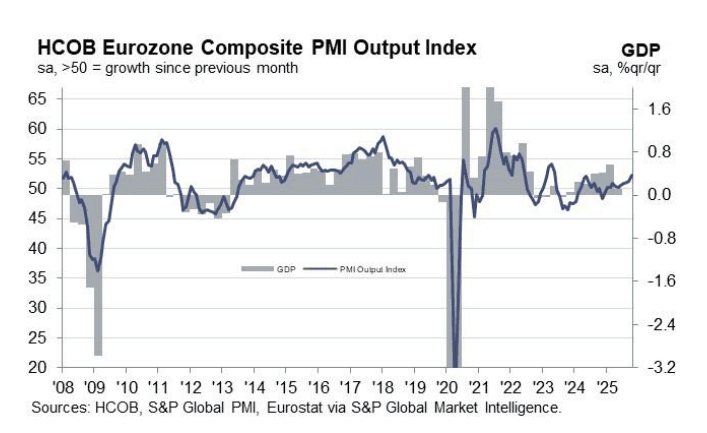

EUROZONE DATA: Oct Flash PMI: Composite At 17-month High; France The Laggard

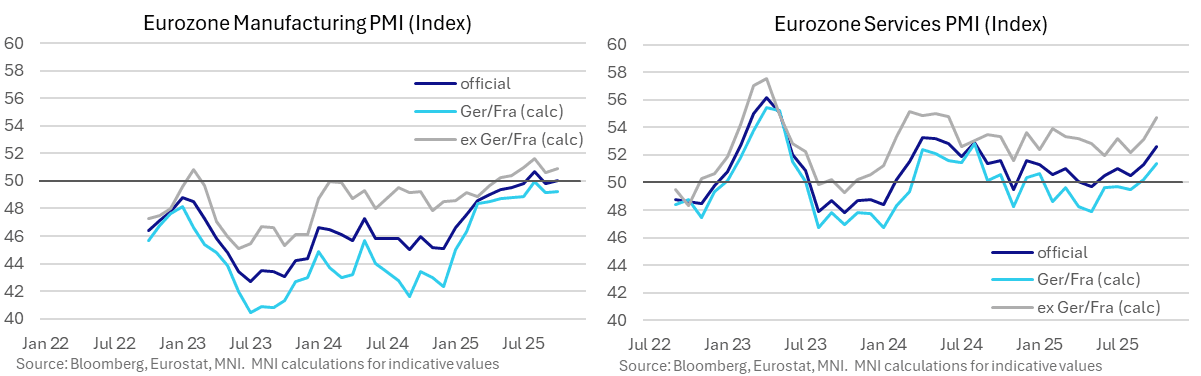

The Eurozone composite PMI rose to a 17-month high of 52.2 in October (vs 51.1 cons, 51.2 prior), supporting ECB Governing Council views that growth risks are “more balanced” at the very least. Strength was driven by Germany and the Eurozone excluding Germany/France, with France the clear laggard amid ongoing political uncertainty/volatility.

- The manufacturing PMI was 50.0, a little above the 49.8 consensus and prior. We estimate the Germany/France manufacturing PMI at 49.3 (vs 49.2 prior), and the ex-Germany/France reading at 50.9 (vs 50.6 prior).

- The services PMI was 52.6 (vs 51.2 cons, 51,3 prior).We estimate the Germany/France services PMI at 51.4 (vs 50.2 prior), the highest since August 2024. Meanwhile, the ex-Germany/France reading extended further to 54.7 (vs 53.1 prior).

Key notes from the Eurozone-wide release, focusing on ex-Germany/France commentary where possible:

- “The euro area excluding Germany and France posted the fastest rise in activity for two-and-a-half years.”

- “Companies often raised their business activity in response to a steeper increase in new orders during October….the overall expansion was led by the services sector, but manufacturing new orders broadly stabilised following a fall in September.”...."While overall new orders increased at a faster pace at the start of the final quarter, new business from abroad continued to decrease".

- “Encouraging trends in output and new orders contributed to a renewed increase in staffing levels during October”….” Jobs growth was centred on the services sector, where the pace of job creation was the sharpest since June 2024....manufacturing employment decreased at the fastest pace in four months.”

- “While input costs increased at a slower pace at the start of the fourth quarter, the opposite was true with regards to output prices, which rose at the fastest pace in seven months. Manufacturers increased their selling prices for the first time in six months, joining the services sector in recording inflation.”

- “Solid increases in output prices were registered in Germany and the euro area excluding the largest two economies, but French companies raised their charges only slightly amid deteriorating customer demand.”

- “Despite stronger expansions in output and new orders in October, business confidence waned to a five-month low”…“ signalled across both the manufacturing and services categories”….” Sentiment was relatively muted in Germany and France, but firms in the rest of the eurozone remained strongly confident that output will rise over the coming year.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: USD extends small gains

- No real reaction in Bund, althought it has pushed higher after the German IFO missed expectatio, came below consensus, the EURUSD dipped to session low on tyhe back of it.

- The liquidity has been quite poor acroos assets in early and most of the moves in G10 FX have been a function of the Dollar bid, as Cable also push through a new intraday low.

- Closest Technical in G10 FX is in Cable, with the next support eyed at 1.3458, the Trendline support drawn from the Aug 1 low.

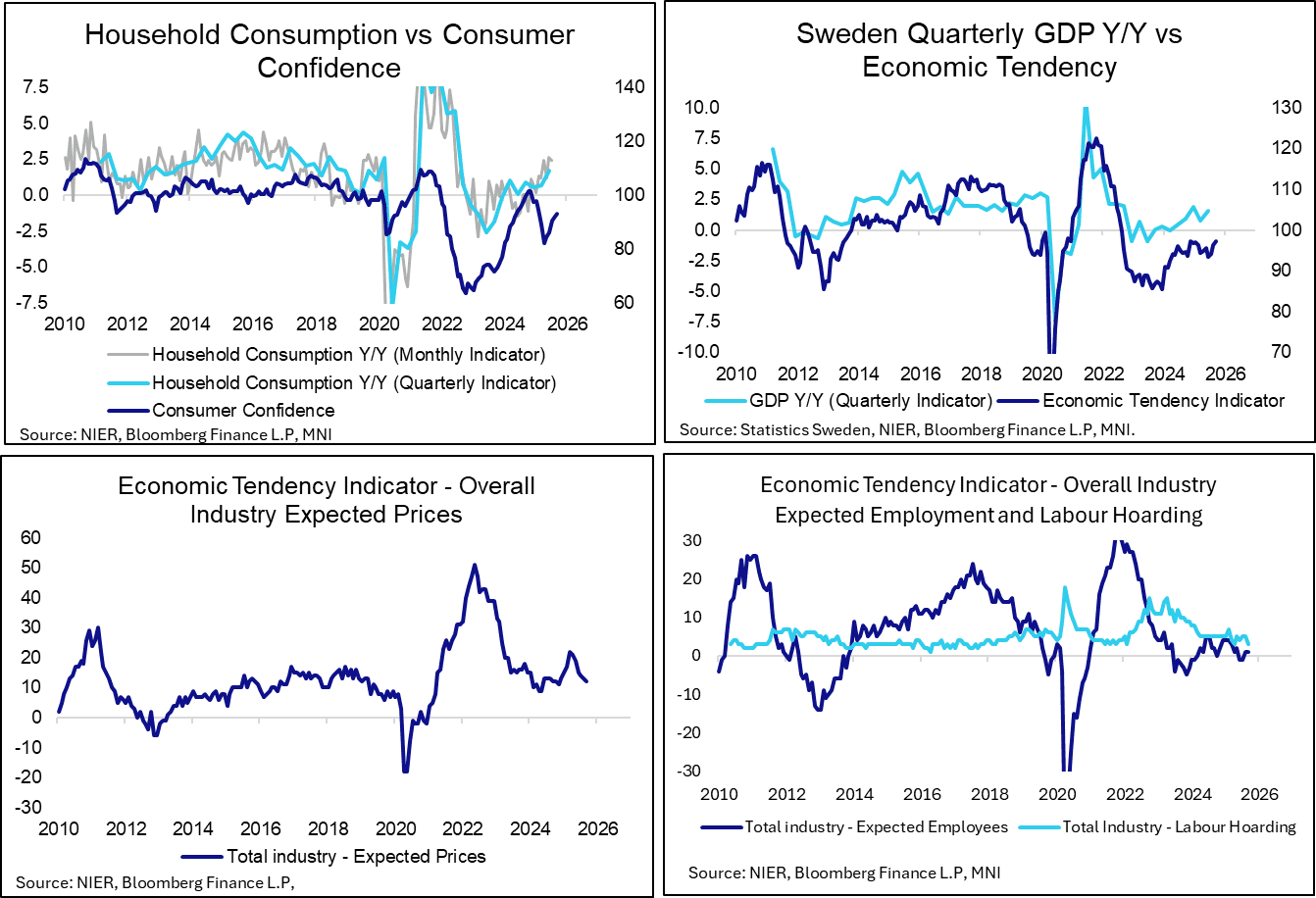

SWEDEN: Sep ETI: Sentiment Picking Up, Inflation Pressures Easing

The Swedish Economic Tendency indicator rose to a year-to-date high of 97.2 in September (vs 96.3 prior). Increases were seen in consumer confidence, alongside the retail, construction and manufacturing sectors. Services sector confidence declined a little.

- Sentiment remains below the neutral 100 level, but the combination of another Riksbank rate cut and increased Government fiscal spending (with particular emphasis on households) should support further improvements ahead. Key for both institutions is whether this translates to better real consumer spending/economic activity outcomes.

- Barring an unexpected shock. the Riksbank’s easing cycle is likely over after yesterday’s 25bp cut to 1.75%.

- Consumer confidence rose for a fifth consecutive month to 93.2, up from a year-to-date low of 82.2 in April. Relative to August, the “Macro” index (consumer’s perceptions of general economic activity) rose to 97.6 (vs 94.8 prior) while the “Micro” index (consumer’s perceptions of their personal economic situations) rose to 90.5 (vs 89.0 prior).

- Business sentiment is strongest in the retail sector (106.5 vs 105.8 prior), after a brief dip below 100 in June. Other sectors remain below neutral.

- Expected prices continued to decline (diffusion index of 12 vs 13 prior and a YTD high of 22 in March), supporting the Riksbank’s assessment that the summer inflation rise was likely to be temporary.

- The expected employment diffusion index was steady at 1, while the labour hoarding index eased to 3 (vs 5 prior).

SOFR OPTIONS: 0QX5 96.875/97.125 Strangle Trades

0QX5 96.875/97.125 strangle desks initially suggest that paper paid 15 on 6K, while others point to a vol seller. -4% delta.