BONDS: Modest Extension Lower In Core Bonds On Hawkish BoJ Sources, JGBs Unmoved

Dec-12 12:47

The hawkish BoJ sources piece from BBG applies some modest, fresh selling pressure across core global FI markets, with TY, Bund and gilt futures softer in the time since the headlines crossed.

- Still, initial support levels remain intact and unchallenged across those contracts.

- Also note that the modest JPY FX strength that followed the headlines was quick to fade, while JGB futures barely moved on the news (offshore markets were a little more sensitive), given that markets are already aware of the BoJ ‘s elongated reassessment of its neutral rate estimate, as well as the fact that the market was already pricing further tightening beyond next week’s BoJ meeting.

- The sources piece indicated that some BoJ officials believe that the terminal rate lies above 1.00%, which won’t come as a shock given widespread prior reporting on the matter.

- Meanwhile, the latest BBG survey reveals median terminal rate expectations of 1.25% amongst the surveyed economists.

- 55bp of cumulative BoJ tightening is priced between now and October ’26 (with 23bp of tightening priced for next week’s decision). That would take the BoJ’s policy rate to the lower boundary of the Bank’s current 1.00-2.50% estimated range

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

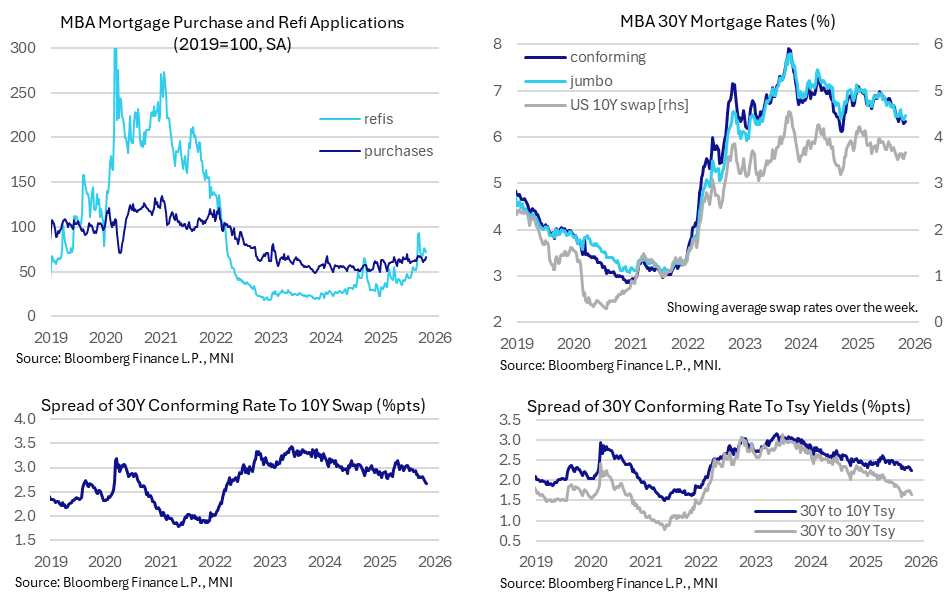

US DATA: Mortgage Rates Steady As Swap Spread Narrows Further

Nov-12 12:28

Mortgage applications were essentially unchanged last week even if it masked a strong uptick in new purchase applications. Mortgage rates have been steady in recent weeks, benefiting from a sizeable tightening in spreads to swap rates.

- MBA composite mortgage applications inched 0.6% higher last week (sa) after -1.9% and 7.1% in the previous two weeks.

- The details were a little more interesting than that suggests though, with new purchase applications increasing 5.8% (largest since early Sept and before that early June) compared to refi applications slipping -3.4%.

- Levels relative to 2019 average for context: composite 71%, new purchases 67%, refis 72%.

- The flatlining in overall activity came as the 30Y conforming rate ticked up 3bps to 6.34% after the 6.30% two weeks prior had been the lowest since Sep 2024.

- The relative stability in mortgages rates in the latest few weeks has come with a further tightening in spreads to swap rates.

- The 30Y mortgage rate to the average 10Y swap rate through the week fell further to 267bps, a fresh low since Apr 2022, compared to an average 285bp in Q1 and a rough range of 300 +/-5bp for some months after reciprocal tariff announcements in April prompted some additional caution in lending standards.

- This narrowing in spreads will be well received by the Trump administration.

OUTLOOK: Price Signal Summary - Bear Cycle In Bunds Remains Intact

Nov-12 12:21

- In the FI space, Bund futures are trading above their recent lows. A short-term bear cycle remains intact and Monday’s fresh cycle low reinforces the bear theme. The contract has cleared a number of important support points; the 50-day EMA, at 129.14, and 128.92, the 61.8% retracement of the Sep 25 - Oct 17 bull leg. Scope is seen for an extension towards 128.52, the 76.4% retracement. Resistance is at 129.31, the 20-day EMA.

- The trend theme in Gilt futures remains bullish and this week’s strong bounce - so far - reinforces a bull theme. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on the bull trigger at 93.98, the Nov 4 high. A clear break of this hurdle would confirm a resumption of the uptrend and open 94.24, a 1.618 projection of the Sep 3 - 11 - 26 price swing. Support to watch lies at 93.09, the 20-day EMA.

MNI EXCLUSIVE: Belgian Debt Agency's Director of Treasury Speaks To MNI

Nov-12 12:14

Maric Post, the Belgian Debt Agency's Director of Treasury and Capital Markets, speaks to MNI.- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

Related bullets

Related by topic

Bunds

Germany

UK

US Treasuries

JGBs

Bank of Japan

Japan