MNI US OPEN - Trump to Host Tech and Business Leaders

EXECUTIVE SUMMARY

- TRUMP TO HOST TECH AND BUSINESS LEADERS AT WHITE HOUSE

- JAPAN, US NEAR DEAL TO BRING LOWER AUTO TARIFFS INTO EFFECT: RTRS

- CHINA EYES CURBS ON STOCK SPECULATION TO FOSTER STEADY GAINS: BBG

- SWISS CPI REMAINS UNCHANGED; SNB SEPTEMBER CUT UNLIKELY

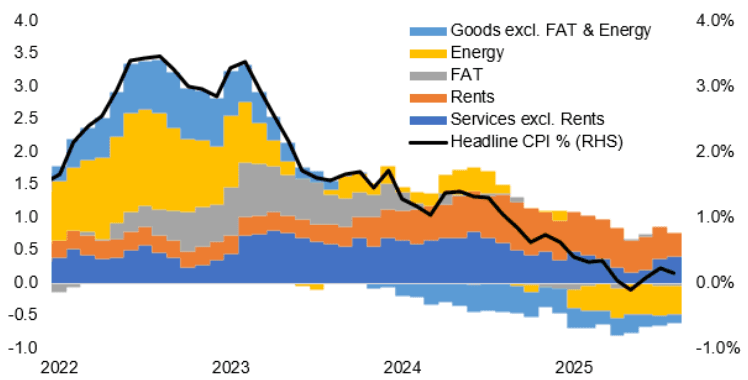

Figure 1: Swiss CPI inflation contributions pp Y/Y

Source: MNI/Federal Statistical Office

NEWS

MNI US PAYROLLS PREVIEW: Slack Metrics Eyed With Risks Rising

Nonfarm payrolls growth is seen at 75k in August (sa) per the broad Bloomberg survey, after 73k in July. Revisions are going to be particular focus after last month’s huge downward revisions heavily altered recent trends, with non-health private payrolls growth at best stalling for the past three months, and dominated the market reaction. The median primary dealer analyst eyes 70k whilst the Bloomberg whisper currently sits at 83k but with the ADP report still to come after publication of this preview.

US (MNI): Trump to Host Tech and Business Leaders at White House

US President Donald Trump is expected to host around two dozen tech and business leaders for an event in the newly-renovated White House Rose Garden at 19:30 ET 00:30 BST. According to an invite list, attendees include Meta founder Mark Zuckerberg, Apple CEO Tim Cook, Microsoft founder Bill Gates, and OpenAI founder Sam Altman. Former Trump advisor Elon Musk is not on the invite list. The dinner will follow an AI event in the White House hosted by First Lady Melania Trump.

US (BBG): Trump Asks US Supreme Court to Uphold His Global Tariffs

President Donald Trump asked the US Supreme Court to uphold his global tariffs, seeking review in a case that could affect trillions of dollars in trade and give him broad new leverage over the world economy. The appeal calls for putting the case on a highly expedited schedule with arguments in early November, according to filings reviewed by Bloomberg. It follows a federal appeals court decision that said Trump can’t impose wide-scale import taxes by invoking a 1977 law designed to address national emergencies.

US/JAPAN (RTRS): Japan, US Near Deal to Bring Lower Auto Tariffs Into Effect, Source Says

apan and the United States are in the final stages of talks to implement lower tariffs on Japanese automobile imports within 10-14 days after the issuance of a U.S. presidential executive order, a Japanese government source told Reuters on Thursday. That means a reduced tariff rate on Japanese cars, from the current 27.5% to 15%, is set to take effect by the end of this month, said the source, who declined to be identified as the matter is private.

US/JAPAN (BBG): Japan’s Akazawa Visits US After Staff-Level Talks Progress

Japan’s top trade negotiator Ryosei Akazawa left for the US for ministerial talks, after lower level discussions on the July trade deal largely wrapped up — an indication that the two sides are making progress on implementing the agreement. “Administrative discussions have been finalized, and I am now traveling to the US as I think we should hold ministerial-level talks now,” Akazawa told reporters Thursday at Tokyo’s Haneda Airport as he left for Washington.

RUSSIA/UKRAINE (BBG): Zelenskiy’s Allies Fear Putin Is Readying New Assault in Ukraine

European leaders are increasingly concerned that Russia will mount a new offensive on Ukraine as they sit down with president Volodymyr Zelenskiy to discuss security guarantees for his country. At their security council meeting in Toulon last week, German and French officials discussed the Russian troops massing outside Pokrovsk, a Ukrainian-held stronghold in the eastern Donetsk region, according to people familiar with the matter who asked not to be named.

EUROPE/UKRAINE (MNI): 'Coalition of Willing' Meeting in Paris Underway

A hybrid in-person and virtual meeting of the so-called Coalition of the Willing group of Ukraine-backers is underway in Paris. Several European leaders and Ukrainian President Volodymyr Zelenskyy will call US President Donald Trump to discuss the outcome of the meeting at 08:00 ET 13:00 BST 14:00 CET. Details of the call likely to hit wires at around 09:00 ET 14:00 BST 15:00 CET. The Elysee said the primary focus of today's meeting is specific security guarantees that will be provided to Kyiv to ensure a peace agreement with Russia can hold.

GERMANY (MNI): IFO Lowers Y/Y Growth Forecasts; Future Q/Q Unchanged

IFO has lowered its growth forecast for Germany to 0.2% in 2025 (0.3% previously) and to 1.3% in 2026 (1.5% previously). The growth forecast for 2027 stands at 1.6%. However, the quarterly growth rates from Q3'25 to Q4'26 were all unchanged (to 1dp) from the last (summer) IFO projection. That means that the 2025 and 2026 Y/Y downward revisions are largely mechanical on the back of growth developing weaker during H1'25.

FRANCE (BBG): French Socialists to Meet Premier With Goal of Replacing Him

France’s Socialists will sit down with Prime Minister Francois Bayrou on Thursday as part of his last-ditch effort to save his job. The premier is facing a confidence vote on Monday and needs the support of rival parties in the country’s National Assembly to avoid a forced resignation. The Socialists, however, have made clear he won’t get it from them. And the party’s leaders have been open about their desire to take his seat.

CHINA (BBG): China Eyes Curbs on Stock Speculation to Foster Steady Gains

China’s financial regulators are considering a number of cooling measures for the stock market as they grow concerned about the speed of a $1.2 trillion rally since the start of August, people familiar with the matter said. The measures proposed to top policymakers in recent weeks include the removal of some short selling curbs, the people said, asking not to be identified as the information is private. Authorities are also contemplating options to rein in speculative trading on concern a sharp reversal might inflict heavy losses on retail investors.

CHINA (BBG): Rare Chinese Huddle on Policy Stokes Talk of Economy, Bond Boost

A rare meeting of Chinese fiscal and monetary policymakers has prompted speculation among analysts that easing measures are on the cards that will bolster the bond market and economic growth this year. A joint working group of officials led by Vice Finance Minister Liao Min and People’s Bank of China Deputy Governor Zou Lan met recently and pledged closer cooperation in support of the economy, according to a government statement late Wednesday.

CHINA (RTRS): China’s BYD Cuts Sales Target, Sources Say, as White-Hot Growth Cools

BYD has slashed its sales target for this year by as much as 16% to 4.6 million vehicles, two people with knowledge of the matter said, as the Chinese EV giant faces its slowest annual growth in five years and other signs that its era of record-setting expansion could be drawing to a close. China's largest automaker told analysts in March it was targeting sales of 5.5 million vehicles for 2025. But internally, the number has been downgraded multiple times in recent months, according to the people.

CHINA (MNI EXCLUSIVE): Fixing Price Guides Yuan Rally, Pressure Ahead in Q4

Chinese forex experts give their yuan outlook for the remainder of the year and beyond. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (MNI EXCLUSIVE): Risk of Weaker Inflation Expectations Concern BOJ

MNI outlines the BOJ's inflation expectations concerns. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

RBA (BBG): RBA Governor Warns Consumer Strength May Slow Rate Cuts

Australian consumers are starting to spend more as disposable incomes and wealth climb, a welcome boost for the economy that could slow the pace of monetary easing if it persists, according to Reserve Bank Governor Michele Bullock. “We are seeing the private sector start to demonstrate a little bit more growth now, which I think is positive,” Bullock said following a lecture in Perth late Wednesday. She referred to second-quarter gross domestic product data released this week which showed consumers largely led the better-than-expected outcome.

INDIA (BBG): Indian Banks Said to Ask RBI for Tweaks to Bond Issuance Plan

Indian lenders have requested the central bank to make various tweaks to the government’s bond-borrowing program that would make it easier to absorb supply amid market volatility, according to people familiar with the discussions. Banks in a meeting with the Reserve Bank of India discussed an extension to the government’s second-half borrowing plan until mid-March, instead of traditionally ending in February, the people said, asking not be named discussing private matters.

MALAYSIA (BBG): Malaysia Keeps Rate as Growth Risks Loom From Tariffs

Malaysia kept its benchmark interest rate unchanged as the central bank weighs the effects of a recent easing and growth risks posed by US tariffs. Bank Negara Malaysia left the overnight policy rate at 2.75% on Thursday, as predicted by 22 out of 24 economists in a Bloomberg survey. “At the current OPR level, the MPC considers the monetary policy stance to be appropriate and supportive of the economy amid price stability,” BNM said in a statement.

DATA

EUROZONE JUL RETAIL SALES -0.5% M/M, +2.2% Y/Y (VS +0.6% M/M, +3.5% Y/Y JUN) (MNI)

UK DATA (MNI): DMP Survey: Employment Growth Soft; Doves More Likely to Vote for Cuts

Employment growth has fallen back on both the realised and expected measures while the price growth measures have also ticked down a little (albeit remaining at high levels). There's no real evolution seen in the expected or realised wage growth numbers here. So overall, the main focus from the MPC will be the employment growth figures. There's not enough here for any of the MPC members who voted for Bank Rate on hold in August to alter their views, but for Bailey and Ramsden who have both stated they are focused on the labour market, this data release probably increases the probability that they vote for a cut in November.

SWITZERLAND DATA (MNI): August CPI Remains Unchanged; SNB September Cut Unlikely

- SWISS AUG CPI -0.1% M/M, +0.2% Y/Y

Swiss CPI inflation printed unchanged and in line with consensus at 0.2% Y/Y in August, with -0.1% M/M a tenth below consensus. Core CPI meanwhile decelerated to 0.7% Y/Y (vs 0.8% cons and prior). This means average Q3 to date inflation continues to stand marginally above the 0.1% forecast given by the SNB in its June meeting. Continued positive prints in Swiss inflation should skew near term policy expectations away from further easing into negative rates territory. The September meeting, priced at implied odds of around 10% of a cut, should remain out of play given today's data.

SWISS AUG UNEMPLOYMENT RATE 2.9% (MNI)

SWEDEN DATA (MNI): CPIF Ex-energy Reading Could Be Enough to Support a Sep Cut

- SWEDEN FLASH AUG CPIF +3.26% Y/Y

- SWEDEN FLASH AUG CPIF EX-ENERGY +2.92% Y/Y

CPIF ex-energy two tenths below the 3.1% Y/Y BBG consensus on a rounded basis. We wrote yesterday that a 2.9% Y/Y rounded CPIF ex-energy reading would probably be sufficient to give three Riksbank Executive Board members (Jansson, Breman, Bunge) confidence that the summer inflation uptick is likely to be temporary. This may pave the way for a (potentially not unanimously supported) 25bp cut in September.

AUSTRALIA DATA (MNI): Household Spending +5% Y/Y, Trade Surplus Up on Lower Imports

- AUSTRALIA JUL TRADE BALANCE A$+7310

Australia July household spending was close to market forecasts. We rose 0.5%m/m, in line with the consensus, although June was revised down a touch to 0.3%, (from 0.5% originally reported). Y/Y spending was still a touch firmer though at 5.1%, versus 5.0% forecast and 4.6% prior. Other data for July trade showed the trade surplus at over A$7bn due to weaker imports (off 1.3%m/m), while exports held up at +3.3%m/m. Softer imports reflected a modest decline in consumer related goods (so some caution around the better household spending story).

FOREX: Steady Trade Into Key US Datapoints

- Markets are generally quiet headed into the NY crossover, with an early phase of USD buying through the open broadly matching the price patterns we've seen so far this week. Volumes are lighter than average despite the minor move higher in the dollar, with EUR, JPY and GBP futures volumes ~30% below average for this time of day - although the roll into Z5 may be clouding this picture somewhat.

- Bucking the recent trend, GBP is seen firmer. Newsflow and fresh headlines are few and far between, with markets narrowing in on November 26th for the UK Budget announcement, which marks the next major macro event. For now, the bear threat in GBPUSD remains present following Tuesday’s sell-off. The pair has traded through a key support at 1.3391, the Aug 22 low. This signals scope for a deeper retracement and exposes 1.3315 next, a Fibonacci retracement. Clearance of this level would strengthen a bearish threat.

- Headlines suggesting that Japan and the US are in the final stages of talks to implement lower tariffs on Japanese automobile imports provided a moderate boost to the yen, allowing USDJPY to decline around 20 pips off the 148.41 session highs. Overall, the pair is operating within a relatively contained 60 pip range as investors await the plethora of US data this afternoon which includes ADP employment, weekly jobless claims and the ISM Services PMI. While all

important data points, a decisive breakout for USDJPY is unlikely ahead of tomorrow's employment report. - Larger FX options rolling off today include decent interest in and around 1.1629-80 (totalling close to E5bln) in EURUSD, while the interest in USDJPY is seen lower; $1.4bln is set to roll off at the Tuesday lows of Y147.00-15. The most sizeable AUD strike is north of yesterday's highs at 0.6595-00.

- ECB speakers today include Cipollone, who appears in EU Parliament and marks the likely last ECB speaker before the media blackout period into next week's rate decision - so is unlikely to deter markets from their current path at this stage. Fed's Williams is set to follow at the midpoint of the US session, speaking on the economic outlook and monetary policy.

EGBS: Passing of Supply Helps Major EGB Futures Extend Higher

The smooth passing of today’s Spanish and French supply appears to have helped major EGB futures extend session highs, with RXU5 now +45 ticks at 129.67. This sees Bunds test resistance at 129.69 (50-day EMA), which shields key short-term resistance at 129.90 (Aug 28 high).

- This morning’s headline flow has been relatively light, with continued weakness in Brent crude futures lending some support to the FI complex.

- The German curve leans bull flatter, alongside its more closely watched (at the current juncture) UK counterpart. Yields are 1.5 to 5bps lower across the curve, with 5s30s down 2.3bps at 104.7bps.

- Today’s LT OAT auction did not raise any major alarm bells regarding demand for French debt amid heightened domestic political/fiscal uncertainty. The 10-year OAT/Bund is 1bp narrower today at 79bps. Focus remains on the fallout from Monday’s no-confidence vote, with PM Bayrou likely to be ousted.

- Eurozone July retail sales were slightly weaker than expected, but this was offset by an upward revision to June (-0.5% M/M vs -0.3% cons, 0.6% prior revised from 0.3% initial).

- Irish final Q2 GDP data is due at 1100BST. If heavily revised, it could have ramifications for the Eurozone-wide GDP reading tomorrow.

GILTS: Bull Flattening Extends After I/L Auction

Strong demand at this morning’s I/L supply has allowed the bull flattening move in gilts to extend.

- A broader extension of yesterday’s rally in core global FI and another downtick in oil provided support in early London trade.

- Futures have traded to fresh session highs (90.62) following the auction.

- First resistance is located at the high from 28 & 29 August (90.84). Bulls need to force a break there to start turning the technical tide a little more in their favour.

- Bears still dominate at this stage, initial support at yesterday’s low (89.36).

- Yields are 1-5bp lower.

- 10-Year yields are ~20bp back from yesterday’s cycle high, while 30-Year yields are ~19bp off yesterday’s multi-decade top.

- 2s10s and 5s30s remain in their steepening trends despite the pullback from cycle highs.

- Modest dovish moves in GBP STIRs, with less than 10bp of easing still priced through year-end, SONIA futures little changed to +2.5.

- The latest BoE DMP survey pointed to a softening employment picture (which will probably embolden doves given their focus areas), meanwhile, it confirmed the impact of NIC & NLW hikes on inflation (which are knowns at this stage).

- Little of note on the UK calendar for the remainder of the day, which will leave cross-market cues and news flow front & centre.

- On the latter, fiscal worry still dominates in the UK.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.974 | +0.7 |

Nov-25 | 3.926 | -4.1 |

Dec-25 | 3.871 | -9.6 |

Feb-26 | 3.773 | -19.4 |

Mar-26 | 3.733 | -23.4 |

Apr-26 | 3.663 | -30.4 |

EQUITIES: Primary Trend Set-Up in Eurostoxx Futures is Bullish

The primary trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective. However, the contract has breached 5371.32, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5387.15, the 20-day EMA. A bull cycle in S&P E-Minis remains intact and the latest pullback is - for now - considered corrective. Price has traded through the 20-day EMA. The key support to watch lies at the 50-day EMA, at 6340.81. A clear break of this EMA is required to signal scope for a deeper retracement. This would open 6239.50, the Aug 1 low and a key support. Moving average studies still highlight a dominant uptrend. The bull trigger is 6523.00, the Aug 28 high.

- Japan's NIKKEI closed higher by 641.38 pts or +1.53% at 42580.27 and the TOPIX ended 31.28 pts higher or +1.03% at 3080.17.

- Elsewhere, in China the SHANGHAI closed lower by 47.681 pts or -1.25% at 3765.876 and the HANG SENG ended 284.92 pts lower or -1.12% at 25058.51.

- Across Europe, Germany's DAX trades higher by 79.48 pts or +0.34% at 23675.77, FTSE 100 higher by 1.62 pts or +0.02% at 9180.1, CAC 40 down 25.56 pts or -0.33% at 7694.15 and Euro Stoxx 50 down 1.99 pts or -0.04% at 5323.02.

- Dow Jones mini down 34 pts or -0.08% at 45274, S&P 500 mini up 9 pts or +0.14% at 6466.25, NASDAQ mini up 49 pts or +0.21% at 23497.75.

Time: 10:00 BST

COMMODITIES: Fresh All-Time Highs for Gold Reinforces Current Conditions

A bear cycle in WTI futures remains intact and the latest bull phase appears to have been a correction. Yesterday’s move down highlights a possible early reversal signal and the end of the corrective phase. Initial resistance to watch is $66.56, the Aug 4 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low. Gold remains in a clear bull cycle and the metal is trading closer to its recent highs. This week’s gains resulted in a breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high in the yellow metal. The break confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3600.00 handle. Initial firm support to watch lies at $3411.8, the 20-day EMA.

- WTI Crude down $0.65 or -1.02% at $63.31

- Natural Gas up $0.03 or +1.04% at $3.095

- Gold spot down $17.88 or -0.5% at $3540.43

- Copper down $6.1 or -1.32% at $456.95

- Silver down $0.27 or -0.66% at $40.9247

- Platinum down $19.36 or -1.36% at $1404.54

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/09/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/09/2025 | 1400/1000 | Fed nominee Stephen Miran | ||

| 04/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 04/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/09/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 04/09/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 04/09/2025 | 1605/1205 | New York Fed's John Williams | ||

| 04/09/2025 | 2300/1900 | Chicago Fed's Austan Goolsbee | ||

| 05/09/2025 | 2330/0830 | ** | average wages (p) | |

| 05/09/2025 | 2330/0830 | ** | Household spending | |

| 05/09/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/09/2025 | 0600/0700 | *** | Retail Sales | |

| 05/09/2025 | 0645/0845 | * | Foreign Trade | |

| 05/09/2025 | 0800/1000 | * | Retail Sales | |

| 05/09/2025 | 0900/1100 | * | Employment | |

| 05/09/2025 | 0900/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey | |

| 05/09/2025 | 1400/1000 | * | Ivey PMI | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |