EUROZONE DATA: Latest ECB Wage Tracker Signals Easing Compensation Pressures

Nov-05 09:20

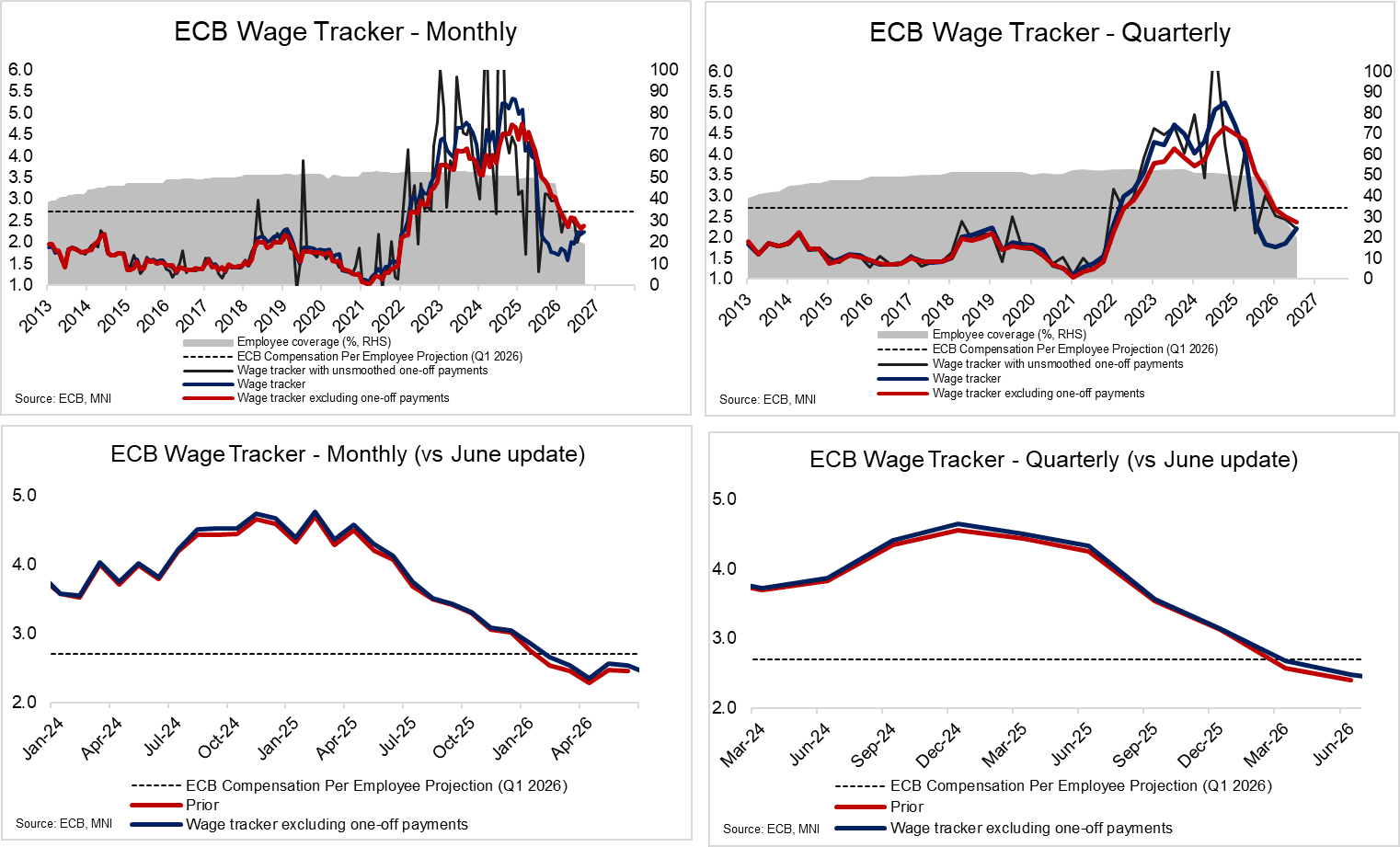

There were marginal upward revisions to the ECB’s latest forward-looking wage tracker relative to the September iteration, but the general conclusion that compensation pressures are expected to ease in the coming year remains intact.

- Negotiated wages excluding one-off payments are expected at 3.15% Y/Y in Q4 2025, up from 3.13% in September. Employee coverage in Q4 2025 is now 47%, up from 46% previously.

- The tracker now includes data for Q3 2026. Wages excluding one-off payments are seen at 2.37% Y/Y, down from an expected 2.49% Y/Y in Q2 2026. Note however that employee coverage remains very low for these quarters – just 27% for Q2 and 19% for Q3.

- Note that since the wage tracker has started being published by the ECB, we have generally seen marginal upward revisions over time.

- In the ECB’s October press conference, President Lagarde noted that “Indicators of underlying inflation remain consistent with our two per cent medium-term target. While firms’ profits are recovering, labour costs are set to moderate further owing to rising productivity and an easing in wage growth. Forward-looking indicators, such as the ECB’s wage tracker and surveys on wage expectations, point to slower wage growth over the remainder of the year and the first half of 2026”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Call Spread Buyer

Oct-06 09:17

SFIH6 96.55/96.65cs, bought for 1 in 7.78k.

FRANCE: Oct.13 Budget Draft Deadline Looms w/No Clear Route To Functional Govt

Oct-06 09:12

French Minister for Public Accounts Amélie de Montchalin warned in an interview with Le Monde last month that the government must submit a draft budget to parliament by October 13 or enact a special law to avoid a shutdown, as it will no longer be possible to pass a budget by January 1.

- De Montchalin said a special law was used earlier this year, “There was no catastrophe because it only lasted six weeks.” However, she added, “France cannot go an entire year without a budget: It's a context in which revenues and expenditures are frozen. Political choices and priorities would give way to a purely accounting form of management.”

- According to de Montchalin, France cannot operate under special accounting, “because, in 2026, we need to allocate €8 billion more to paying interest on the debt. Without an approved budget, those €8 billion would have to be found elsewhere, in a top-down manner, without a debate in Parliament.”

- The resignation of Prime Minister Sébastien Lecornu has left President Emmanuel Macron with no obvious route to restoring the stability required to pass a budget, with any successor likely to encounter the same resistance from both the left and right in parliament.

- Emmanuel Cau, head of European equities strategy at Barclays, “The only way to stop this crisis is to have a new election. It’s making Europe hard to invest in and creating an excuse for investors to tread carefully… The market has to think about the far right being in a position to capitalise.”

- Jordan Bardella, president of the far-right Rassemblement National, said this morning. “We have no other possibility but to return to the French people because, once again, the longer we wait, the more we play with the stability of the country...”

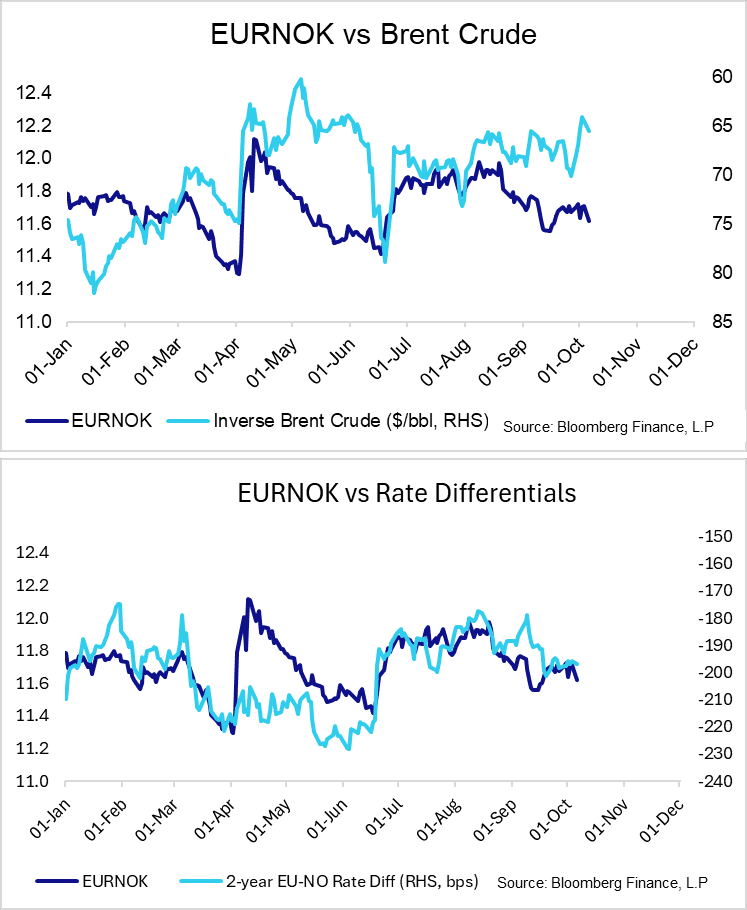

NOK: Outperforming G10 Basket On Commodity Strength; Sep CPI This Week

Oct-06 09:05

- NOK outperforms the G10 basket this morning, trading off strength in Brent crude and natural gas futures. EURNOK is down 0.78% at 11.6171, just off session lows of 11.6059.

- The cross has narrowed the gap to 11.6000, which has historically been an important pivot level going back to 2023. Better support meanwhile is seen at 11.5387, the September 15 low.

- Crude’s ~1.6% rise appears to be a relief rally following OPEC’s decision to increase November’s output by 137kb/d (in line with October’s rise), against risks of a larger move. Meanwhile, cooler October weather forecasts have supported TTF futures, according to our commodities team.

- This week’s Norwegian calendar is headlined by the September inflation report on Friday. Early consensus expects CPI-ATE steady at 3.1% Y/Y, a touch below Norges Bank’s 3.2% projection in the September MPR.

- Following Norges Bank’s hawkish September cut, the risk in the coming months is likely tilted towards more – not less – easing. However, this will require a faster pullback in underlying inflation and a larger degree of economic slack than is currently being observed.

- Danske Bank believe that “short-term monetary policy setting is not the key determinant for the attractiveness of being invested in NOK and SEK” at the current juncture. Instead, they think Scandi longs “look like a play on the direction of USD real rates and the Goldilocks-narrative [i.e. “Fed rate cuts on weaker but not recessionary labour market data”]”. They continue to favour a long EURNOK bias for now, but caution that "if risk continues to rally in the coming week we will contemplate closing down the position and wait for better entry levels".