AUSSIE BONDS: Modestly Cheaper, AU-US 10Y Diff At Fresh High

ACGBs (YM -3.0 & XM -3.0) are modestly cheaper in today’s pre-holiday shortened session.

- Cash US tsys showed little reaction to the FOMC minutes release for the December meeting yesterday. The key paragraph from the December FOMC meeting minutes (link here) indicates (as did the meeting Dot Plot) a sizeable minority of members seeing no further easing through end-2026, but a base case among a solid if narrow majority that further limited cuts would ensue if the data cooperate.

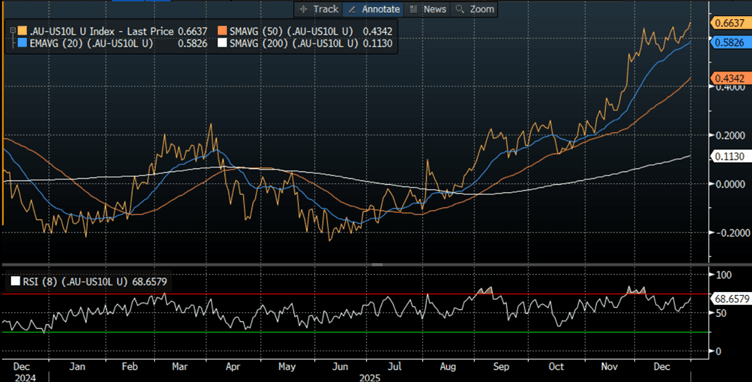

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at +65bps, a fresh cycle high.

- The bills strip is cheaper, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 108% by June and 163% by December 2026.

- By the end of January, Australians should have a clearer picture of whether they can expect interest rate hikes in 2026. Quarterly inflation data, due to be released on January 28, will confirm or allay RBA fears that upward price pressures are entrenched in the economy.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Futures Challenging Recent Lows, Q3 GDP Out Wednesday

The early bias in Aussie bond futures is weaker, with 3yr (YM, last 96.08) and 10yr (XM, 95.45) futures off around 1.5-2.5bps in the first part of dealings. ACGB yields are around 1.5-2bps firmer across the curve, a continuation of recent yield gains. This follows a softer lead from US Tsy futures on Friday, in what was an impacted session by CME data issues and shortened due to the Thanksgiving break. There were no obvious headline drivers for US Tsys. The AU-US 10yr sits at +52bps, close to recent cycle highs, the differential having established a new higher range amid a dovish Fed backdrop, and uncertainty around whether the next RBA move could be a hike.

- For Aussie futures, the 10yr is back at lows from last week at 95.45, with downside focus on 95.415, then 95.30, levels last seen in the first half of the year. For the 3yr, downside focus will be on test under 96.00.

- In cash ACGB yields, the 3yr is near 3.88%, with upside focus likely to rest in the 3.95-4.00% region. The 10yr is just above 4.53%, with earlier 2025 highs above 4.60%. The AU 3/10s curve is close to recent lows, last +65bps.

- Little easing risk for the RBA is priced in the next few months, while by the Nov meeting next year around 10bps of tightening is priced in.

- Earlier we had the final S&P Global manufacturing print for Nov. It was unchanged at 51.6 versus the initial flash estimate.

- The highlight of the week will be Wednesday’s Q3 GDP which Bloomberg consensus expects to show a pickup in growth to 0.7% q/q and 2.2% y/y after Q2’s 0.6% & 1.8%. Other inputs into GDP are released this week with inventories as part of Monday’s Q3 business indicators. It is expected to be flat while company profits should rise 1.6% q/q after Q2’s 2.4% q/q decline.

OIL: Crude Finished November Down, OPEC To Leave Q1 Output Steady

Oil prices finished November down. As expected OPEC decided to continue with its plan to leave output unchanged through Q1 as it is a time of seasonally low demand. It had been unwinding previous output reductions through 2025 but with a record market surplus forecast for 2026, this was an opportunity to pause.

- OPEC agreed to allow a review of members’ production capacity which will help with quota setting for 2027. The next meeting is 4 January.

- In holiday-thinned trading, WTI fell 0.3% to $58.48/bbl to be down 3.5% in November. It reached a high of $59.64 before declining to $58.27. A bearish trend remains intact with the bear trigger at $55.99, while resistance is at $61.84.

- Brent was down 0.9% to $62.32/bbl on Friday to finish the month 2.9% lower. It rose to $63.39 before falling to $62.12, holding above the bear trigger at $59.93.Initial resistance is at $65.25.

- Ukraine struck a Russian refinery and a vessel from its shadow fleet in the Black Sea over the weekend. Attacks drove diesel prices higher through much of November but have been trending lower since negotiations for a peace deal began and were down 5.1% last week.

- Talks continued between the US and Ukraine in Florida over the weekend with Secretary of State Rubio saying that they were “productive” but “more work” is needed. President Trump said that Envoy Witkoff will meet President Putin this week.

BONDS: NZGB Yield Rise Extends, NZ-US10yr To +27bps, Second Tier Data This Week

NZGB yields are higher for most parts of the curve, up around 2-4bps in early Monday dealings. The 5 and 7yr tenors are leading the move, although the 2yr is lagging (off around 1bps). This is extending last week's break higher in yields, as speculation continues around what the next move will be for the RBNZ (most likely an extended pause, but markets are pricing in hike risks towards the end of 2026). The 10yr was last near 4.26%, while the 2yr is holding under 2.75% at this stage.

- This leaves the NZ 2/10s curve steeper at near +152bps, but we remain off recent highs near +160bps. These moves follow a generally positive session for US Tsy yields on Friday (albeit a shortened one, which was also impacted by a CME data issue, which impacted Tsy futures). Still, the NZ-US 10yr spread continues to push higher following last week's break higher, last around +27bps.

- The 2yr swap rate (NDSO2) is up around 5bps to near 2.70%, which is fresh highs back to mid Sep.

- We had Oct building permits data a short while ago, which fell -0.9%m/m, but this follows a 7.3% gain for Sep.

- This week's data calendar is second tier. Terms of trade for Q3 print tomorrow, while on Wednesday the Nov ANZ commodity price and Nov home prices. On Thursday, Q3 volume of construction work done is out.