MNI US OPEN - US Govt Shutdown Becomes Longest in History

EXECUTIVE SUMMARY

- SENATE DEMOCRATS DEBATE PATH TO ENDING GOVERNMENT SHUTDOWN: WaPo

- MAMDANI MAKES HISTORY WITH DECISIVE WIN IN NYC MAYORAL RACE

- RIKSBANK HOLDS IN NOV, FORESEES PROLONGED PAUSE

- MORE THAN TWO BOJ MEMBERS POSITIVE ON HIKE

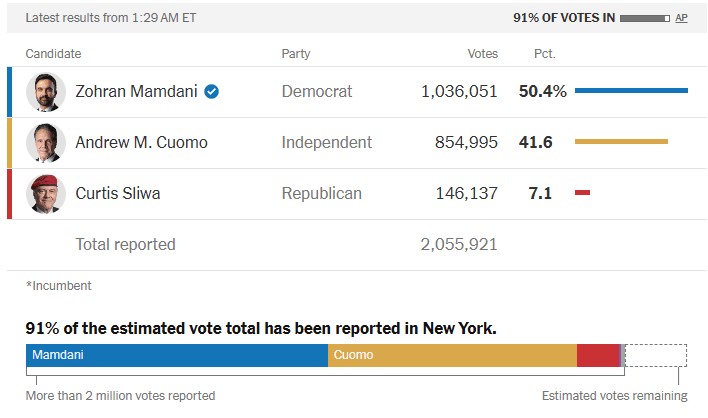

Figure 1: New York mayoral election votes

Source: NYT

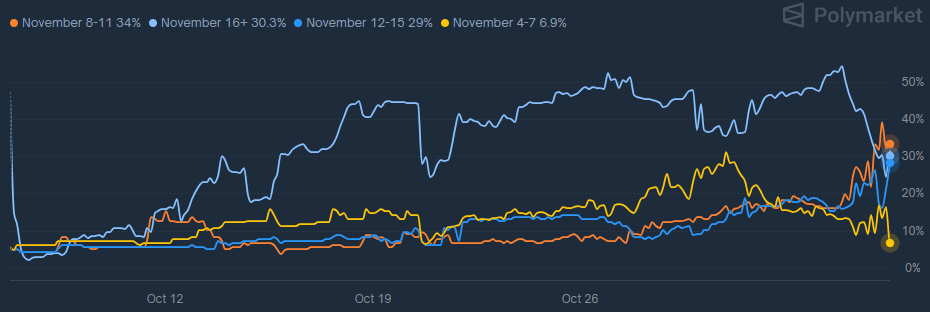

Figure 2: Betting market odds surge to imply ~70% odds of US gov shutdown ending by Nov 15

Source: Polymarket

NEWS

US (MNI): Strong Election Day Performance Tempers Optimism of Shutdown Resolution

Its Day 36 of the US government shutdown, officially the longest shutdown in US history. Yesterday, the Senate rejected the House-passed November 21 funding bill for a 14th time. However, there is increased optimism of an offramp following an acceleration of bipartisan talks on an emerging deal to end the impasse. Punchbowl reports there are now 'more than a dozen Senate Democrats' engaging with Republicans on reopening the government. In response, the most likely end date of the shutdown has been revised down from November 29 to November 13, per Polymarket.

US (WaPo): Senate Democrats Debate Path to Ending Government Shutdown

A handful of moderate Senate Democrats are considering voting to end what has now become the country's longest government shutdown, splitting the caucus as some colleagues to their left urge them to hold out. A bipartisan group of senators is working to craft a deal in which Congress would pass three full-year appropriations bills to fund some agencies, along with a short-term bill that would reopen the rest of the government, according to four people familiar with the talks, who spoke on the condition of anonymity to describe private discussions. In exchange, Senate Republicans would agree to hold a vote at a set date on extending Affordable Care Act subsidies that are otherwise slated to expire.

US (BBG): Mamdani Makes History With Decisive Win in NYC Mayoral Race

Zohran Mamdani was elected the 111th mayor of New York in a historic victory that will put an avowed democratic socialist in charge of the city that serves as the capital of global finance. Mamdani, a Democrat, received 50.4% of the votes, while former Governor Andrew Cuomo, running on an independent line after his loss to Mamdani in the primary, garnered 41.6% with 98% of the vote counted. Republican Curtis Sliwa got 7.1%.

US (BBG): California Passes New House Maps in Triumph for Newsom

California voters passed a ballot measure that could flip as many as five congressional seats to Democrats from Republicans, handing Governor Gavin Newsom a major political victory in his fight against President Donald Trump. Proposition 50 was backed by about 65% of voters, with nearly half of precincts reported. The Associated Press called the outcome within a minute of polls closing.

US (BBG): Virginia, New Jersey Wins Fuel Democrats 2026 Comeback Hopes

Democrats reclaimed political momentum Tuesday with gubernatorial victories in Virginia and New Jersey, early signs that voter unease with the economy in President Donald Trump’s second term could give them a path to winning control of Congress next year. Abigail Spanberger’s comfortable win in the Virginia governor’s race Tuesday, and Mikie Sherrill’s in New Jersey, gave Democrats their biggest electoral triumphs since Trump’s return to power.

US/CHINA (BBG): China Ends Levies on US Farm Goods After Fentanyl Duties Cut

China will remove retaliatory tariffs that it imposed on a range of US agricultural products, after Washington halved its fentanyl-related levies on Chinese goods. The country’s Ministry of Finance confirmed in a notice on Wednesday that it will end all tariffs imposed March 4 on soybeans and other US agricultural products including corn, wheat, sorghum and chicken. The move was previously flagged in a White House fact sheet.

RIKSBANK (MNI): Riksbank Holds in Nov, Foresees Prolonged Pause

Riksbank left its policy rate on hold at 1.75% at its November meeting and stated that the economy had evolved largely as anticipated, with its September forecast for a prolonged policy pause holding good. The Executive Board stated that the latest data supported its view that recent elevated inflation was transitory, that there were signs of growth picking up and that the policy rate "is expected to remain at this (1.75%) level for some time to come." November is an interim meeting, with no new forecast round and the Board's economic assessment was that there had been no major changes to the outlook.

UK (MNI): UK Needs GBP50 Billion Fiscal Consolidation - NIESR

A fiscal consolidation of GBP50 billion should be in UK Chancellor of the Exchequer Rachel Reeves' budget on Nov 26, the National Institute of Economic and Social Research said on Wednesday, in order to build a headroom of one to one-and-a-half percent of GDP. "A buffer of at least GBP30 billion" is needed to "avoid a cycle of repeated fiscal resets," NIESR Director David Aikman said, after Reeves only met her fiscal rules by GBP10 billion of headroom in her budget in March.

EU (BBG): EU Nations Seal Deal on 2040 Climate Goal to Cut 90% Emissions

European Union member states sealed a deal to reduce emissions by 90% through 2040 compared with 1990 levels, a move that bolsters the bloc’s climate leadership credentials ahead of the COP30 summit. The agreement was announced by Denmark, holder of the EU’s rotating presidency, after marathon talks among environment ministers that started on Tuesday morning in Brussels and culminated on Wednesday.

BOJ (MNI): More Than Two Members Positive on Hike - BOJ Minutes

One Bank of Japan board member, apart from the two who proposed raising the policy rate to 0.75%, said it was time to consider another increase as more than six months had passed since the last hike, minutes of the Sept 18-19 meeting showed Wednesday. However, the member noted that uncertainty remained over the pace of the U.S. economic slowdown and said it was appropriate for the Bank to maintain its current policy stance for the time being. Two other members said they were positively considering a rate hike, though not immediately.

JAPAN (BBG): Japan’s Mimura Sees Some Yen Moves Deviating From Fundamentals

Recent moves by the yen are deviating from economic fundamentals when interest rate differentials are taken into account, Japan’s top currency official said Wednesday. “Basically we always say you should look at interest rate differentials between yen and the dollar,” and the currency pair should move in line with the gap, Atsushi Mimura, Vice Finance Minister for International Affairs, said. “If you look at the actual movement of foreign exchange and the moves of differentials between US and Japan interest rates on public bonds, you do see some sort of deviation recently, I would say.”

CHINA (BBG): China’s Premier Woos Global Firms With $24 Trillion GDP Vow

Chinese Premier Li Qiang suggested his country’s economy will maintain its current growth pace, touting China as an attractive market for global companies as Beijing seeks to mitigate concerns over its trade imbalances. Li said gross domestic product is expected to surpass 170 trillion yuan ($23.9 trillion) in five years, implying an average annual growth rate of about 4% through 2030 without adjusting for price changes. That’s in line with the nominal GDP growth reported so far this year.

CHINA (BBG): PBOC Plans Second Reverse Repo Round to Support Liquidity - Paper

Chinese central bank will conduct a second round of outright reverse repurchase operations this month to maintain ample market liquidity and further support government bond issuances and guide financial institutions to increase credit lending, Shanghai Securities News reported, citing analysts.

CHINA (MNI INTERVIEW): PBOC to Boost Tech Loans Via Structural Tools

An advisor shares his view on the PBOC's funding of tech firms. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CENTRAL BANK PREVIEW

MNI NORGES BANK PREVIEW: Steady Rates, Steady Guidance

Norges Bank is unanimously expected to hold the deposit rate at 4.00% on Thursday. The November decision will not be accompanied by an updated MPR or rate path projection, only a concise Monetary Policy Assessment. Norges Bank rarely makes meaningful policy rate or guidance pivots at these interim meetings, so the base case is for a short policy statement with no new signals.

MNI NBP PREVIEW: Cut on Cards After Soft CPI Print

The November meeting may be the last chance for the NBP to cut interest rates this year as an unwritten local convention dictates that the MPC sits on its hands in December. Although recent communications signalled continued vigilance amid lingering inflationary risks, another dovish CPI reading prompted a realignment of market consensus around a 25bp rate reduction. We too are inclined to think that the MPC will deliver an opportunistic cut before taking the next couple of months to reconsider its stance.

MNI BCB PREVIEW: Prolonged Pause Still Required

The Copom is widely expected to leave the Selic rate unchanged at 15.00% for a third consecutive meeting on Wednesday, as the committee maintains its hawkish stance to rein in unanchored inflation expectations. Though inflation and inflation expectations have been declining gradually, they remain above target and officials have continued to reiterate their high for longer messaging recently. Nonetheless, with activity showing some further signs of softening as well, focus will be on the forward guidance and whether there are any signals for a possible rate cut in the near future.

MNI BANXICO PREVIEW: Majority to Maintain Easing Bias

Banxico is expected to deliver another 25bp rate cut on Thursday, bringing the overnight target rate down to 7.25%. Although core inflation remains stuck above the ceiling of the 2-4% target range, the majority of the Board continues to place more emphasis on the weakness of economic activity. Nonetheless, the vote is likely to be split once again, with Deputy Governor Heath continuing to focus on the stalling of the core disinflation process. Focus will therefore remain on the forward guidance, which is likely to keep the door open to further easing ahead given the backdrop of Fed rate cuts and a resilient Mexican peso.

MNI BNM PREVIEW: BNM on Hold as Easing Cycle Ends

Growth in Malaysia remains underpinned by resilient domestic demand, strong employment and wage growth. Exports rebounded strongly in the September data, and have been surprisingly resilient for much of 2025 supported by the electronics upcycle. Malaysia has seen moderating inflation for most of this year, causing the Central Bank to reduce inflation forecast ranges. The CPI for September result of +1.5% is the first time CPI YoY has printed in line with the bottom end of the new range since the beginning of the year.

DATA

EUROZONE DATA (MNI): Growth Momentum Improving Everywhere in Oct PMIs Except France

- EUROZONE OCT FINAL SERV PMI 53.0 (52.6 FLASH, 51.3 SEP)

- EUROZONE OCT FINAL COMPOSITE PMI 52.5 (52.2 FLASH, 51.2 SEP)

- GERMANY OCT FINAL SERV PMI 54.6 (54.5 FLASH, 51.5 SEP)

- FRANCE OCT FINAL SERV PMI 48.0 (47.1 FLASH, 48.5 SEP)

The October PMI round signalled a positive start to Eurozone growth momentum in Q4. With Q3 flash GDP having already printed above the ECB's September projections, the case for unchanged policy rates going forward is growing. However, some ECB officials remain cognisant of downside risks heading into 2026. Following upward revisions in France and Germany, and stronger-than-expected readings in Italy and Spain, the Eurozone services PMI was revised up to 53.0 (vs 52.6 flash, 51.3 prior). With the manufacturing PMI confirming flash estimates at 50.0 on Monday, this left the composite reading at a 29-month high of 52.5.

EUROZONE DATA (MNI): Latest ECB Wage Tracker Signals Easing Compensation Pressures

There were marginal upward revisions to the ECB's latest forward-looking wage tracker relative to the September iteration, but the general conclusion that compensation pressures are expected to ease in the coming year remains intact. Negotiated wages excluding one-off payments are expected at 3.15% Y/Y in Q4 2025, up from 3.13% in September. Employee coverage in Q4 2025 is now 47%, up from 46% previously.

EUROZONE SEP PPI -0.1% M/M, -0.2% Y/Y (VS -0.4% M/M, -0.6% Y/Y AUG)

ITALY DATA (MNI): New Business Inflows Rise to 1.5 Year High in October Services PMI

- ITALY OCT SERV PMI 54.0 (53.0 FCAST, 52.5 SEP)

- ITALY OCT COMP PMI 53.1 (52.1 FCAST, 51.7 SEP)

Italy (as Spain earlier) came in stronger than expected at 54.0 (53.0 cons; 52.5 prior). Growth in new work was a key driver, supported by a fresh rise in exports. Key highlights: "Both output and new business increased at sharp and accelerated paces. Notably, October saw an end to the trend of decline in exports, with the volume new business from abroad up slightly on the month." On the higher exports: "Some panellists noted higher sales from European customers, but there were also reports of persistent international uncertainty."

SPAIN DATA (MNI): More Solid Domestic Demand Signals in October PMI Round

- SPAIN OCT SERV PMI 56.6 (54.5 FCAST, 54.3 SEP)

- SPAIN OCT COMP PMI 56.0 (54.3 FCAST, 53.8 SEP)

Spanish domestic demand remains solid according to the October PMI round, with today's stronger-than-expected services reading building on the signals from Monday's manufacturing print. The services and composite readings reached year-to-date highs in October

UK DATA (MNI): Upward Revision to Oct Services PMI, But Fall in Employment Still Noted

- UK OCT FINAL SERV PMI 52.3 (51.1 FLASH, 50.8 SEP)

- UK OCT FINAL COMPOSITE PMI 52.2 (51.1 FLASH, 50.1 SEP)

Momentum in UK services activity remains positive, though October's 52.3 final read remains below August's 54.2. While stronger new orders supported the aggregate index, another reduction in employment numbers and easing output charge inflation will be noted by the BOE. Key notes from the UK services PMI release: "Survey respondents cited a gradual turnaround in new work and sales opportunities, despite elevated business uncertainty and delayed decision-making among clients"

GERMANY DATA (MNI): Factory Orders Recover a Little in September

- GERMANY SEP FACTORY ORDERS +1.1% M/M (VS -0.4% AUG)

German factory orders were a little stronger than expected in September, at 1.1% M/M amid an August upward revision to -0.4% (-0.8% unrevised). By itself, September represents some recovery in the series but not a material one considering index levels continue to print not far off cycle lows. "When large-scale orders are excluded, new orders were 1.9% higher than in the previous month. The less volatile three-month on three-month comparison showed that new orders were 3.0% lower in the 3rd quarter of 2025 than in the 2nd quarter; when large-scale orders are excluded, new orders were down 1.5%", Destatis comments.

FRANCE DATA (MNI): Strong France IP Driven by Transport Equipment, Amid Revisions

- FRANCE SEP IND PROD +0.8% M/M, +1.3% Y/Y (VS -0.9% M/M, +0.1% Y/Y AUG)

French industrial production for September came in firmer than expected at 0.76% M/M (0.1% Bloomberg consensus) as it recovered after an weaker August than first thought with -0.9% M/M. Manufacturing output also increased 0.9% M/M (vs -1.0% August, downwardly revised from -0.7%). Looking at the details, transport equipment rebounded strongly (5.5% M/M vs -4.3% prior), "following the lead of the aerospace industry, which, since June, has been the sector contributing most to chances in manufacturing output", notes INSEE.

NEW ZEALAND DATA (MNI): New Zealand Unemployment 5.3% in Q3

New Zealand’s unemployment rate rose 10 basis points to 5.3% in the third quarter, in line with expectations, Stats NZ data showed Wednesday. The underutilisation rate edged up to 12.9% from 12.8%, while the employment rate eased to 66.6% from 66.8%. All salary and wage rates, including overtime, increased 2.1% on quarter. Average weekly earnings for full-time equivalent employees rose to NZD1,688 from NZD1,621, while average ordinary-time hourly earnings climbed to NZD43.60 from NZD41.98.

FOREX: USD Remains on Front-Foot, DXY Testing August Highs

- After some moderate weakness during the APAC session, the US dollar has reversed back to recovery highs, keeping the post-FOMC topside momentum firmly intact. Gains today for the DXY would represent a sixth consecutive winning session, as the index currently flirts with the August highs, a break of which would represent 5-month highs.

- The most notable price action overnight was for USDJPY, which had a sharp selloff to 152.96, as the risk off sentiment across global markets initially extended. Assisting the yen rally was the BOJ minutes, where one board member, apart from the two dissenters, said it was time to consider another hike. Subsequently, risk stabilised and provided a more supportive tone for USDJPY, which has risen to a session high of 153.84 ahead of the NY crossover.

- In line with the broader greenback advance, USDCAD is also on a 5-session winning streak, currently trading at 6-month highs. Canada yesterday budgeted its biggest ever cash deficit this fiscal year, excluding the pandemic, on a fiscal push to revitalize sluggish growth in the country. This week’s extension of USDCAD highlights a clear reversal of the corrective bear leg between Oct 14 - 29. Spot is currently testing 1.4136, the top of a bull channel drawn from the Jul 23 low. Above here, 1.4167 is the next level of note, the 50.0% retracement of the Feb 3 - Jun 16 bear leg.

- GBPUSD remains in focus following its pronounced downtrend since mid-September. The pair remains close to cycle lows today as markets digest Chancellor Reeves’ speech on Tuesday hinting at tax increases, and await tomorrow's BoE MPC decision, set to be a close decision between a hold and a 25bp cut. Following the break of 1.3041, sights are on 1.2971 next, a Fibonacci projection point. Note that the trend is in oversold territory and a recovery would allow this condition to unwind. Initial resistance is at 1.3142, the Aug 1 low.

- ISM services highlights today's data calendar. A set of ECB speakers including Schnabel are scheduled over the next couple of days, while we will also hear from SNB's Tschudin today.

EGBS: Bund Futures Continue to Consolidate Above Key Support Zone

- The early risk-off inspired bid in Bund futures has faded, but RXZ5 remains above the 129.13 support area (aligning with the 50-day EMA and October 13 low). Futures are currently -2 ticks at 129.27, with solid results at today's 15-year Bund auction helping the contract away from session lows of 129.22.

- German yields are up to 1bp lower across the curve.

- Alongside the German supply, Italy held a E5bln buyback transaction.

- 10-year EGB spreads to Bunds are up to 1bp wider on the session, with global equity sentiment still relatively weak.

- Following upward revisions in France and Germany, and stronger-than-expected readings in Italy and Spain, the Eurozone services PMI was revised up to 53.0 (vs 52.6 flash, 51.3 prior). With the manufacturing PMI confirming flash estimates at 50.0 on Monday, this left the composite reading at a 29-month high of 52.5.

- There were marginal upward revisions to the ECB's latest forward-looking wage tracker relative to the September iteration, but the general conclusion that compensation pressures are expected to ease in the coming year remains intact.

- ECB’s Kocher is scheduled to speak on “Negative Rates and the Effective Lower Bound” later today.

GILTS: Lower But Recent Ranges Intact

Gilts trade around session lows with a recovery from overnight lows in equity benchmarks, a firmer-than-flash final services PMI release and source reports pointing to some potential movement to end the U.S. government shutdown applying pressure.

- Futures through yesterday’s low, last -22 at 93.44.

- Monday’s base (93.32) untested, bulls remain in technical control.

- Yields now ~0.5bp higher across the curve.

- Only 30s managed to pierce their October yield low during yesterday’s rally.

- SONIA futures now 0.5-3.0 lower alongside the pressure in the long end.

- The bulk of the focus remains split between tomorrow’s BoE decision and local fiscal matters.

- On the former, we have characterised our view as 50/50 (when it comes to a cut or a hold), which is more dovish than current market pricing (~6bp of easing).

- We would have more confidence in a cut if the Budget was not coming into view, particularly given the soft food CPI reading in the latest monthly inflation release.

- Our full preview of the decision will be published later today.

- Elsewhere, the NIESR has suggested that the Budget should include GBP50bln of fiscal consolidation, with the aim of building fiscal headroom of ~1.5% of GDP.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.908 | -6.2 |

Dec-25 | 3.809 | -16.0 |

Feb-26 | 3.675 | -29.4 |

Mar-26 | 3.613 | -35.6 |

Apr-26 | 3.504 | -46.6 |

Jun-26 | 3.474 | -49.5 |

Jul-26 | 3.414 | -55.6 |

Sep-26 | 3.401 | -56.9 |

EQUITIES: E-Mini S&P Remains Above Key Pivot Support at 50-Day EMA

Recent weakness in Eurostoxx 50 futures appears to have been corrective. The contract has found support ahead of the 50-day EMA, at 5571.03. Support below the EMA lies at 5555.00, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Sights are on resistance and the bull trigger at 5742.00, the Oct 29 high. The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Support at the 20-day EMA, at 6803.81, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6702.18 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- Japan's NIKKEI closed lower by 1284.93 pts or -2.5% at 50212.27 and the TOPIX ended 41.85 pts lower or -1.26% at 3268.29.

- Elsewhere, in China the SHANGHAI closed higher by 9.062 pts or +0.23% at 3969.248 and the HANG SENG ended 16.99 pts lower or -0.07% at 25935.41.

- Across Europe, Germany's DAX trades lower by 157.28 pts or -0.66% at 23791.83, FTSE 100 lower by 11.07 pts or -0.11% at 9703.96, CAC 40 down 17.23 pts or -0.21% at 8050.3 and Euro Stoxx 50 down 33.89 pts or -0.6% at 5626.31.

- Dow Jones mini up 13 pts or +0.03% at 47227, S&P 500 mini down 11.25 pts or -0.17% at 6790.5, NASDAQ mini down 81 pts or -0.32% at 25494.25.

Time: 10:00 BST

COMMODITIES: Gold Off Week's Lows, But Shy of Initial Resistance at $4161.40

WTI futures are unchanged and the contract remains in a corrective cycle for now. Note that price has recently traded through the 50-day EMA, currently at $61.03. The breach of this EMA signals scope for a stronger recovery. Note too that a resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low. A fresh cycle low last week in Gold highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3867.3. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

- WTI Crude up $0.3 or +0.5% at $60.88

- Natural Gas down $0.12 or -2.65% at $4.228

- Gold spot up $38.19 or +0.97% at $3971.07

- Copper down $1.75 or -0.35% at $493.05

- Silver up $0.63 or +1.33% at $47.7921

- Platinum down $0.59 or -0.04% at $1539.74

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 05/11/2025 | 1445/0945 | *** | S&P Global Services Index (f) | |

| 05/11/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 05/11/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 05/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 05/11/2025 | 1610/1610 | BOE Breeden At SALT Blockchain Event | ||

| 06/11/2025 | 2330/0830 | ** | Average Wages (p) | |

| 06/11/2025 | - | NorgesBank Meeting | ||

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 06/11/2025 | 0030/1130 | ** | Trade Balance | |

| 06/11/2025 | 0700/0800 | ** | Industrial Production | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0800/0900 | ** | Industrial Production | |

| 06/11/2025 | 0800/0900 | ** | Unemployment | |

| 06/11/2025 | 0810/0910 | ECB Schnabel at ECB Money Market Conference | ||

| 06/11/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/11/2025 | 0830/0930 | ECB De Guindos on Natixis Webinar | ||

| 06/11/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 06/11/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/11/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 06/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 06/11/2025 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 06/11/2025 | 1400/1400 | Decision Maker Panel Data | ||

| 06/11/2025 | 1500/1000 | * | Ivey PMI | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 06/11/2025 | 1530/1030 | BOC Governor Macklem testifies at Senate | ||

| 06/11/2025 | 1600/1100 | NY Fed's John Williams | ||

| 06/11/2025 | 1600/1100 | Fed Governor Michael Barr | ||

| 06/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 06/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 06/11/2025 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 06/11/2025 | 1830/1930 | ECB Lane at IMF Conference | ||

| 06/11/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/11/2025 | 2030/1530 | Fed Governor Christopher Waller | ||

| 06/11/2025 | 2130/1630 | Philly Fed's Anna Paulson | ||

| 06/11/2025 | 2230/1730 | St. Louis Fed's Alberto Musalem | ||

| 07/11/2025 | 2330/0830 | ** | Household Spending |

Note: Due to U.S. government shutdown, some data may be unavailable.