EU REAL ESTATE: Property: Week in Review

A positive tone in Credit was not matched in Equities. Stocks were between 1% and 7% lower on the week as the Fed quashed talk of another rate cut this year.

• Public Property Invest CEO sounded upbeat on the chance of an upgrade from Fitch. We looked at 5 criteria and tend to agree. See here and here.

• Digital Realty was moved to Pos by Moody’s on Data Centre strength. LEG Immo was also moved to Positive.

• S&P moved Heimstaden Bostad to Stable from Neg. The agency comments implied that mid-BBB may be within reach by YE26. See here.

• Immobiliare Grande Distribuzione returned to the market with €300m 5yr ms+212. The bonds attracted >1bn in orders and rallied 11bps to trade 7bps inside SuperNova 30s.

• CPI Property tapped the 30s for €200m to finance a Make-Whole on €256m CPIPGR 2.75 26 @ DBR+50. We see this bond maturing at ~100.19.

• AroundTown tapped their recent Perp for €200m to carry out a Clean-Up Call on 4 hybrids. (see Perps section)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: BLOCK: Nov'25 SOFR Ratio Call Spread

- 5,000 SFRX5 96.75/97.00 1x2 call spds, 0.0 net ref 96.36 at 0951:02ET

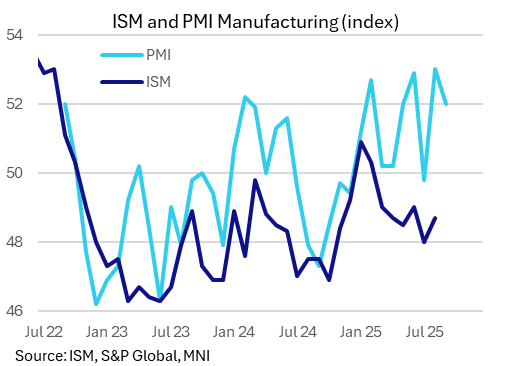

US DATA: Final Manufacturing PMI Unchanged From Flash, Still Shows Modest Growth

The final September manufacturing PMI reading was unchanged from the flash report at 52.0 (53.0 prior). The initial reading had been in line with consensus and both suggest a manufacturing sector in modest if slightly weaker expansion in the month, alongside elevated if somewhat softening price pressures. The sustained +50 readings have been cited by some analysts as reason for optimism on upcoming ISM reports (which have been lagging PMI readings for several months).

- From the S&P Global report: "The latest survey showed a weaker gain in production, whilst new order book growth softened as tariffs continued to weigh on exports. Tariffs and broader policy uncertainty also dampened firms’ assessment of the business outlook, but expectations of manufacturing production reshoring and hopes of better demand in the year ahead meant sentiment remained positive overall."

- On inflation: "Cost pressures meanwhile were again elevated, with tariffs reportedly the dominant factor pushing up overall purchase prices. Whilst firms sought to pass on higher supplier costs to clients, competitive pressures and signs of faltering demand meant output charge inflation softened to an eight-month low."

- The final September services / composite readings are out Friday.

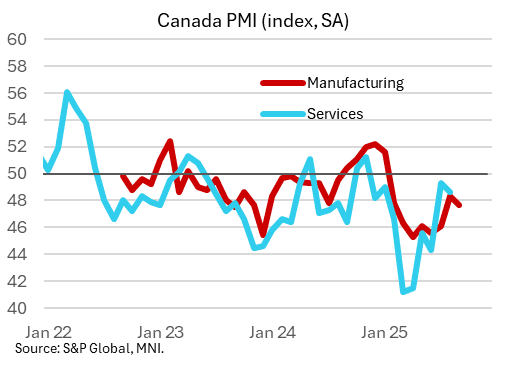

CANADA DATA: Manufacturing PMI Suggests Poor Activity, Softer Price Pressures

Canadian Manufacturing PMI softened in September, to 47.7 (no consensus) from 48.3 prior in what was an overall weak report. August had marked a 7-month high for the index, with the latest move lower keeping it below the 50 mark for an 8th consecutive month.

- The report showed poor demand, production, exports, and employment in the month, suggesting that a nascent pickup in activity over the summer (highlighted by better-than-expected GDP in July followed by anticipated flat growth in August) lacks momentum, at least in the beleaguered manufacturing sector. Per the S&P Global report:

- "Both output and new orders contracted in September, and at quicker rates than in August. Panellists continued to bemoan the adverse impact on demand of tariffs and wider economic uncertainty. Production and new orders have now fallen for eight months in a row. New export sales were again especially hard hit due to tariffs, with firms again pointing to continued weakness in sales to the United States. The lack of overall new orders and cuts to production meant firms generally chose to not replace leavers at their plants. Some firms also reported enforced layoffs. The net result was a decline in employment for an eighth successive month, although the rate of contraction was modest and the softest since February."

- While "Tariffs meanwhile remained an ongoing source of cost pressures in September and "Input prices again rose sharply", "the rate of inflation eased noticeably since August and was the second-lowest of the year so far." And importantly for the BOC's consideration, "Manufacturers struggled to pass on their higher input costs

to clients in the form of increased selling prices during the month. This was highlighted by the latest data on output charges, which increased only modestly in September and to the softest degree in nearly a year. Panellists attributed their lack of pricing power to market competition and a soft demand environment." - We get the Services/Composite PMI figures on Friday.