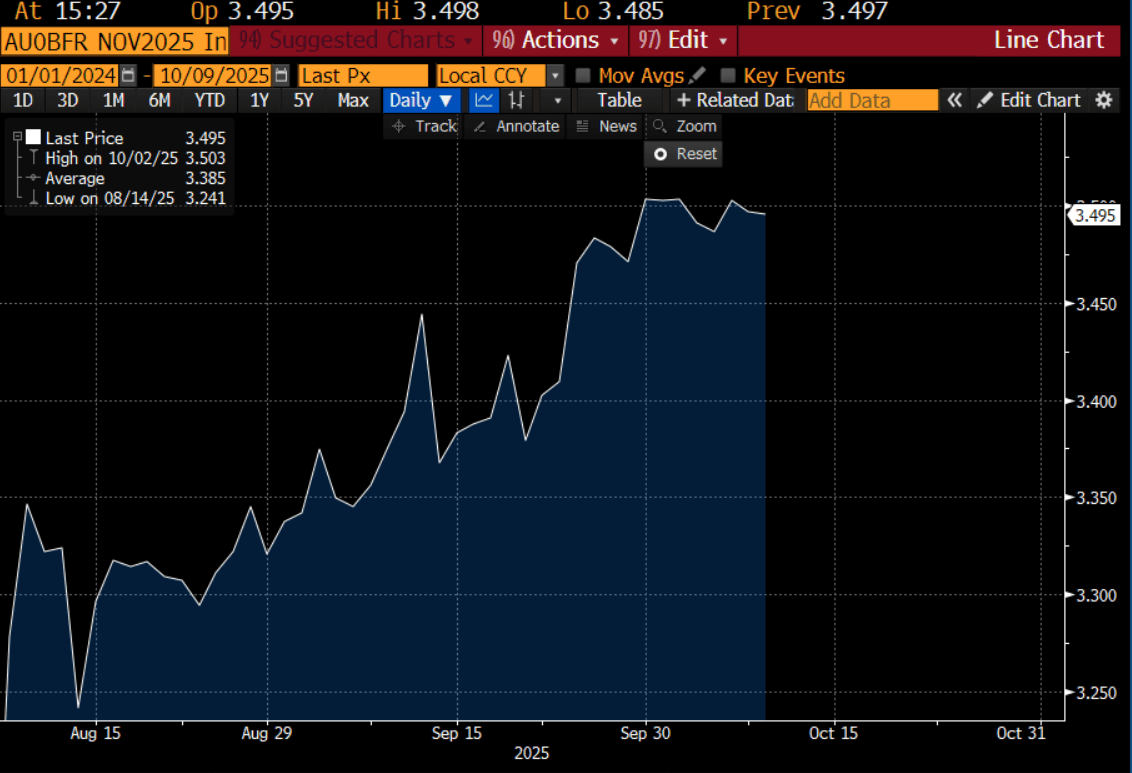

AUSSIE BONDS: Richer Despite Higher Inflation Exp, RBA Testimony Tomorrow

ACGBs (YM +1.5 & XM +3.0) are stronger and hovering near session bests.

- This comes even though Melbourne Institute consumer inflation expectations continued to trend higher in October rising 0.1pp to 4.8%, the highest in almost two years. This is consistent with the RBA’s more cautionary tone regarding the inflation outlook and Westpac saying that higher Q3 inflation prints weighed on October consumer confidence. Households appear to have ignored lower petrol prices in the first week of October. Q3 CPI is released on 29 October and is likely to shape sentiment and the rate outlook.

- RBA-dated OIS pricing continues to assign a 40% probability to a 25bp rate cut in November, with a total of 14bps of easing priced by year-end (See chart). Nevertheless, current pricing marks a notable shift from late September, when markets had fully priced a 25bp cut ahead of the August CPI release.

- Cash US tsys are little changed in today’s Asia-Pac session.

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +21bps. At 21bps, the differential remains near the top of the +/- 30bp range it has traded in since late 2022.

- The bills strip is little changed.

- Tomorrow, the local calendar will see an appearance before the Senate Economics Legislation Committee by RBA Governor Bullock and Assistant Governor Kent.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

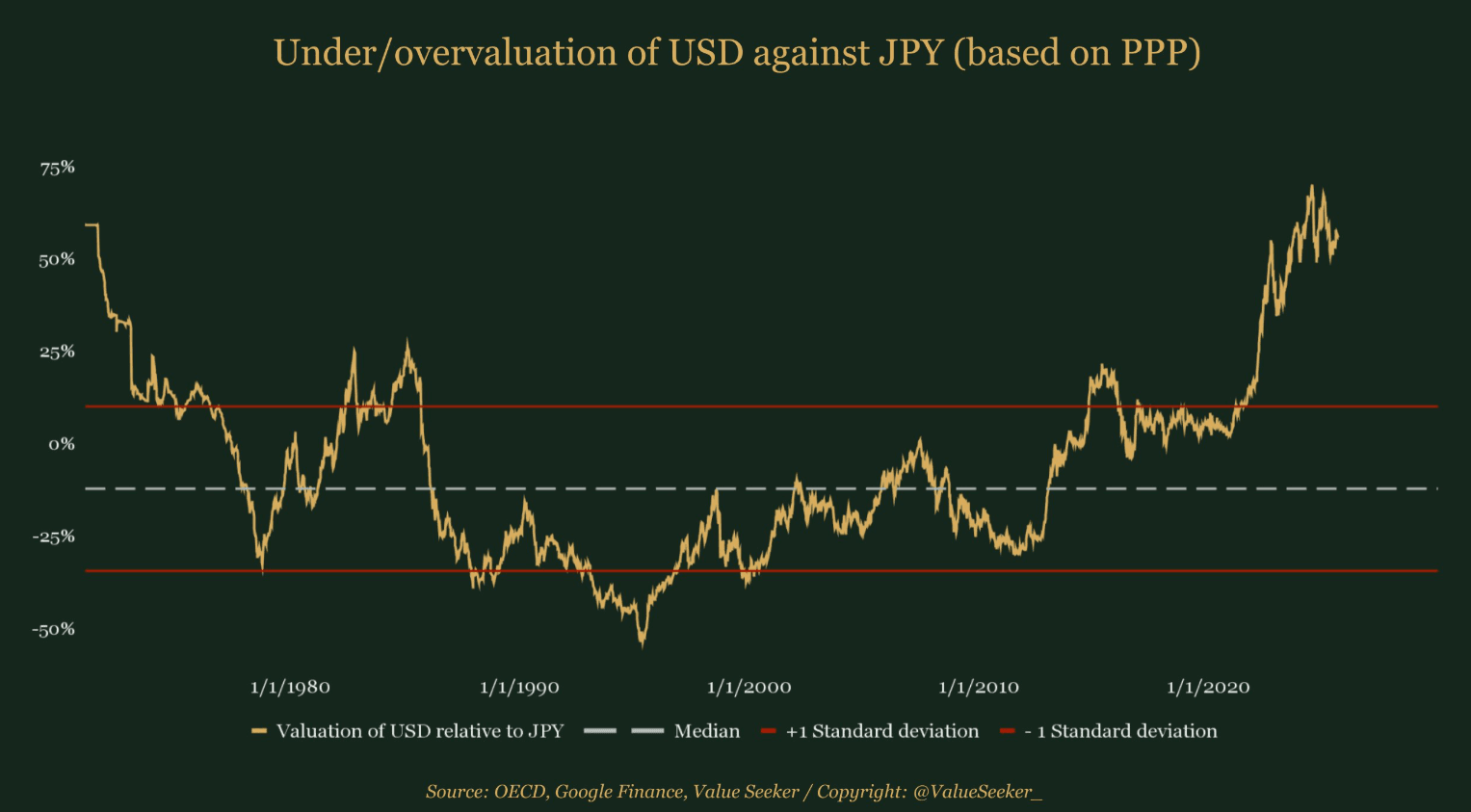

JPY: Asia Wrap - USD/JPY Drifts Lower After Filling In The Monday Morning Gap

The Asia-Pac USD/JPY range has been 147.16-147.58, Asia is currently trading around 147.20, -0.20%. USD/JPY could not hold onto the gains it made in early Asian trading yesterday and ended up filling in the gap. The support towards 146.00 comes back into view, it has been solid for most of July and August, can it continue to hold as the USD’s own support begins to look precarious. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so the inability for the price to extend yesterday would be disconcerting, a move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- Value Seeker on X: “The Japanese Yen remains highly undervalued relative to most currencies, including the US Dollar, which trades 50% (3 st. dev.) above its purchasing power parity against the Japanese currency.” See Graph Below.

- Bloomberg - “Japan’s Kono Says BOJ Needs to Hike Rate to Fix Yen, Inflation. The Bank of Japan should raise its benchmark rate to support the yen and curb inflation, Liberal Democratic Party lawmaker and former digital transformation minister Kono Taro said, as political uncertainty clouds the outlook for economic policy.”

- "KATO: MULL IMPACT OF TARIFFS, OPPOSITION VIEWS FOR ECO PACKAGE, PRICE RELIEF IS NEEDED TO PROTECT LOW-INCOME HOUSEHOLDS” - BBG

- "JAPAN LDP DECIDES TO HOLD 'FULL-SPEC' LEADERSHIP VOTE: NTV" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($931m), 147.50($521m).Upcoming Close Strikes : 145.75($1.12b Sept 11), 150.00($1.11b Sept 11) - BBG..

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +78427( Last +76761), leveraged funds though again used the dip to add a decent clip to their newly built short JPY position -66914(Last -52275). One of them is going to be wrong.

Fig 1 : JPY Undervaluation Vs USD(based on PPP)

Source: MNI - Market News/@ValueSeeker_/OECD

BONDS: NZGBS: Yields Up From Earlier Lows, Q2Data Points To Weak GDP

NZGB benchmark yields are up from earlier lows. The 2yr yield is now up close to 2bps, tracking back towards 2.95%. The 10yr NZGB yield is around 4.31%, still off 1.5bps. Both benchmarks remain close to recent lows. US Tsy yields have drifted a touch higher, led by the front end, which may have spilled over to NZ at the margins.

- The NZ 2/10s curve remains flatter last near +136.5bps. The NZ 2yr swap rate has edged up to 2.735%, against earlier lows near 2.705%, so mirroring the movement in NZGB front end yields.

- On the data front, Q2 NZ business sales values rose 2.1% q/q with profits up 4.2%. Salaries and wages rose only 1.2% q/q. Manufacturing volumes fell 2.9% q/q after rising 2.4%. Q2 GDP is released on September 18 and the RBNZ is forecasting it to fall 0.3% q/q. Data has shown weak building, goods exports and manufacturing volumes. The RBNZ is expected to cut rates at its October and November meetings.

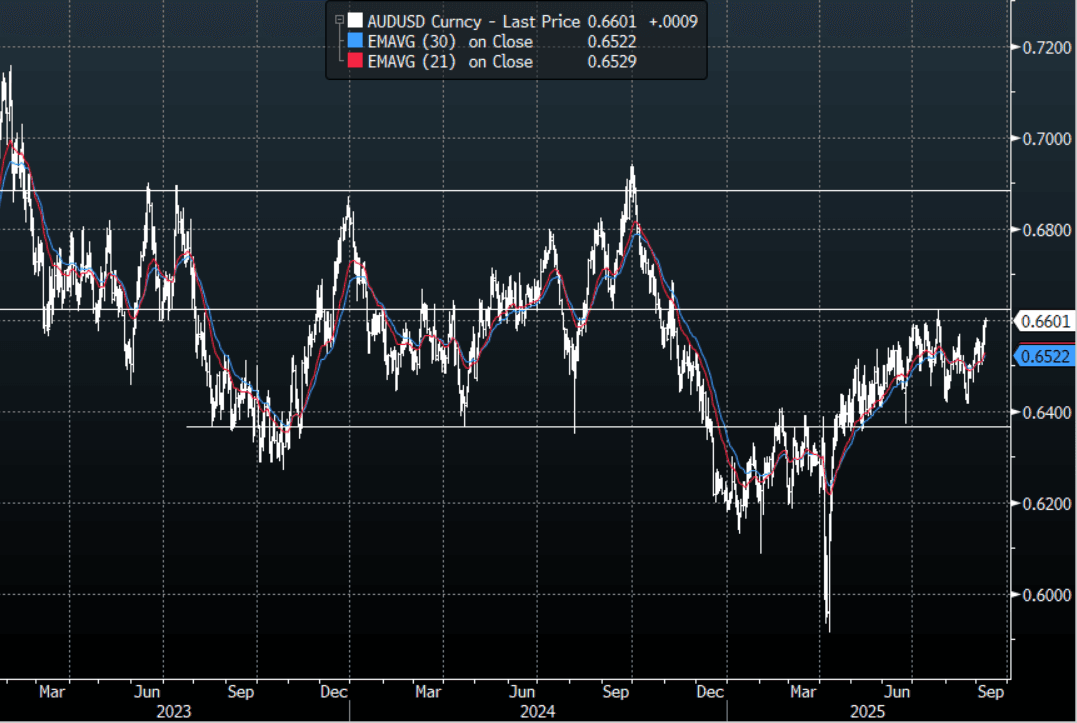

AUD: Asia Wrap - AUD/USD Probes Above 0.6600

The AUD/USD has had a range of 0.6588 - 0.6604 in the Asia- Pac session, it is currently trading around 0.6600, +0.12%. US rates extended lower again and the USD traded soft, the headwinds for the USD seem to be compounding which points to a potential look below its support. The AUD has drifted higher and is looking to test the top-end of its recent range. The AUD remains in its recent multi-month range of 0.6350-0.6650, should the USD break and extend lower we could potentially see the AUD break back above 0.6650. Should this occur it could provide the upward momentum to target levels back towards 0.6900/0.7000. Although still in the range the bias is for dips back to 0.6500 to be supported now.

- Growth Recovery Continued In Q3, August Costs/Prices Moderated. August NAB business confidence fell to +4 from +8 but conditions improved to +7 from +5. Both have improved in Q3 to date by around 3 points signaling that GDP growth should continue to recover. The price/cost components were lower in August with purchase cost and retail price increases at multi-year lows, which should reassure the RBA. However, the Q3 average of final product prices is still around where it was in H1 signaling some stabilisation in disinflation. Labour demand also appears to have steadied.

- Consumer Sentiment Weaker But Series Is Volatile: Westpac consumer sentiment fell 3.1% m/m to 95.4 in September after August’s robust +5.7% m/m to 98.5. It remains in pessimistic territory but above the 2025 average helped by 75bp of monetary easing and lower inflation.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6515(AUD429m), 0.6600(AUD420m). Upcoming Close Strikes : 0.6550(AUD777m Sept 10) - BBG

- CFTC Data last week shows Asset managers reduced their shorts for the first time in a while -66025(Last -78758), the Leveraged community though look to be rebuilding their own shorts after winding them down -11860(Last -6447).

- AUD/JPY - Asia-Pac range 97.12 - 97.28, Asia is trading around 97.20. The pair topped out towards 97.50 but has held onto most of its gains on the gap higher yesterday unlike USD/JPY. A sustained break above 97.50/98.00 is needed to reignite the upward trend.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P