EU REAL ESTATE: Property: Week in Review

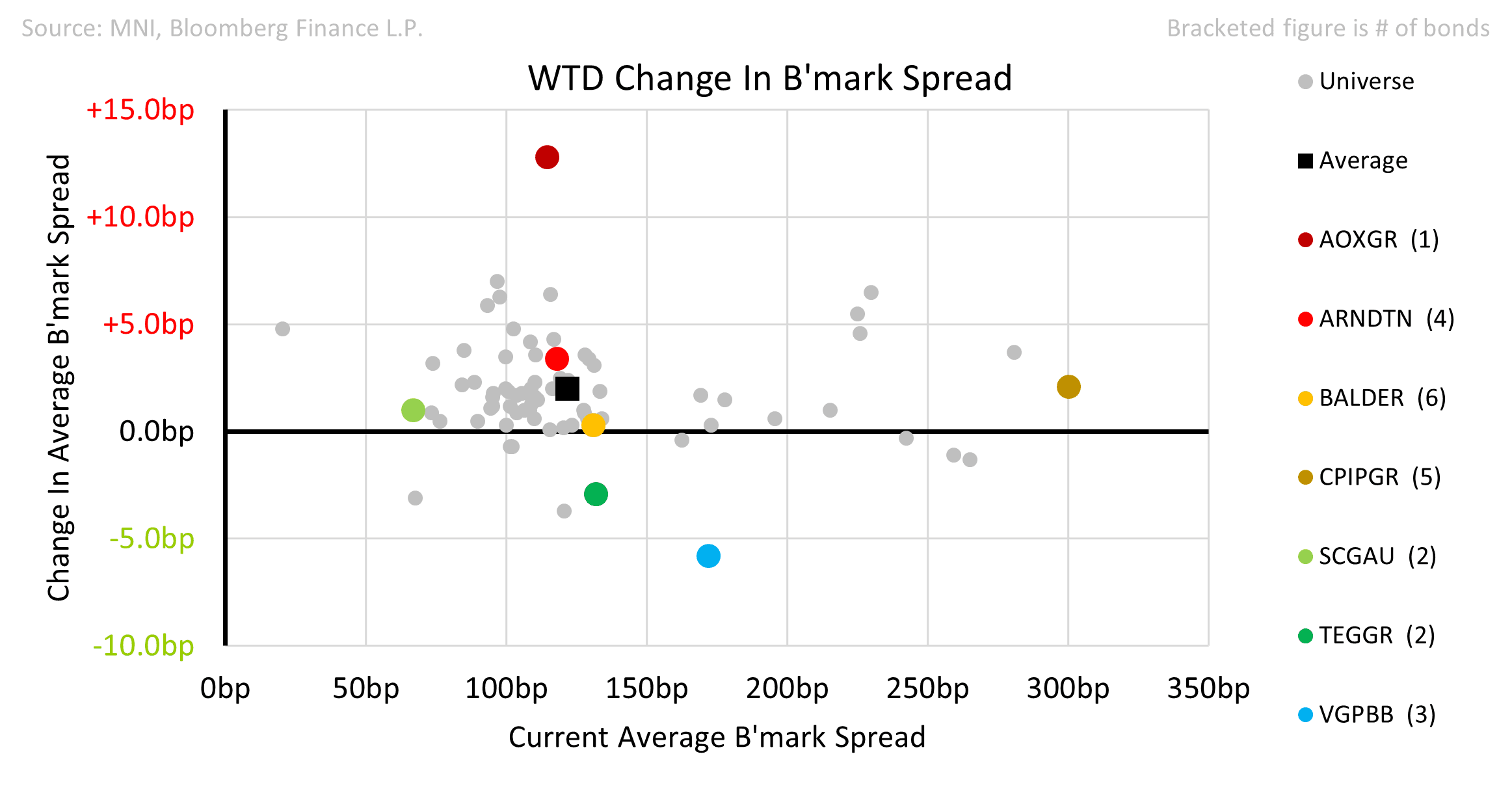

3 New Issues this week and 5 companies reported. Spreads a little softer as issuance picks up. VGPBB curve was the outperformer.

• Merlin returned to the market with a €550m 8yr Green bond. Its first issue in over 4 years. The deal came at a 10bps discount to the secondary curve which is arguably tight as the bonds are well-held. MRLSM’s expansion into Data Centres may require CAPEX of around €25bn (over many years) but they did tap the equity markets for €921m in July 2024 demonstrating a conservative approach. EQIX/DLR trade 20bps wider than Merlin.

• TAG Immo issued €300m 6.5yr to complete the repayment of bridge financing of the Resi4Rent Polish acquisition. Bonds came flat to Kojamo 32s and are now around 3bps inside. TEGGR 30s rallied 7bps on the week.

• Balder’s second visit to the market this year saw a dual-tranche €500m 7.5yr and a tap of the Jan-28s.

• SCentre demonstrated remarkably high and stable occupancy. Guidance was raised to +3% distribution.

• AroundTown reported a 2% reduction in LTV (40% ex-hybrids; 58% with). Vacancy at Offices and Retail is still too high for our liking though the company has managed a pivot away from Offices towards Residential & Hotels. The company is leaning towards a more positive growth strategy as the economy stabilises. Data Centres are a focus though refitting old offices is weak compared to Merlin’s green-field purpose-built units. Curve +3 wider.

• MLP Group continues to expand. Yield-on-cost for its pipeline is 11.5% so we don’t expect a slow-down. LTV c.43% remains very manageable.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GLOBAL MACRO: Key Deals Still Outstanding With Two Days to Go

As Trump confirms that the August 1st tariff deadline will not be extended, we make some tweaks to our list of still-outstanding key deals:

- Brazil: Talks with US advancing, Lula studying counter-tariffs, contingencies if 50% tariff installed

- Canada: Negotiations at an "intense phase" as of Monday

- Chile: Expects copper tariff exception, officials in Washington

- China: Trump to make call on extension, "a couple" of details still to work out

- India: Preparing to face higher US tariffs of 20-25% temporarily, US delegation in mid-August. Expects deal by Sept/Oct

- Mexico: Optimistic, aims for tariff agreement this week. Talks today.

- Norway: Tariff talks "still ongoing"

- Singapore: US 'non-committal' on 10% tariff staying, rising or falling

- South Africa: Remains committed to solution, but is working on response plan including tariff desk for exporters

- South Korea: Declines to comment on US demands for investment fund, actively discussing a package, hasn't heard whether deadline would be extended

- UK: Not expecting steel deal during Trump's UK visit

- Global: Baseline RoW tariff will be 15-20%

US: Trump Underscores August 1st Tariff Deadline

U.S. President Trump posts the following to Trump Social: "THE AUGUST FIRST DEADLINE IS THE AUGUST FIRST DEADLINE — IT STANDS STRONG, AND WILL NOT BE EXTENDED. A BIG DAY FOR AMERICA!!!"

EURIBOR OPTIONS: ERZ5 97.87 Puts Lifted

ERZ5 97.87 puts paper paid 1.0 on 18K.