AUSTRALIA DATA: RBA Likely To Wait After Higher Core & Sticky Services Prints

Oct-29 01:25

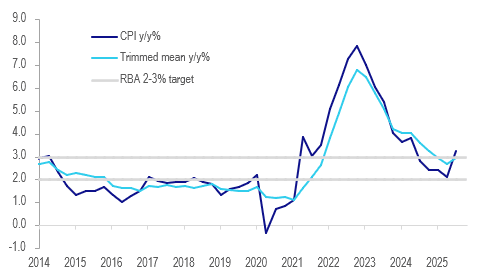

Q3 CPI printed higher than expected with the underlying trimmed mean rising 1.0% q/q to be up 3.0% y/y up from 0.7% q/q (revised +0.1pp) & 2.7% y/y. In August the RBA forecast Q4 at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid. Thus there is likely to be a near-term upward revision to its inflation forecasts at a minimum and given the Board’s cautious stance it looks like rates will be on hold on 4 November as it waits for more data.

Australia CPI y/y%

Source: MNI - Market News/LSEG

- The RBA also looks at the 2q/2q annualised rate, which printed at 3.4% in Q3, above the top of the 2-3% band and up from Q2’s 2.8%. At 3.0%, trimmed mean rose for the first time since Q4 2022. The quarterly rate was the highest since Q1 2024, when policy was being tightened.

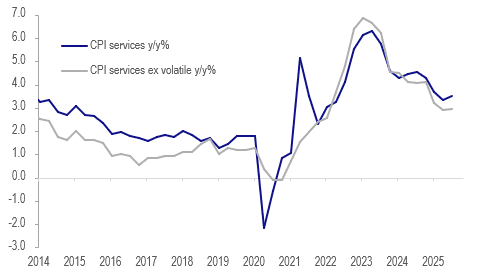

- Governor Bullock sounded worried about services inflation in September given trends in the July/August data and stickiness overseas. Australia’s headline services rose 1.3% q/q and 3.5% y/y up from Q2’s 3.3% due to rents and medical services. Market services also increased 1.3% q/q, in line with Q3 2023 & 2024, leaving the annual rate at 2.9% - both quarterly & annual rates tentatively suggest stickiness in Australia too.

- Headline continues to be impacted by government electricity rebates and jumped 1.3% q/q & 3.2% y/y in Q3 up from Q2’s 0.7% & 2.1%. The ABS noted that electricity prices rose 9% q/q. Other contributors to the quarterly CPI rise were housing (+2.5%), recreation (+1.9%) and transport (+1.2%).

- There are a lot of key data before the December meeting which the RBA may want to wait for, including October jobs on 13 November, Q3 wages 19 November, October CPI 26 November (first full sample monthly CPI) and Q3 GDP 3 December.

Australia services CPI y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

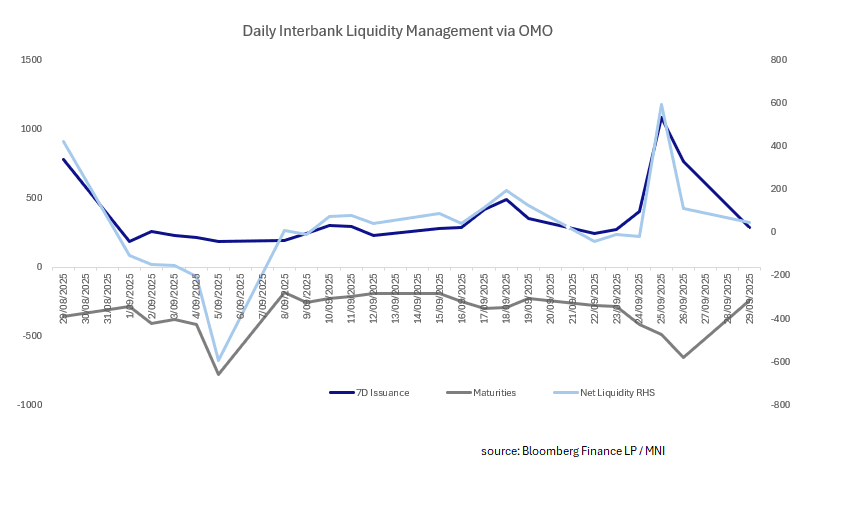

CHINA: Central Bank Injects CNY48.1bn via OMO

Sep-29 01:23

- The PBOC issued CNY288.6bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY240.5bn.

- Net liquidity injects CNY48.1bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.47%, from prior close of 1.55%.

- The China overnight interbank repo rate is at 1.32%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.58%.

MNI: CHINA PBOC CONDUCTS CNY288.6 BLN VIA 7-DAY REVERSE REPO MON

Sep-29 01:22

- CHINA PBOC CONDUCTS CNY288.6 BLN VIA 7-DAY REVERSE REPO MON

CNH: USD/CNY Fixing Edges Lower As USD Strength Stalls

Sep-29 01:17

The USD/CNY fix printed at 7.1089, versus a BBG market consensus of 7.1265

- This fixing moved lower again after bouncing towards the end of last week(Friday's print was 7.1152). The error term adjusted lower to 176 pips (from -307 pips last).

- Spot USD/CNH tracks near 7.1330 in latest dealings, down a little from the highs seen just below the 7.1500 area seen at the end of last week.