RBA: RBA’s Hauser Says Rate Cut Chance “Very Low”, Inflation “Too High”

RBA Deputy Governor Hauser spoke to the ABC and noted that while the November CPI data was “helpful”, it was largely within expectations. It moved in the right direction for the RBA to prolong its pause but remain cautious. This view is in line with Hauser saying that the probability of near-term monetary easing is “very low” as the last rate cut this cycle has likely taken place.

- The new monthly CPI series is still to be tried and tested especially as it has a very short track record. Therefore, the Q4 quarterly print on 28 January is likely to be the key inflation data into the 3 February RBA decision.

- Hauser noted that inflation above 3.0% is “too high”. With the bank forecasting Q4 trimmed mean at 3.2%, policy could be on hold for some time unless it materially surprises to the upside and makes the RBA ask “what was driving that”, which Hauser said “might be an important part of our overall judgement”. The Board focuses on the inflation outlook and will provide updated forecasts at its February meeting.

- He noted that there “wasn’t a lot of news in the data yesterday for us” with Black Friday sales adding downward pressure on inflation but housing costs rising.

- Hauser refused to comment on market pricing for 2026 rate hikes.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

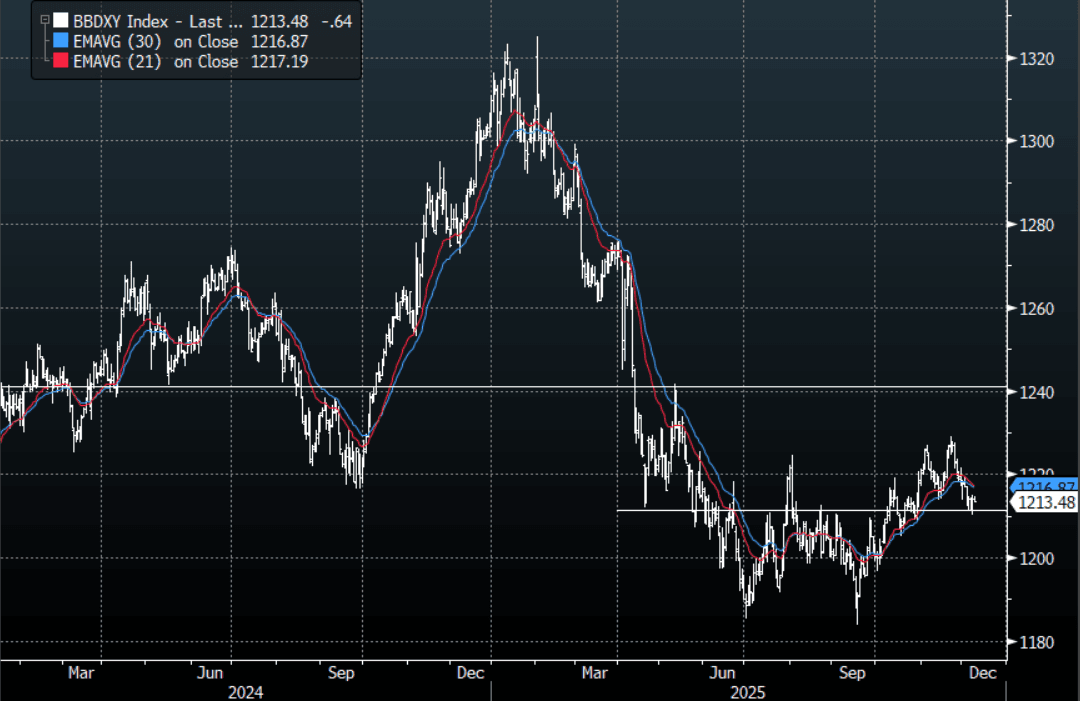

USD: BBDXY - Bounces Off 1210, Reacting To Higher U.S. Yields

The BBDXY range overnight was 1210.89 - 1214.88, Asia is currently trading around 1213, -0.05%. US yields continued to extend higher as we approach the FOMC, and overnight both risk and the USD started to react. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1219-1222. Support remains toward 1210 which needs to be worked through and then the more important 1205 area.

- MNI FED WATCH: 3rd Risk-Management Cut, Then Easing Bar Rises. The Federal Reserve is expected Wednesday to lower its overnight benchmark rate for a third straight meeting to 3.50%-3.75% but with dwindling support for continued easing, the bar moves higher on further cuts next year.

- Bloomberg - “The market is not positioned for higher US yields, leaving any further selloff in Treasuries exposed to an overhang of longs closing out. JPMorgan’s Treasury Client Survey shows the net long for all clients has reduced in the last couple of weeks, but remains elevated, while the net short for all clients and the active client segment remains very low.”

- The BBDXY Average True Range for the last 10 Trading days: 342 Points

Fig 1: BBDXY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

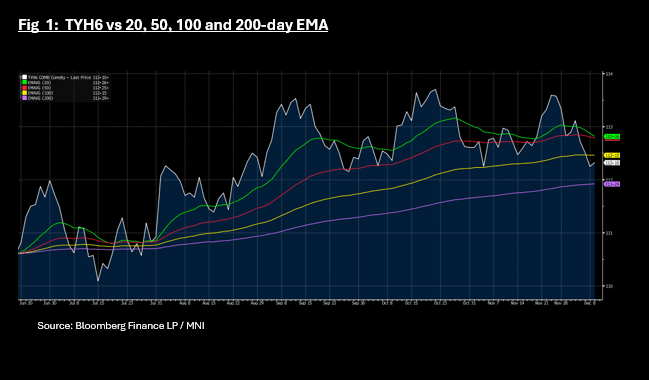

US TSYS: Yields Lower, TYH6 Near Mid-Point of Key Tech Levels

The US 10-Yr (TYH6) had opened the Asia trading day at 112-09+ with volumes low, sitting below the 100-day EMA of 112-15 for the first time since July. TYH6 is up at 112-10+ in morning trade, at the approximate mid-point between the 100-day EMA and the bottom side resistance being the 200-day EMA of 111-29+

Cash sees yields 0.3 -0.5bps lower. The 2-Yr and 3-Yr are unchanged this morning as markets are locked in for FOMC.

- The 2-Yr is at 3.577%

- The 5-Yr is at 3.745%

- The 10-Yr is at 4.162% - 0.4bps lower

- The 30-Yr is at 4.799% - 0.4bps lower

The 10-Yr remains in the 4.00% -4.20% range that has held in recent weeks. A more hawkish outlook from the FED could see new ranges established, particularly for the 10-yr.

Tonight sees a US$75bn 6-week bill auction and a US$39bn 10-Yr auction.

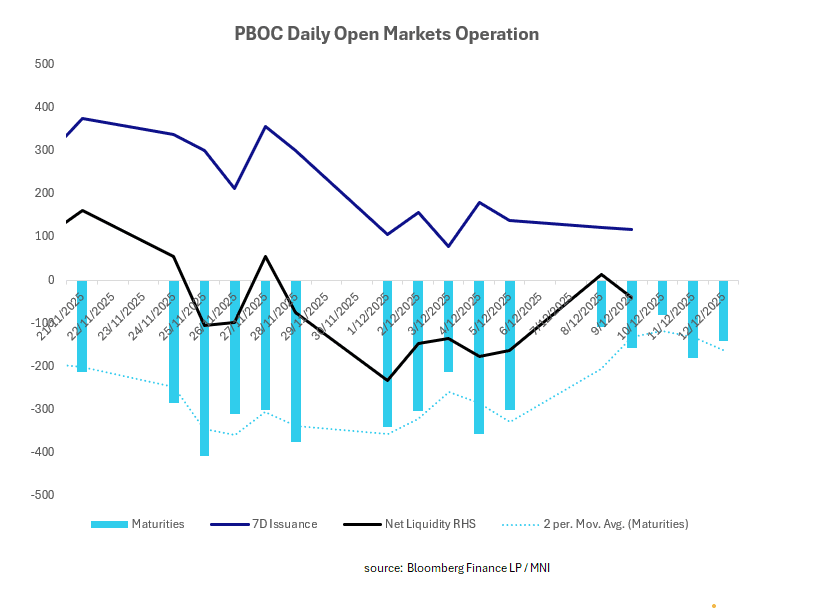

CHINA: Central Bank Withdraws CNY39bn via OMO

The PBOC kicked off the week with a modest injection yesterday ahead of a light maturity profile for 7-day repos, following the withdrawal of over CNY800bn last week. However today the OMO sees a move back to modest withdrawal despite signs that repo rates are trying to move higher.

- The PBOC issued CNY117.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY156.3bn.

- Net liquidity withdraws CNY39bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.32%, from the prior close of 1.20%.

- The China 7-day interbank repo rate is at 1.43%, from the prior close of 1.46%.