MNI US OPEN - US Reportedly Preparing for Strike on Iran

EXECUTIVE SUMMARY

- US OFFICIALS PREPARE FOR POSSIBLE STRIKE ON IRAN IN COMING DAYS

- MNI BOE PREVIEW - ALL ABOUT THE VOTE AND MINUTES

- NORGES BANK CUTS TO 4.25% AGAINST MARKET CONSENSUS

- US CASH MARKETS CLOSED, CORPUS CHRISTI MAY THIN LIQUIDITY IN EUROPE

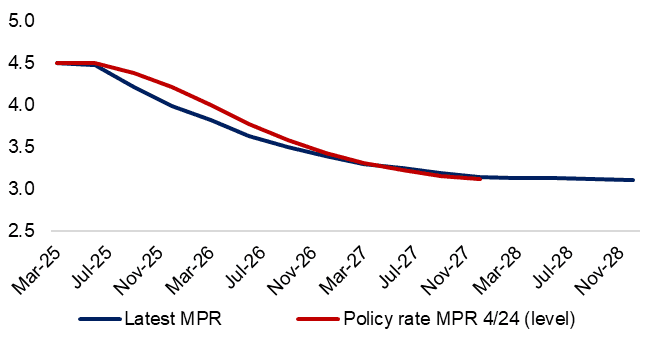

Figure 1: Norges Bank policy rate forecast revised lower following surprise rate cut

Source: Norges Bank, MNI

NEWS

US: Cash Markets Closed for Juneteenth Public Holiday

US cash markets are closed for the Juneteenth public holiday, which will thin out liquidity into the afternoon. UST futures close early at 13:00ET/18:00BST.

EUROPE: Corpus Christi Day Could Thin Out Liquidity

Corpus Christi Day may thin out desks in some areas of Europe, making for lighter liquidity in wider markets. Regional holidays in Germany and Switzerland are the most noteworthy.

US/MIDEAST (BBG): US Officials Prepare for Possible Strike on Iran in Coming Days

Senior US officials are preparing for the possibility of a strike on Iran in the coming days, according to people familiar with the matter, a sign that Washington is assembling the infrastructure to directly enter a conflict with Tehran. The situation is still evolving and could change, said the people, who requested anonymity to discuss private talks. Some of the people pointed to potential plans for a weekend strike. Top leaders at a handful of federal agencies have also begun getting ready for an attack, one person said. A White House official said that all options remain on the table.

US/EU (FT): EU Weighs UK-Style Trade Deal With US

The EU is pushing for a UK-style trade deal with the US that would leave some tariffs in place after next month’s deadline, further delaying retaliation against Washington. Michael Clauss, adviser to German Chancellor Friedrich Merz, told an FT Live event in Berlin on Thursday that instead of a full deal by July 9, he expected “a declaration saying: ‘OK, this is a little bit along the model of the US-UK [agreement]’.” Diplomats and officials briefed on the matter say that early talk in Brussels of retaliatory levies if US President Donald Trump did not lift all measures against EU countries has diminished as governments in the bloc fear the economic consequences, and the risk of European internal disagreement on taking countermeasures.

US/JAPAN (BBG): US Focus on Auto Trade Gap Is Sticking Point for Japan Deal

A strong US focus on its auto trade deficit with Japan is a key factor keeping the two nations from reaching a deal, according to a Japanese opposition party leader who met with Prime Minister Shigeru Ishiba to discuss the tariff negotiations. Yoshihiko Noda, who heads the Constitutional Democratic Party of Japan, said on Thursday that he asked Ishiba what was preventing the two sides from finding common ground in the talks that have continued for around two months.

MNI FED REVIEW - JUNE 2025: Less Uncertainty, Less Easing

The June FOMC communications had a hawkish tilt overall, despite the immediate dovish reaction to the updated Dot Plot retaining the median expectation of 50bp in rate cuts by end-2025. Chair Powell was far from emphatic about the prospect of rate cuts, all but taking a cut at the July meeting off the table. His comments all but reversed the initial dovish market reaction. That said, the FOMC still remains committed to cutting, if only in half-hearted and patient fashion.

MNI BOE PREVIEW - JUNE 2025: All About the Vote and Minutes

The June MPC meeting will be a surprise to markets if the outcome is anything other than an on hold decision with unchanged official guidance. Expectations are relatively strongly pointing towards a 7-2 vote split with both Dhingra and Taylor likely to follow up their votes for a 50bp cut in May with a vote for a sequential cut (the magnitude of which is unlikely to elicit a market reaction). The main focus is on whether the dataflow has been enough to convince any other members of the MPC to vote for sequential cuts.

UK (BBG): London Seeks More Chinese Listings as City Battles IPO Drought

London is seeking to attract more Chinese firms to list on its stock exchange as the city struggles with a shrinking equity market and a deal drought across Europe. “We need to get more IPOs happening in London,” Chris Hayward, policy chairman of the City of London Corp., said in an interview from Shanghai. “We don’t want to lose business across the Atlantic.” The authority for London’s Square Mile financial district can provide opportunities for Chinese firms to secure customers and funding in the UK and drive them to list in the city via its connect scheme with Shanghai, Hayward said.

NORGES BANK (MNI): Norges Bank Delivers Surprise Policy Rate Cut

Norges Bank finally started its easing cycle, cutting the policy rate by 25bp to 4.25%, stating that if the economy evolved broadly as expected that the rate would be reduced further this year. The policy rate was set at 4.50% back in December 2023 and stayed there until now and analysts were largely anticipating another no change decision in June. Governor Ida Wolden Bache, however, said that the near term inflation outlook was softer than previously assumed and "a cautious normalisation of the policy rate will pave the way for inflation to return to target without restricting the economy more than necessary."

SNB (MNI): SNB Cuts by 25bp to 0.00%, Inflation Forecast Lower

SNB cuts by 25bp to 0.00%. Core FX communications paragraph appears materially unchanged on first sight "remain willing to be active in the foreign exchange market as necessary". Conditional inflation forecast slightly downwardly revised: 2025 0.2% (vs 0.4%), 2026 0.5% (vs 0.8%), 2027 0.7% (vs 0.8%) GDP forecasts marginally downwardly revised: 2025 1.0-1.5% (vs 1.0-1.5% in March meeting); 2026 1.0-1.5% (vs 1.5% in March) Press statement with neutral rates outlook: "The SNB will continue to monitor the situation closely and adjust its monetary policy if necessary, to ensure that inflation remains within the range consistent with price stability over the medium term."

ECB (BBG): ECB’s Rehn Says Lasting Mideast Crisis Could Be Stagflationary

An extended flare-up of the crisis in the Middle East could cause a stagflationary shock in the euro area, European Central Bank Governing Council member Olli Rehn said. That would mean inflation accelerating at the same time as economic growth weakens and unemployment rises, Rehn writes in column published by Finland’s government on Thursday. On the other hand, the baseline scenario shows the subdued growth outlook is weighing on inflation next year, Rehn says.

ECB (MNI): Villeroy Says if Rates Move, More Likely to Be Cut

The European Central Bank is more likely to cut than increase its deposit rate if it adjusts it over the next few months, though the ECB also has to be alert to the inflationary impact of higher oil prices, Bank of France Governor Francois Villeroy said in a speech in Florence on Thursday. "The current assessment suggests that, barring a major exogenous shock, including possible new military developments in the Middle East, if monetary policy were to move in the next six months, it could be more in the direction of accommodation," Villeroy said, adding that monetary policymakers needs to remain alert and agile given uncertainties over trade and the conflict in the Middle East.

GERMANY (MNI): Merz Placating States But Tax Cut Delays Possible

Chancellor Merz has hinted a compromise will be met following state-level discontent around the "growth booster" tax package, which would otherwise incur expenditure gaps for the state and municipal level. Nevertheless, some delays for the programme may be possible if no compromise is met. A federal-state working group will come up with a proposal leveraging sales tax redistribution or fixed amount transfers to ensure state and municipal-level compensation, Handelsblatt comments. If a compromise is not being met before at least passing in Bundesrat, which is planned for 11 July, the draft bill could end up in the Bundesrat's "mediation committee", which would at least slow its passing down.

SWEDEN (MNI): Long-Term Inflation Expectations Comfortably Anchored Around Target

Swedish long-term inflation expectations remain well-anchored around the target, according to Origo Group's latest "big" expectations survey. Inflation expectations have broadly tracked developments in spot, which have been on a decelerating trend since March. More favourable inflation prospects encouraged the Riksbank to lend more support to economic activity with a 25bp cut at yesterday's meeting.

JAPAN (BBG): Japan to Propose Trimming Super-Long Bond Issuance From July

Japan’s finance ministry is considering trimming its issuance of super-long bonds starting in July, according to a draft of a revised bond issuance plan seen by Bloomberg. The ministry is set to propose cutting issuance of 20-, 30- and 40-year bonds by ¥100 billion ($690 million) each per auction through the end of March 2026, the draft plan showed Thursday. To offset the decrease, the ministry is considering increasing issuance of 2-year bonds and other shorter-dated debts.

JAPAN (BBG): Japan Ruling Party Makes Election Pledge of 50% Pay Rise by 2040

Japan’s ruling party said it aims to ensure workers secure a cumulative 50% pay increase by 2040 with the economy expanding to a value of ¥1 quadrillion ($6.9 trillion) as it unveiled its platform ahead of a national election next month. The Liberal Democratic Party will try to ensure real wages and nominal wages rise annually by 1% and 3%, respectively, so that annual pay will increase by ¥1 million by fiscal 2030, according to its campaign manifest released on Thursday.

BRAZIL (MNI): BCB Raises Rate to 15.00%, Rates to Stay Elevated

The Brazil central bank raised the Selic rate to 15.00%. The market, sell-side consensus, had been for a steady 14.75% policy rate outcome (which was also our on bias). It was a close call though, as we noted in our BCB preview: "with economic activity appearing resilient and the labour market still tight, the Copom may opt to hike rates by a further 25bp, as the committee continues to stubbornly pursue the convergence of inflation to target." The BCB noted in its statement: "Copom decided to increase the Selic rate by 0.25 pp to 15.00% pa, and judges that this decision is consistent with the strategy for inflation convergence to a level around its target throughout the relevant horizon for monetary policy."

MNI CBRT PREVIEW - JUNE 2025: Room to Hold Until July

The CBRT is expected to keep its one-week repo rate unchanged at 46.00% this month following a 350bp hike in April, but risks of a rate cut are noted by some analysts given the recent slowdown in monthly inflation. However, upside price pressure stemming from FX weakness post the arrest of the Istanbul mayor Ekram Imamoglu in March ultimately warrants further caution, while increased funding through the key policy window has already led to a reduction in the weighted-average funding rate.

PHILIPPINES (BBG): Philippines Cuts Key Rate Again as Inflation Stays Below Target

The Philippine central bank lowered its key interest rate by a quarter point for the second time this year as widely expected, after inflation remained below target. The Bangko Sentral ng Pilipinas reduced its overnight target reverse repurchase rate to 5.25% on Thursday. The BSP stayed on an easing path after inflation slowed further in May, staying below the central bank’s 2%-4% goal for a third month. The move is in line with Governor Eli Remolona’s signal last month for at least two more rate cuts this year, continuing a cycle of reductions that started in August.

TAIWAN (BBG): Taiwan Holds Key Rate as It Weighs Tariffs, Currency Gains

Taiwan held its benchmark interest rate for the fifth straight quarter as it considers worries about the impact of tariffs on the economy, inflation and currency gains. The policy rate stayed at 2%, the central bank in Taipei said in a statement Thursday. The Central Bank of the Republic of China, as the institution is formally known, trimmed its prediction for consumer price index growth this year to 1.81% from 1.89%, adding it expected inflationary pressure to ease in the second half. Central bank Governor Yang Chin-long has said a rate cut would most likely come when CPI fell under 1.5%.

S. KOREA (BBG): South Korea Plans $22 Billion Extra Budget as Tariffs Hit Growth

South Korea unveiled an extra budget worth billions of dollars, in a bid to support an economy struggling with sluggish consumption and mounting trade headwinds from Donald Trump’s tariffs. The 30.5 trillion won ($22.2 billion) proposal includes 15.2 trillion won for economic stimulus and 5 trillion won for supporting livelihoods like small businesses, the finance ministry said in a statement. Another 10.3 trillion won is set aside to cover revenue shortfall for this year’s existing budget, as taxation income fell due to weaker corporate performance and consumer spending.

DATA

AUSTRALAIA DATA (MNI): Unemployment at 4.1% in May, Employment Weak

- AUSTRALIA MAY UNEMPLOYMENT RATE +4.1%

- AUSTRALIA MAY LABOR PARTICIPATION RATE +67%

- AUSTRALIA MAY EMPLOYED PERSONS CHANGE -2.5K

- AUSTRALIA MAY F-T EMPLOYED PERSONS CHANGE 38.7K

Australia’s unemployment rate in May printed at 4.1%, unchanged from April and inline with expectations, while employment contracted by 2,500, below the 21,000 roles expected and down from April’s 89,000 result, data from the Australian Bureau of Statistics showed Thursday. "Despite employment falling by 2,000 people this month, it’s up 2.3% compared to May 2024, which is stronger than the pre-pandemic, 10-year average annual growth of 1.7%,” said Sean Crick, head of labour statistics at the ABS. "This fall in employment, combined with a drop in unemployment of 3,000 people, meant that the unemployment rate remained steady at 4.1% for May."

NEW ZEALAND (MNI): New Zealand GDP Grows 0.8% Q/Q

The New Zealand economy grew 0.8% q/q in Q1, 10 basis points higher than the previous quarter, data from Stats NZ showed Thursday. The print was also 10bp higher than market expectations. The economy shrunk 0.7% on a yearly basis. “Expenditure on GDP rose 0.9% in the March 2025 quarter, following a 0.6% rise in the December 2024 quarter," Stats NZ noted. "Expenditure on GDP fell 0.9% over the year ended March 2025 compared with the year ended March 2024.”

FOREX: USD Index Tops Trendline; Surprise Norway Cut Hits NOK

- NOK is sliding against all others in G10 on the back of a surprise 25bps rate cut from the Norwegian central bank. The decision itself was coupled by a larger-than-forecast downward revision to the MPR rate path, adding additional pressure to the currency. EURNOK rallied to meet resistance at the 50-day EMA of 11.5921, but has faded somewhat toward the NY crossover.

- The greenback is furtively firmer against all others in G10, helping the USD Index edge to new weekly highs headed through the European open. Much of this USD strength being based off renewed geopolitical risk on the building expectation that US officials are preparing for a possible strike on Iran "in the coming days" - a move that could prompt retaliation against US assets in the region.

- What's notable about this USD rally is that it's triggered a bullish signal for the DXY via a break and possible close above the downtrendline drawn off the early February high. This trendline has helped define the dollar weakness across Trump's administration, and this week's move raises the risk of a correction higher in the near-term.

- Following USDJPY's initial drop on the FOMC's unchanged median dot for 2025, the pair once again found decent demand in the 1.4435/40 area. Subsequently, USDJPY has traded steadily higher towards the top end of the recent range, narrowing the gap to last week's highs at 145.46, a level that continues to cap the topside this week.

- This puts the 50-dma into contention at 99.512, with the 23.6% retracement above at 100.50. Outside of the USD Index, Antipodean currencies look particularly prone to a possible correction lower: NZD/USD has broken back below 0.60, while AUD/USD has met support at 0.6461, the uptrendline drawn off the mid-May low.

- The Bank of England rate decision is up next, with markets expecting no change from the MPC today. The vote split will be of market interest in addition to the use of language around "cautious" and "gradual" descriptors for the easing cycle.

- US data are few and far between Thursday, with the US on market holiday for Juneteenth.

BONDS: Off Lows, Early London Bear Steepening Intact on Middle East & Fed

Core global FI markets off lows, with the rally in crude oil stalling and EGB supply digested smoothly.

- ECB speak has generally reaffirmed the Bank’s data-dependent approach, with GC member Villeroy indicating the potential for a rate cut further down the line.

- FI markets were subjected to some selling pressure in early London trade, as European participants reacted to yesterday’s FOMC decision and ongoing tension in the Middle East.

- Bund futures last -29 at 130.87 vs. lows of 130.73.

- The contract continues to trade below the Jun 13 high. Key short-term support to watch lies at 130.12.

- German yields 2-3bp higher, curve steeper. 2s10s and 5s30s stick within recent ranges.

- EGB spreads to Bunds little changed to wider (SPGBs flat, OATs +1bp, BTPs +1.5bp, GGBs +2bp) with equities lower.

- Gilt futures -30 at 92.76 vs. lows of 92.56.

- Initial support and resistance located at the 20-day EMA (92.25) & a Fibonacci level (93.13), respectively.

- Yields 1.5-4.0bp higher, curve steeper. Multi-week ranges in benchmark yields and major curves intact.

- BoE-dated OIS little changed on the day, essentially showing 0 odds of a move today, 19bp cuts through August, 24bp through September, 39bp through November and 47bp through year-end.

- We continue to lean towards a cut in August, risks to market pricing may be skewed a little dovishly given the recent evolution of data.

EQUITIES: Eurostoxx 50 Futures Continue to Trade at Their Recent Lows

Eurostoxx 50 futures continue to trade at their recent lows. The latest pullback has resulted in a breach of the 50-day EMA at 5297.44. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would signal a short-term top and highlight scope for a deeper retracement. This would open 5178.00, the May 6 low, and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5347.51, the 20-day EMA. The trend condition in S&P E-Minis remains bullish. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6006.73, the 20-day EMA. A clear breach of this average would suggest potential for a deeper retracement and expose the 50-day EMA, at 5902.27. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

- Japan's NIKKEI closed lower by 396.81 pts or -1.02% at 38488.34 and the TOPIX ended 16.27 pts lower or -0.58% at 2792.08.

- Elsewhere, in China the SHANGHAI closed lower by 26.701 pts or -0.79% at 3362.108 and the HANG SENG ended 472.95 pts lower or -1.99% at 23237.74.

- Across Europe, Germany's DAX trades lower by 117.48 pts or -0.5% at 23200.33, FTSE 100 lower by 32.93 pts or -0.37% at 8810.56, CAC 40 down 52.78 pts or -0.69% at 7603.34 and Euro Stoxx 50 down 35.36 pts or -0.67% at 5231.55.

- Dow Jones mini down 181 pts or -0.43% at 42007, S&P 500 mini down 25.75 pts or -0.43% at 5955.5, NASDAQ mini down 112.25 pts or -0.52% at 21608.

Time: 09:50 BST

COMMODITIES: Medium-Term Trend Signals for Gold Remain Bullish

WTI futures traded sharply higher last week and last Friday’s early rally marked an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted $67.11, the Jun 13 low. A breach of this level would signal scope for a deeper retracement. A bullish theme in Gold remains intact and short-term weakness is considered corrective. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3275.5, the 50-day EMA.

- WTI Crude up $0.65 or +0.87% at $75.79

- Natural Gas down $0.01 or -0.3% at $3.978

- Gold spot up $1.12 or +0.03% at $3370.41

- Copper down $4.2 or -0.86% at $486.6

- Silver down $0.33 or -0.9% at $36.4038

- Platinum down $24.77 or -1.87% at $1296.58

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 19/06/2025 | 0945/1145 | ECB de Guindos On Eurozone Economic Outlook | ||

| 19/06/2025 | 1030/1230 | ECB Lagarde Keynote Speech At Economic Integration Conference | ||

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | - | ECB Cipollone At Eurogroup Meeting | ||

| 19/06/2025 | 1600/1800 | ECB Lagarde At Financi'Elles event | ||

| 20/06/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 20/06/2025 | 2330/0830 | *** | CPI | |

| 20/06/2025 | 0600/0700 | *** | Public Sector Finances | |

| 20/06/2025 | 0600/0700 | *** | Retail Sales | |

| 20/06/2025 | 0600/0800 | ** | PPI | |

| 20/06/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 20/06/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 20/06/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 20/06/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 20/06/2025 | 1230/0830 | ** | Retail Trade | |

| 20/06/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/06/2025 | 1530/1630 | BOE to announce Q3 APF sales schedule | ||

| 20/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 20/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |