AUSSIE BONDS: Post-CPI Rally Extends, AU-US 10y Diff Tightest Since Early Dec

ACGBs (YM +8.5 & XM +9.0) are sharply stronger. * Cash ACGBs are 7-8bps richer, extending yesterday...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD - BBDXY Consolidates Overnight Gains

The BBDXY has had a range today of 1213.40 - 1214.57 in the Asia-Pac session; it is currently trading around 1213, -0.05%. The USD has traded sideways in a quiet Asian session. US yields continued to extend higher as we approach the FOMC, and overnight both risk and the USD started to react. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1219-1222. Support remains toward 1210 which needs to be worked through and then the more important 1205 area.

- EUR/USD - Asian range 1.1635-1.1649, Asia is currently trading 1.1645. The pair continues to consolidate around the 1.1650 area. On the day it looks like dips back toward 1.1580-1600 should be supported initially, looking to retest the 1.1680 area again eventually.

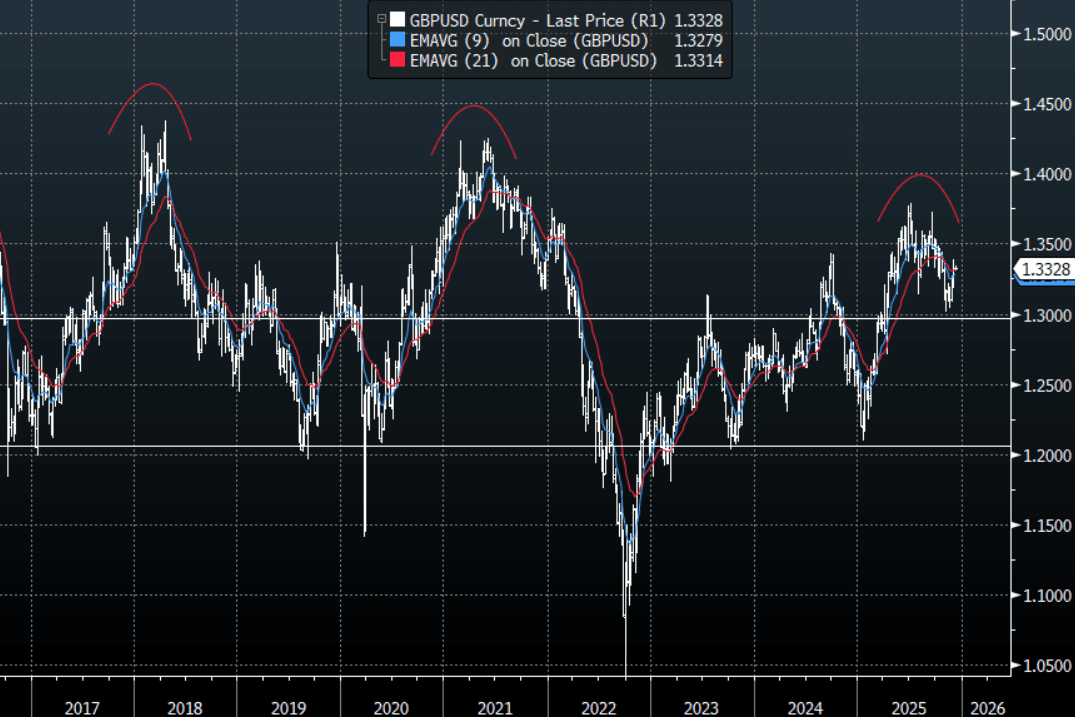

- GBP/USD - Asian range 1.3319-1.3335, Asia is currently dealing around 1.3330. The pair is consolidating on a 1.33 handle. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3260-1.3290 area, while above here look for the market to test the 1.3370-90 area again at some point.

- Cross asset : SPX +0.10%, Gold $4195, US 10-Year 4.166%, BBDXY 1213, Crude Oil $58.75

- Data/Events : Germany Trade Balance SA

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Largely Unchanged, Consolidating Below 156.00

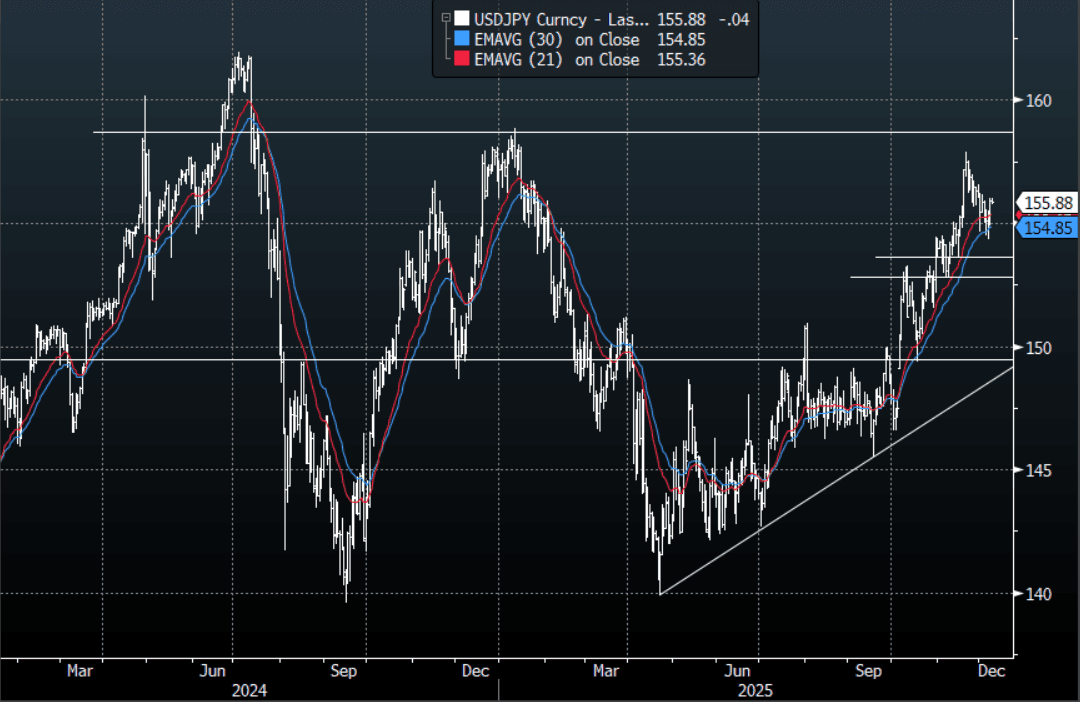

The USD/JPY range today has been 155.74 - 156.04 in the Asia-Pac session, it is currently trading around 155.90, +0.05%. The pair has traded sideways with little direction in a quiet session. The move overnight was supported by the sell-off in treasuries which has seen US yields move quite a bit higher as we approach the FOMC. The market is pricing in the fact that the Yen move looks likely to force the BOJ into action in December. This has stalled the upward momentum for the moment and could keep it contained in the short-term but I suspect the market will still look for opportunities to express a long USD at the right levels. Technically USD/JPY is still in an uptrend, the first big support back toward the 153-155 area has held on very well upon first examination. On the day, the market will be watching to see if there is any follow-through on this constructive price action. First support on the day is back toward 155.30-50, looking for a test of 156.20-40, a break of which would open up a move back to the 157.00 area.

- Bloomberg - “Foreign investors now dominate Japan’s $7.4 trillion government bond market, accounting for roughly 65% of monthly transactions, up from 12% in 2009. The BOJ’s retreat, coupled with PM Sanae Takaichi’s spending plans, have driven yields to multi-decade highs, sparking concerns of market volatility.”

- "AKAZAWA: SEE NO PARTICULAR CHANGE IN CHINA RARE EARTH CONTROLS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($589m), 157.00($425m). Upcoming Close Strikes : 155.00($1.1b Dec 12), 156.00($1.77b Dec 11), 159.00($1.4b Dec 12) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 91 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBA: More Concerned About Inflation & Its Drivers, Waiting For Q4 CPI

In a unanimous decision, the RBA’s Board decided to leave rates at 3.6% where they have been since August, which was expected. While it remains “cautious”, the statement shifted slightly hawkish with more concern regarding rising inflation but it needs “longer to assess the persistency of inflationary pressures”. It noted that there was “uncertainty” around monthly CPI data given it is new signaling that the Board was content this month to wait for Q4 CPI on 28 January ahead of the next decision on 4 February. Governor Bullock speaks to the press at 1530 AEDT.

- In terms of inflation, the RBA noted that the October CPI suggested “some signs of a more broadly based” increase in inflation and it could be “persistent” and needs “close monitoring". It also added to the guidance paragraphs that risks have now “tilted to the upside”.

- There was also concern around inflationary drivers. It pointed out that it is the WPI that has peaked while “broader measures” were strong and that unit labour cost growth remains “high”.

- Capacity utilisation was also said to be above its “long-run average” and reiterated that firms are finding it difficult to source labour. Consistent with this, Bullock said to the senate last week that while it is difficult to estimate, she believes that the output gap has closed.

- The Board no longer sees policy as “a little restrictive” but added the degree of restrictiveness to the list of uncertainties.

- It is also waiting for the full effect of 2025’s 75bp of easing to “flow through fully to demand, prices and wages”. But the recovery continues and private demand growth remains stronger than the RBA expected.