MNI US OPEN - Trump Says Xi Hard to Make Deal With

EXECUTIVE SUMMARY

- TRUMP SAYS XI HARD TO MAKE DEAL WITH

- MNI BOC PREVIEW - NOT ENOUGH CLARITY TO CUT

- MERZ PLANS €46BN CORPORATE TAX BREAKS TO REVIVE GERMAN ECONOMY

- JAPAN’S NEGOTIATOR AKAZAWA TO VISIT US JUNE 5-8 FOR TRADE TALKS

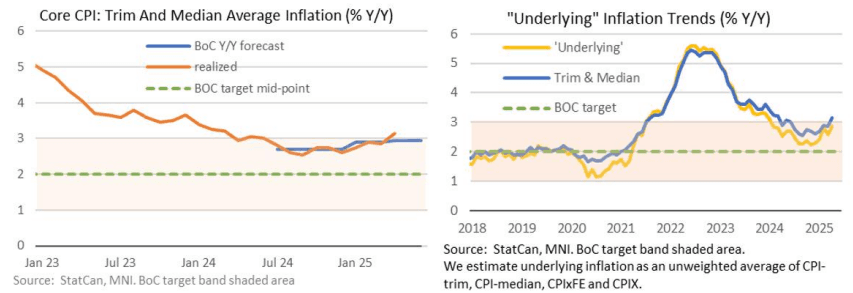

Figure 1: Recent Canada inflation trends

NEWS

MNI BOC PREVIEW - JUNE 2025: Not Enough Clarity to Cut

The Bank of Canada is likely to maintain the overnight rate target steady at 2.75% for a second consecutive meeting on Wednesday, though analyst opinion and pricing eye a possible 25bp cut. April’s pause came after 225bp of cuts to arrive in the middle of the BoC’s currently estimated neutral range of 2.25-3.25% (unchanged in the April Monetary Policy report). With this having put the BOC in a position to see further developments in the US-Canada trade dispute before pulling the trigger on further moves, incoming economic data have tilted toward a further hold.

MNI ECB PREVIEW - JUNE 2025: The Last Consecutive Cut?

The ECB is fully expected to cut its three key rates by 25bp this week, taking its deposit rate to 2.00%. That would be the mid-point of the neutral estimated range of 1.75-2.25% according to ECB staff, although senior ECB leadership including Lagarde last meeting have been keen to downplay neutral discussions when faced with significant shocks. Nearing the perceived end of the easing cycle, focus will be on any clues around the willingness or lack thereof to highlight a potential pause in July. A July cut is only about 25% priced, perhaps vulnerable to dovish surprises.

US/CHINA (MNI): Trump Says Xi Hard to Make Deal With

U.S. President trump posts the following on Truth Social: "I like President XI of China, always have, and always will, but he is VERY TOUGH, AND EXTREMELY HARD TO MAKE A DEAL WITH!!!"

US/EU(MNI): Sefcovic Had "Productive Discussion" w/USTR, "Advancing in Right Direction"

EU Trade Commissioner Maros Sefcovic posts on X: "Had a productive and constructive discussion with [USTR Jamieson Greer] on the margins of the OECD Trade Ministerial. We're advancing in the right direction at pace - and staying in close contact to maintain the momentum." Following US President Donald Trump's announcement of a 50% tariff on the EU (delayed until 9 July), Sefcovic has pledged that calls would take place between EU and US teams at least every other day in order to try and reach an agreement. However, Trump's signing of a directive raising steel and aluminium tariffs to 50% as well as the 'reciprocal' tariffs could further muddy the waters.

US/EUROPE (FT): Europe Confronts Trump’s Triple Threat on Ukraine, NATO and Trade

European governments are braced for high-stakes negotiations with US President Donald Trump that will put the continent’s defence, economy and security on the line. Grand designs to build “an independent Europe” are on hold as officials strain to maintain Trump’s support through five weeks of crunch talks over Ukraine, transatlantic trade and the US security commitment to Nato. Europe’s negotiators are increasingly concerned that the US president will demand concessions in one area in exchange for support in another, forcing the EU to sacrifice its core values or accept a firm break with Washington.

US/JAPAN (BBG): Japan’s Negotiator Akazawa to Visit US June 5-8 for Trade Talks

Japan’s lead trade negotiator Ryosei Akazawa says he’s visiting the US between June 5 to 8 for talks with his counterparts in Washington. Not currently considering accompanying Prime Minister Shigeru Ishiba to the G-7 summit in Canada, Akazawa tells reporters.

US/IRAN (NYT): U.S. Proposes Interim Step in Iran Nuclear Talks Allowing Some Enrichment

The Trump administration is proposing an arrangement that would allow Iran to continue enriching uranium at low levels while the United States and other countries work out a more detailed plan intended to block Iran’s path to a nuclear weapon but give it access to fuel for new nuclear power plants. The proposal amounts to a bridge between the current situation, in which Iran is rapidly producing near-bomb-grade uranium, and the U.S. goal of Iran enriching no uranium at all on its soil.

US (BBG): Trump Obscures Medicaid Cuts in Bid to Pass Massive Tax Bill

Donald Trump publicly resisted Medicaid cuts — until his budget director, Russell Vought, convinced the president that reductions to heath coverage for low-income people, embedded in the Republican tax bill, were just weeding out fraud and abuse. Trump has readily adopted that rhetoric, repeatedly declaring that his signature bill contains “no cuts” to the social safety program, even as the non-partisan Congressional Budget Office estimates at least 7.6 million people would become uninsured if the bill takes effect.

US (WSJ): Trump Seeks Congress’s Approval for Package of DOGE Cuts

The White House is sending Congress a $9.4 billion rescissions package Tuesday that would codify some spending cuts made by the Trump administration, effectively asking lawmakers to reverse spending they previously voted into law. The White House also is weighing the use of a separate, controversial process called impoundment to claw back funds, sidestepping the legislative branch and setting up a likely legal battle. The rescissions package, which includes $8.3 billion in cuts to foreign aid and $1.1 billion to public media, can pass the House and Senate with a simple majority.

US (WSJ): Elon Musk Calls Trump Megabill a ‘Disgusting Abomination’

Former White House cost-cutting czar Elon Musk called President Trump’s “big, beautiful” tax and spending package a “disgusting abomination,” stepping up his criticism just as the Senate is trying to quickly pass the measure and get it signed into law by July 4. Musk’s comments are his latest sharp words about the package, which includes tax cuts as well as reductions to spending on Medicaid and food assistance. Last month, he gave new fuel to GOP critics of the Republicans’ multitrillion-dollar agenda, saying that the current measure failed to reduce the federal deficit.

US (NYT): Higher Tariffs on Steel and Aluminum Imports Go Into Effect

U.S. tariffs on steel and aluminum imports doubled on Wednesday, as President Trump continued to ratchet up levies on foreign metals that he claims will help revitalize American steel mills and aluminum smelters. The White House called the increased tariffs, which rose to 50 percent from 25 percent just after midnight Eastern time, a matter of addressing “trade practices that undermine national security.”

GERMANY (FT): Friedrich Merz Plans €46bn Corporate Tax Breaks to Revive German Economy

Germany’s new government will seek to pass a €46bn package of corporate tax breaks over the summer in an effort to jolt the Eurozone’s largest economy out of stagnation. Finance minister Lars Klingbeil, a Social Democrat, will outline the measures during a cabinet meeting on Wednesday. The tax incentives, which include deductions for new equipment and new electric vehicles, will cost about €46bn in total by 2029, when the coalition’s term expires, according to government estimates seen by the Financial Times.

EUROPE/CHINA (MNI): European Lobby Supports China Medical Device Limits

MNI (Beijing) The European Chamber of Commerce in China supports the end goal of the EU’s recent measure to restrict Chinese medical device manufacturers from public procurement tenders, aimed at ensuring reciprocal market access, a statement from the chamber on Wednesday said. While urging caution in the application of trade defence tools, the chamber noted in a recent survey 100% of respondents in the medical devices sector reported missing business opportunities in 2024 due to market access and regulatory barriers.

EUROPE (BBG): Europe’s T+1 Shift Projected to Be Costlier Than US Transition

Europe’s transition to a faster settlement regime will likely be more expensive than in the US, as the region’s complex market infrastructure requires larger teams to steer the process. The shift to what’s known as T+1 is estimated to cost $36 million for large European custodians, according to a report by Firebrand Research. That compares to a $13 million average cost similar firms incurred around the North American transition, it said.

UK (The Times): Rachel Reeves Pledges £15bn Investment to Boost North

Rachel Reeves will warn that Britain has become reliant on “too few places” for economic growth as she promises £15 billion for transport links in the north and Midlands to spur growth and combat the threat of Reform. The chancellor will set out a dozen local transport projects designed to encourage growth in red wall areas where Nigel Farage is breathing down Labour’s neck, promising to give “every region a fair hearing” on bids for public cash. She will confirm a rewrite of Treasury investment rules designed to divert money away from the southeast towards areas that ministers say have been “locked out” of public cash and left behind economically.

UK (BBC): UK Temporarily Spared From Trump’s 50% Steel Tariffs

The UK has been temporarily spared from US President Donald Trump's executive order doubling steel and aluminium tariffs from 25% to 50%. The order raises import taxes for US-based firms buying the metals from other countries from Wednesday - but the levy remains at 25% for the UK. However, the UK could end up facing the higher rate if its deal signed with the Trump administration last month, which would see steel and aluminium tariffs axed, does not come into force.

ECB (BBG): Lagarde’s ECB Future Set for Scrutiny After WEF Job Speculation

Christine Lagarde is about to face scrutiny on her commitment to keep leading the European Central Bank, not least as she nears the milestone of having just about tamed inflation. The president, who will hold a press conference on Thursday to present the Governing Council’s latest policy decision, has been courted for the top job at the World Economic Forum in Switzerland, even though her term in Frankfurt officially lasts for another 2 1/2 years. It’s not unprecedented for those in her position to get quizzed on such matters by reporters, as happened with her predecessor Mario Draghi when speculation arose that he might become Italian head of state. Even so, such queries would highlight just how much Lagarde finds herself at a crossroads at present.

S.KOREA (MNI): Lee Announces Nominations for Key Gov’t Positions After Swearing-in

Following his swearing into office earlier today, President Lee Jae-myung has announced the nomination of Kim Min-seok as the new administration's first prime minister. Kim (61) has served two separate terms in the National Assembly (1996-2002 and since 2020), as well as a period as president of the DPK. He has served as an adviser to Lee and is seen as a close political ally. Lee described Kim as "the right person to overcome the crisis and restore the people's economy as he has both a concrete sense and the political power to unite". The former Minister of Unification Lee Jong-seok was nominated as the director of the National Intelligence Service. Lee is seen as a notable figure in the 'neutralist realignment' movement, which advocates for a more independent foreign policy for South Korea not so closely tied into that of the United States.

JAPAN (MNI): LDP Coalition Partner to Propose Lower Consumption Tax on Food

Headlines have crossed from Reuters, citing local news wires (Yomirui), that Japan's ruling coalition partner, Komeito will propose lowering the consumption tax on food from 8% to 5%. This would be a campaign pledge ahead of expected upper house elections in July of this year. Reuters notes: "The campaign pledge, to be announced on Friday, will also include a proposal to offer cash payouts to cushion the blow to households from rising living costs, the paper said." The proposal would reported be funded via revenue increases and not increased debt issuance, per RTRS.

JAPAN (BBG): Japan’s Fertility Rate Hits Record Low Despite Government Push

Japan’s fertility rate declined in 2024 for the ninth consecutive year, reaching another historical low that underscores the immense challenge facing the government as it attempts to reverse the trend in one of the world’s most aged societies. The total fertility rate — the average number of children a woman is likely to have over her childbearing years — fell to 1.15, down from 1.2 the previous year, and marking the lowest rate in records going back to 1947, according to a Health Ministry release on Wednesday. The trend was particularly notable in Tokyo, where the rate was below 1 for the second year in a row.

MEXICO (BBG): Mexico Will Ask US Government for Steel Tariff Exemption

Mexico will ask Donald Trump’s administration this week to be exempted from an increase in steel tariffs to 50%, the country’s economy minister said on Tuesday. “It’s not fair and it’s unsustainable. We will present our arguments on Friday to exclude Mexico from this measure,” Marcelo Ebrard said during an event in Mexico City. Ebrard, who will travel to Washington on Friday for talks with US officials, said Mexico has a “Plan B” in the event that the heightened levy remains in place.

MNI NBP PREVIEW - JUNE 2025: Pause Amid Brighter Outlook

The consensus is for the National Bank of Poland (NBP) to take a breather after a 50bp cut delivered in May and leave the reference rate unchanged at 5.25%. Although the inflation outlook has become even more benign, robust outturns for wage growth and retail sales may encourage the Monetary Policy Council (MPC) to act on the Governor’s forward guidance and stay put at least until the publication of the next macroeconomic projection in July.

DATA

EUROZONE DATA (MNI): May Services PMI Revised Higher; Composite Remains Just Above 50

- EUROZONE MAY SERVICES PMI 49.7 (48.9 FLASH, 50.1 APRIL)

- GERMANY MAY SERVICES PMI 47.1 (47.2 FLASH, 49.0 APRIL)

- FRANCE MAY FINAL SERVICES PMI 48.9 (47.4 FLASH, 47.3 APRIL)

The Eurozone May services PMI was revised up to 49.7 (vs 48.9 flash, 50.1 prior), following an upward revision in France and a stronger-than-expected Italian print. We estimate the Germany/France combined services PMI at 47.9 (vs 48.3 prior), and the ex-Germany/France measure at 52.8 (vs 51.6 flash, 53.2 prior). That helps the composite PMI remain just about in expansionary territory for the fifth consecutive month (it has had a range of 50.2-50.9 through this year), consistent with positive, but sluggish growth. A reminder that the ECB is expected to revise its GDP projections lower at tomorrow's decision, but this will likely be centred in 2026.

SPAIN DATA (MNI): Tariff-related Uncertainty Weighs on Activity

- SPAIN MAY SERVICES PMI 51.3 (52.9 FCAST, 53.4 APRIL)

The Spanish services PMI was weaker-than-expected at 51.3 (vs 52.9 cons, 53.4 prior), the lowest in 18 months and in contrast to the stronger-than-expected manufacturing reading on Monday. Curiously, there appears to be a larger negative impact from tariffs in the services PMI (see below) compared to the manufacturing counterpart, which noted "several panellists noted a relative improvement in European and US demand, albeit still characterised by some hesitation in committing to new work amid the uncertain tariff outlook". The composite reading was 51.4 (vs 52.3 cons, 53.5 prior), the lowest since December 2023.

SPAIN DATA (MNI): Industrial Production Trend Remains Tepid at Best

Spanish industrial production surprisingly fell -0.8% M/M in April (cons 0.0, INE index calculates at -0.85%) in seasonally and working day adjusted terms. It follows a 0.9% M/M increase in March although monthly changes are volatile. Production of consumer goods increased 1.0% M/M but capital (-0.5%) and intermediate (-0.7%) softened whilst energy (-5.5%) slumped. Looking through the monthly noise, IP only increased 0.6% Y/Y swda (-5.7% Y/Y in nsa terms, in part because of the later Easter this year) as the production trend remains bleak.

ITALY DATA (MNI): Services PMI Strongest Since June 2024, Employment Rising

- ITALY MAY SERVICES PMI 53.2 (52.0 FCAST, 52.9 APRIL)

The Italian services PMI was stronger-than-expected at 53.2 (vs 52.0 cons, 52.9 prior), the highest level since June 2024. That brings the composite PMI to 52.5 (vs 51.4 cons, 52.1 prior), the highest since April 2024. Services employment continued to tick up on May, consistent with the record-low Italian unemployment level reported yesterday. Key notes from the release: "Overall new work volumes continued to rise at a modest pace in May. The latest increase was the fourth in successive months and was a result of incoming new orders from both existing and new customers, panel member reports showed".

UK DATA (MNI): Services PMI Revised Upward; Growth/Labour Market/Inflation Slowing

- UK MAY SERVICES PMI 50.9 (50.2 FLASH, 49.0 APRIL)

There was an upward revision to the UK services PMI with the May print being revised to 50.9 from the flash print of 50.2. The composite PMI was also revised up, back above 50 to 50.3 from the flash of 49.4. Note that in yesterday's testimony in front of the Treasury Select Committee several MPC members noted that underlying indicators suggested that UK GDP growth was close to zero (in contrast to some of the one offs that have skewed the hard data upwards recently). There isn't much in this data release today that would suggest otherwise. The press release notes that the overall services numbers were "helped by

improving confidence among clients and fewer reports of tariff concerns."

GERMANY DATA (MNI): VDMA Machine Orders Expectedly Deteriorate in April

VDMA German machine orders fell 6% Y/Y in April, driven by a low print from non-euro countries (-13% Y/Y). The release represents a significant fall from March's +4% Y/Y, which brought Q1 to be the first positive quarter in machinery orders since Q1 2022. "This was an expected setback", VDMA comments as April saw material uncertainty following a firmer trade stance from the US administration. Domestic orders came in at -4% Y/Y (-3% March).

SWEDEN DATA (MNI): May PMIs Post Solid Performance, But Riksbank Interests Elsewhere

The solid performance of the Swedish May PMIs contrasts somewhat with the May Economic Tendency Indicator, which eased to 94.6 from 95.0 in April. However, the composite PMI has generally been more optimistic than then ETI since the pandemic. For the Riksbank, more focus will be on tomorrow's flash CPIF report and the central bank's own Business Survey on June 10. The Swedish services PMI moved back into expansionary territory in May, rising to 50.8 from 48.7 prior, above the 4-analyst strong 48.9 consensus. The composite PMI was thus 50.3, unchanged on the month.

AUSTRALIA DATA (MNI): Aussie Q1 GDP +0.2%, Productivity Measures Weaker

- AUSTRALIA Q1 GDP +0.2% Q/Q

- AUSTRALIA Q1 GDP +1.3% Y/Y

Australia’s GDP rose 0.2% in the March quarter, 20 basis points lower than expected, and 1.3% y/y, according to Australian Bureau of Statistics data released Wednesday. “Public spending recorded the largest detraction from growth since the September quarter 2017,” said Katherine Keenan, head of national accounts at the ABS. GDP per capita fell 0.2%, following a 0.1% rise in Q4. GDP per hour worked, a key productivity measure, fell 1% y/y, while real unit labour costs grew 2.6%. The RBA expects productivity growth to reach 0.9% by the December quarter.

FOREX: USD Index Holds JOLTS Rally, Hopes for US-China Breakthrough Dwindle

- The USD Index remains either side of the 99.00 handle, but is holding the majority of the rally off lows yesterday. Despite this recovery, the dollar remains well inside the downtrend drawn off the mid-May highs, with the firm downward bias in the 50-dma cementing the recent momentum lower.

- EUR trades off the overnight lows, either side of 1.1400 headed into the NY crossover having failed to make progress above 1.1455 yesterday. A stabilisation in the long-end of the EGB curve is helping contain the currency, although trade tensions and the risk of headlines remain at the forefront. EU's Sefcovic this morning stated that talks with the US are going in the right direction "at pace" - however markets are growing increasingly used to the slow progress made in negotiations with the White House.

- Similarly, Trump posted overnight that the Chinese President Xi is "extremely hard to make a deal with" - hampering sentiment somewhat, but the lack of follow through for currency markets is the latest signal that expectations for a near-term breakthrough are limited.

- The Bank of Canada rate decision takes focus going forward, with markets expecting no change on rates from the Bank although a not insignificant minority see risks of a further dovish tilt at the Bank. Markets see the BOC in a position to wait for further developments in the US-Canada trade dispute before pulling the trigger on further moves, incoming economic data have tilted toward a further hold. In particular, better-than-expected GDP and a pickup in core inflation should tilt the balance toward a hold.

- US ADP Employment Change is a calendar highlight, with the ISM services index for May set to follow. Markets continue to watch for any signals ahead of Friday's nonfarm payrolls print from the data, particularly in the context of yesterday's stronger-than-expected job openings numbers. Fed's Bostic & Cook are set to moderate a session at the Fed Listens event series.

EGBS: Bunds Weaken But Support Still Some Way Off, Focus Remains on ECB

Bund futures have weakened steadily through the European morning, currently -31 ticks at 130.99. German cabinet approval of a E46bln corporate tax cut alongside spillover from USTs appears to have contributed to the weakness intraday. First support remains at 130.39, the May 29 low, but a bullish technical theme remains intact.

- June is still the front contract in Bunds for now, but expect September to take its place by the end of the day as Eurex rolls progress ahead of this week’s risk events (ECB decision Thursday, US NFP Friday).

- German yields are around 1bp higher across the curve.

- The Eurozone May services PMI was revised up to 49.7 (vs 48.9 flash), which added incremental pressure to EGBs. That helped the composite PMI remain just about in expansionary territory for the fifth consecutive month (it has had a range of 50.2-50.9 through this year), consistent with positive, but sluggish growth.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels. The BTP/Bund spread is back at 96.5bps at typing.

- Regional focus remains on tomorrow’s ECB decision.

GILTS: Holding Lower

Gilts hold lower, with weakness in core global FI (given renewed focus/reports surrounding German fiscal easing and a rally in European equity benchmarks) spilling over.

- Futures -44 at 91.48, filling yesterday’s opening gap higher.

- The recent gains in the contract have allowed short-term oversold conditions to unwind, with the uptick considered corrective from a technical perspective.

- Initial support and resistance located at 91.16/92.11.

- Yields 1-3bp higher, 10s lead the sell off.

- 10s stick in the wide 4.40-4.80% range that has been in play since mid-January.

- The benchmark remains within the wedge drawn off the longer-term uptrend (beginning at the December ’21 lows) and the short run downtrend drawn off the ’25 high. It last trades at 4.67%, with the boundaries of the wedge located at 4.500% & 4.787% today.

- Fiscal fragility remains a topic of discussion in the UK. This morning has seen Chancellor Reeves once again stress that she has no intention of raising taxes at the same scale as was seen in the ’24 Budget.

- No real reaction was seen following the mark higher in the final services PMI print, gilts were already under pressure.

- Mar-28 supply from the DMO passed smoothly, although the cover was a touch below average.

- There is little of note on the UK calendar for the remainder of the day, with wider focus set to fall on the U.S. ISM services survey and macro inputs (tariff matters and European fiscal issues remain front and centre there).

EQUITIES: Eurostoxx 50 Moving Average Studies Remain in Bull-Mode Position

The trend cycle in Eurostoxx 50 futures remains bullish and a recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5262.93, the 50-day EMA. A clear break of this average is required to signal a possible reversal. The trend condition in S&P E-Minis is unchanged and remains bullish and the contract is trading just ahead of its recent high. A print above 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. An extension would open 6057.00 next, the Mar 3 high. Key support lies at 5765.62, the 50-day EMA.

- Japan's NIKKEI closed higher by 300.64 pts or +0.8% at 37747.45 and the TOPIX ended 14.02 pts higher or +0.51% at 2785.13.

- Elsewhere, in China the SHANGHAI closed higher by 14.227 pts or +0.42% at 3376.203 and the HANG SENG ended 141.54 pts higher or +0.6% at 23654.03.

- Across Europe, Germany's DAX trades higher by 207.88 pts or +0.86% at 24299.5, FTSE 100 higher by 6.83 pts or +0.08% at 8793.83, CAC 40 up 52.2 pts or +0.67% at 7816.04 and Euro Stoxx 50 up 35.5 pts or +0.66% at 5411.2.

- Dow Jones mini up 71 pts or +0.17% at 42669, S&P 500 mini up 11.25 pts or +0.19% at 5992.25, NASDAQ mini up 27 pts or +0.12% at 21732.

Time: 09:50 BST

COMMODITIES: WTI Futures Close to Recent Highs But Bear Threat Remains Present

WTI futures continue to trade closer to their recent highs. A bear threat remains present and the recovery since Apr 9 still appears corrective. A key resistance area to monitor is $62.51, the 50-day EMA. It has again been pierced. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. A bullish theme in Gold remains intact and this week’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Sights are on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, key support and the bear trigger to watch has been defined at $3121.0, the May 15 low.

- WTI Crude up $0.03 or +0.05% at $63.43

- Natural Gas down $0.05 or -1.32% at $3.673

- Gold spot up $8.49 or +0.25% at $3361.69

- Copper up $5.55 or +1.15% at $488.95

- Silver up $0.01 or +0.04% at $34.5228

- Platinum up $13 or +1.2% at $1092.56

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 04/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/06/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/06/2025 | 1430/1030 | BOC press conference | ||

| 04/06/2025 | 1800/1400 | Fed Beige Book | ||

| 05/06/2025 | - | European Central Bank Meeting | ||

| 05/06/2025 | 2330/0830 | ** | average wages (p) | |

| 05/06/2025 | 0130/1130 | ** | Trade Balance | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/06/2025 | 0545/0745 | ** | Unemployment | |

| 05/06/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/06/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 05/06/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/06/2025 | 0745/0845 | BOE's Greene Opening Remarks at Econdat Conference 2025 | ||

| 05/06/2025 | 0800/1000 | * | Retail Sales | |

| 05/06/2025 | 0830/0930 | Decision Maker Panel data | ||

| 05/06/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/06/2025 | 0900/1100 | ** | PPI | |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech |