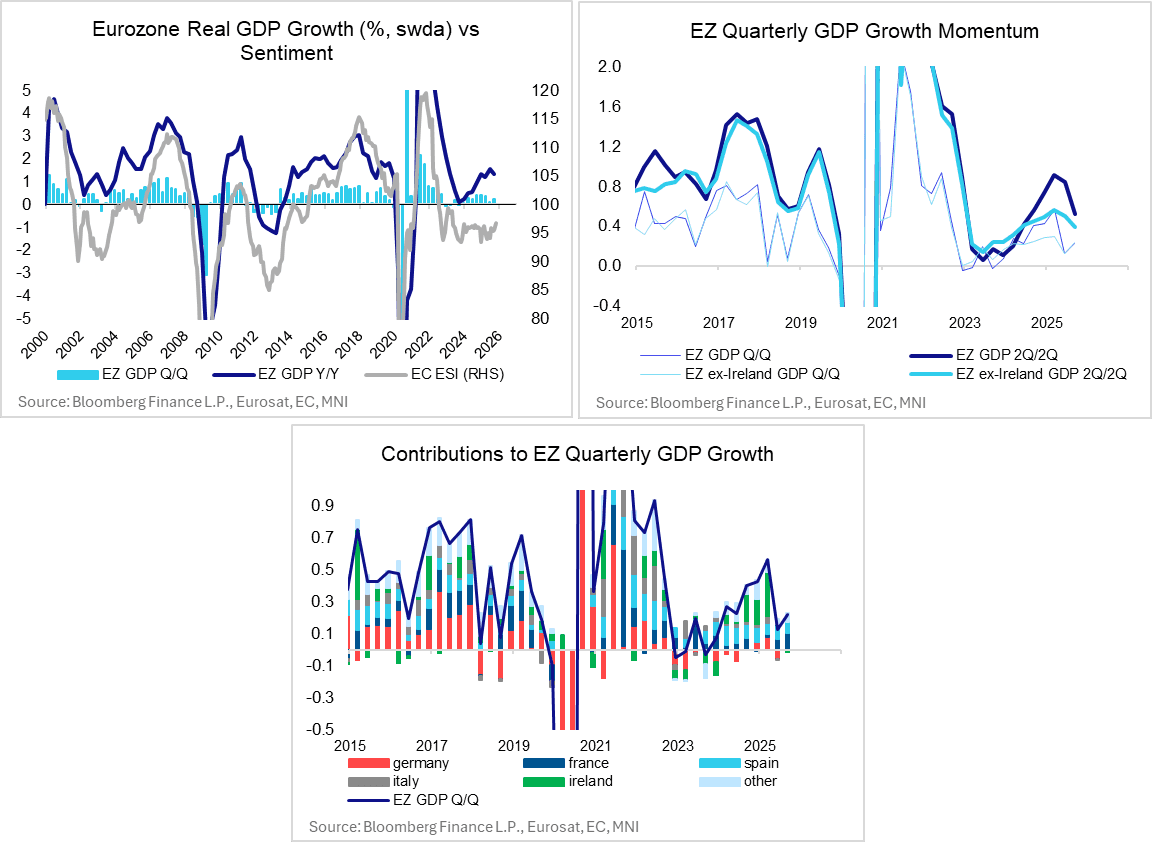

EUROZONE DATA: Q3 Flash GDP Prints Consistent With "More Balanced" Growth Risks

The Eurozone flash Q3 GDP readings released over the past two days have been consistent with ECB signalling that growth risks are “more balanced”. Given the lack of national accounts data available at present, we don’t expect any tweaks to the description of growth in the ECB’s balance of risk assessment today. However, a hawkish change could see growth risks described as “balanced” (rather than “more balanced”) in response to the stronger-than-expected Q3 flash GDP print and the solid October flash PMIs last week.

- The Eurozone-wide flash reading of 0.22% Q/Q was above consensus (0.1%) and the ECB’s September projections (0.0%). However, note that this still leaves underlying 2Q/2Q growth at its lowest since Q2 2024.

- Breaking down the 0.22% Q/Q flash reading, France contributed 0.10pp, Spain added 0.07pp, Germany made no contribution and Italy subtracted 0.01pp. The rest of the Eurozone added 0.06pp.

- A breakdown of expenditures is not available in all countries, including the Eurozone-wide release. However, summarising the details from the four largest economies:

- Domestic Demand: Appears to be positive in all countries except Italy. Gross fixed capital formation growth was highlighted in France (0.4% Q/Q), Germany and Spain (1.7% Q/Q)

- Net Exports: Mixed developments. The external sector contributed positively to growth in France and Italy, but negatively in Spain and Germany.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK: PM To Deliver Conference Speech @14:00BST Under Major Political Pressure

Prime Minister Sir Keir Starmer will deliver a keynote address to the annual conference of his centre-left Labour Party at ~14:00BST (09:00ET, 15:00CET) Livestream here. The speech is seen as an important one for the PM as he is set to remain under intense political pressure in the short and medium term:

- The latest opinion polling from Ipsos shows Starmer with the lowest personal satisfaction rating of any British prime minister since the outlet began conducting surveys in 1977. The PM's net rating for September is -66, with the previous recorded lows coming from Conservative prime ministers, Rishi Sunak (-59, April 2024) and John Major (-59, August 1994).

- The upcoming budget announcement on 26 November is expected to raise the UK's tax burden further from already post-war highs. MNI's Markets team have assessed some of the potential options for the chancellor ahead of the announcement. Higher taxes without demonstrable improvements in public services could spur further shifts in support towards Nigel Farage's right-wing populist Reform UK.

- The next electoral test for the PM and Labour comes in May 2026. Local elections will take place across swathes of England in addition to elections to the Scottish and Welsh parliaments. Poor results in these contests, particularly the loss of first place in Wales and control of cities in the Midlands and northern England to Reform UK could spark a leadership challenge against Starmer.

EUROPEAN INFLATION: German State-Level Details: Firmer Energy, Services

Looking a bit closer at this morning's German state level September CPI data, an energy acceleration to around -0.7% Y/Y (from -2.4% in August) stands out, bringing overall goods inflation to around 1.5-1.6% Y/Y (1.3% prior). Also services looks firmer than previously this time, at around 3.3% Y/Y (3.1% prior).

- Food inflation appears to have tapered off a little, to around 2.9% Y/Y in September (incl. non-alcoholic beverages, vs 3.2% prior).

- Within the services-heavy subcategories, the largest magnitude of change will likely be in education, we see the category around 3.9% Y/Y (from 5.1% prior, but note its low weighting in the CPI basket). Restaurants and hotels meanwhile seem to have accelerated, to around 3.9% - 4.0% (3.6% prior). Restaurants will see a VAT decrease in January in Germany.

- The mixed-weighting transport category meanwhile also accelerated, that comes on the back of the mentioned energy acceleration which is driven by base effects. We see transport at around 2.5% Y/Y in September (vs 1.4% prior).

LOOK AHEAD: Tuesday Data Calendar:Fed Speak, PMI, JOLTS, Cons Conf, House Prices

- US Data/Speaker Calendar (prior, estimate)

- 09/30 0900 Boston Fed Collins Council on Foreign Relations

- 09/30 0900 FHFA House Price Index MoM (-0.2%, -0.2%)

- 09/30 0900 S&P Cotality CS 20-City MoM (-0.25%, -0.20%), YoY (2.14%, 1.55%)

- 09/30 0945 MNI Chicago PMI (41.5, 43.3)

- 09/30 1000 JOLTS Job Openings (7.181M, 7.200M), Rate (4.3%, 4.2%)

- 09/30 1000 JOLTS Quits Level (3.208M, 3.165M), Rate (2.0%, --)

- 09/30 1000 JOLTS Layoffs Level (1.808M, 1.827M), Rate (1.1%, --)

- 09/30 1000 Conf. Board Consumer Confidence (97.4, 96.0)

- 09/30 1030 Dallas Fed Services Activity (6.8, --)

- 09/30 1130 US Tsy $85B 6W & $50B 52W bill auctions

- 09/30 1330 Chicago Fed Goolsbee Participates in a Q&A at Midwest Agriculture Co

- 09/30 1530 Chicago Fed Goolsbee on Fox Business

- 09/30 1910 Dallas Fed Logan moderated discussion

- Source: Bloomberg Finance L.P. / MNI