AUSSIE BONDS: Richer But AU-US 10Y Diff At Range Top Ahead Of Jobs Data

Nov-12 04:10

ACGBs (YM +1.5 & XM +2.0) are modestly stronger despite today’s much stronger-than-expected home loan data.

- The recovery in home lending began in Q2 after the RBA began easing in February and the 75bp to August appears to have contributed to the sharp rise.

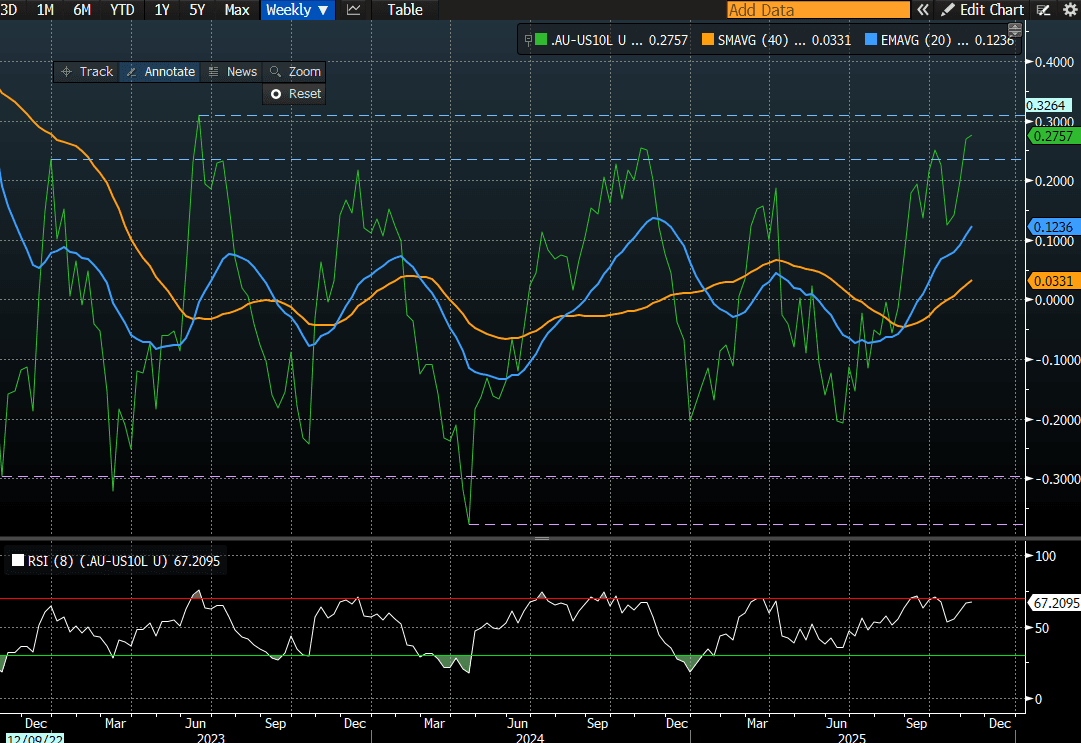

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +29bps. At this level, investors may be tempted to position for a narrowing in the differential, as it sits near the top of its well-defined ±30bps trading range (see chart).

- However, such trades carry meaningful risk ahead of tomorrow’s October employment data. The unemployment rate rose 0.2pp to 4.5% in September.

- The unemployment rate is widely expected to normalise somewhat at 4.4% but there are a few economists who expect it to stay at 4.5% or fall back to 4.3%.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 9% probability, with a cumulative 16bps of easing priced by mid-2026.

- The AOFM plans to sell A$800mn of the 1.75% 21 November 2032 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: As Trade War Intensifies, Equities Suffer (amended)

Oct-13 04:08

- With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington.

- Unsurprisingly the KOSPI followed China's lead and is down -1.6%. As always with market, context is key and the KPSPI hit new all time highs recently and any move lower is as much driven by the locking in of profits by investors, rather than a sea change in sentiment at this stage.

- With the JCI doing very little, South East Asia's other major bourse the FTSE Malay KLCI is down just over -0.50%. It has consistently underperformed the run up in equities in the recent period of strength and naturally its downside seems less pronounced.

- The focus on China arguably gives India a short respite having been in the sights of the US recently. The NIFTY 50 delivered a positive though modest week of gains last week, yet is giving some of those gains back in Monday morning trade.

ASIA STOCKS: As Trade War Intesifies, Equities Suffer

Oct-13 04:07

- With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington.

- Unsurprisingly the KOSPI followed China's lead and is down -1.6%. As always with market, context is key and the KPSPI hit new all time highs recently and any move lower is as much driven by the locking in of profits by investors, rather than a sea change in sentiment at this stage.

- With the JCI doing very little, South East Asia's other major bourse the FTSE Malay KLCI is down just over -0.50%. It has consistently underperformed the run up in equities in the recent period of strength and naturally its downside seems less pronounced.

- The focus on China arguably gives India a short respite having been in the sights of the US recently. The NIFTY 50 delivered a positive though modest week of gains last week, yet is giving some of those gains back in Monday morning trade.

CHINA: September Exports Surge (Ex US) as Trade War Intensifies

Oct-13 03:18

- The moderation of exports in August was short-lived as September's numbers jumped +8.3% YoY, beating expectations and much stronger than the month prior.

- According to BBG estimates, the decline in exports to the US was significant, down -27% YoY. This points to the growth of demand from non US markets, arguably weakening the US's position in a trade war. Exports to Africa, India and other Asian nations are soaring with the latter back to pre-COVID levels.

- US President Donald Trump had threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping, in a lengthy statement on Truth Social, citing a letter from Beijing which he claims lays out new rare earth export control measures.

- The new Chinese rare earth export control measures are scheduled to take effect on December 1. Starting November 8, Beijing will also restrict exports of equipment needed to manufacture batteries for electric cars in a bid to protect the competitiveness of Chinese autos, per The New York Times.

- Imports climbed +7.4% in September for it's largest monthly expansion since April 2024. Despite being a crude indicator for domestic demand, the result nevertheless comes a an invaluable time as the US rhetoric ramps up.

- Along with the decline in exports to the US, imports from the US declined -16.1%, widening the trade surplus with the US to $22.bn.

- Whilst this data captures a period before the weekend's escalation it may slightly strengthen Beijing's position in negotiations, given the ever growing decline in the US's importance to China's trade outcome.