MNI US OPEN - Prospect of December BOJ Hike Gaining Traction

EXECUTIVE SUMMARY

- NVIDIA’S HUANG UNSURE WHETHER CHINA WOULD ACCEPT H200 CHIPS

- BESSENT UNDER DISCUSSION TO ALSO LEAD NATIONAL ECONOMIC COUNCIL: BBG

- KEY JAPAN OFFICIALS WOULD GO ALONG WITH A BOJ DECEMBER RATE HIKE: BBG

- PUTIN MEETS MODI IN INDIA TO UNDERSCORE DEFENSE AND ENERGY TIES

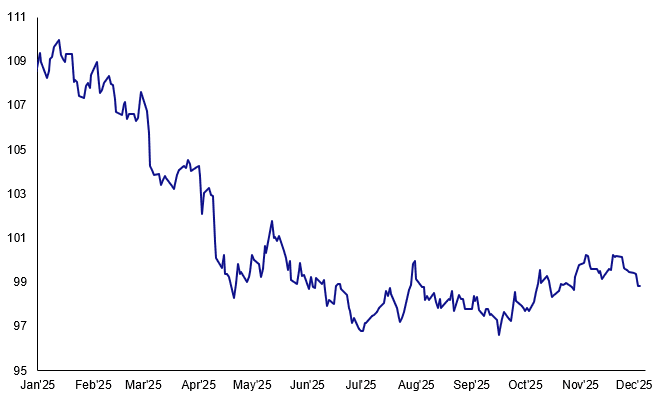

Figure 1: DXY falls to new pullback lows as greenback weakness persists

Source: MNI, Bloomberg Finance L.P.

NEWS

US/CHINA (BBG): Nvidia’s Huang Unsure Whether China Would Accept H200 Chips

Nvidia Corp. Chief Executive Officer Jensen Huang said he’s unsure whether China would accept the company’s H200 artificial intelligence chips should the US relax restrictions on sales of the processors, following a meeting Wednesday with President Donald Trump. Addressing reporters at the US Capitol, Huang said he and Trump talked about export controls but declined to offer specifics. The Nvidia chief’s meeting with the president comes after Trump administration officials discussed whether to allow the H200 to be sold in China. Asked whether authorities in Beijing would allow Chinese companies to buy the H200, Huang expressed uncertainty.

US (BBG): Bessent Under Discussion to Also Lead National Economic Council

Donald Trump’s aides and allies are discussing the possibility of making Treasury Secretary Scott Bessent the top White House economic adviser — in addition to his current job — should the president pick Kevin Hassett as the next chair of the Federal Reserve, according to people familiar with the matter. Tapping Bessent to lead the White House’s National Economic Council would allow him to consolidate oversight of Trump’s economic policies if Hassett — the current NEC director — becomes the next leader of the US central bank, an announcement Trump has hinted at in recent days. The people spoke on the condition of anonymity to discuss potential moves that have not been finalized.

RUSSIA/INDIA (MNI): Putin Meets Modi in India to Underscore Defense and Energy Ties

Russian President Vladimir Putin begins a 2-day visit to India where he will meet with Prime Minister Narendra Modi to underscore defense and energy ties between the two countries. Bloomberg reported this morning that India will pay about $2bn to lease a nuclear-powered submarine from Russia. Meanwhile, the Russia-India Business Forum starts in New Delhi.

ECB (BBG): ECB’s Cipollone Says Inflation Risks Balanced, Nikkei Reports

European Central Bank Executive Board member Piero Cipollone indicated he’s comfortable with current policy settings. “Risks around inflation seem balanced and our central scenario seems more and more credible,” he told Nikkei in an interview published Thursday. “So for the time being — as the president has said several times — we are in a good place. And we stand ready to react to any shock.”

FRANCE/CHINA (BBG): Macron Urges Xi to Boost Chinese Investment to Shrink Trade Gap

French President Emmanuel Macron pushed for more Chinese investment during a meeting with Chinese leader Xi Jinping, as Paris looks to rebalance its economic ties with Beijing and narrow a persistent trade gap. Macron said Europe, including France, needs a clearer framework to attract more Chinese direct investment. He warned that China’s growing trade surplus with the rest of the world is becoming unsustainable, while investment flowing into Europe remains too low.

BOJ (BBG): Key Japan Officials Would Go Along With a BOJ December Rate Hike

Key members of Prime Minister Sanae Takaichi’s government wouldn’t try to stop the Bank of Japan if it decides to raise interest rates in December, according to people familiar with the matter, a stance that makes a move more likely. Still, there are some senior officials who oppose that timing, the people added. The comments come amid heightened speculation that the BOJ will increase the benchmark rate to 0.75% at the end of its next policy meeting on Dec. 19, following remarks from Governor Kazuo Ueda on Monday.

BOJ (MNI EXCLUSIVE): BOJ Frets Over Neutral Rate Update

MNI discusses how the BOJ plans to communicate its neutral-rate estimate following a potential hike. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (MNI): BOJ's Ueda Sees Econ Package Boosting Underlying CPI

Bank of Japan Governor Kazuo Ueda said on Thursday that the government’s economic stimulus package will have a positive impact on economic growth and boost underlying inflation. Ueda told lawmakers that the stimulus package, mainly countermeasures to cope with high prices, will lower headline CPI, but it will exert upward pressure on underlying inflation through economic growth. However, he could not comment on the degree of the impact.

JAPAN (BBG): Japan’s Strongest 30-Year Bond Sale Since 2019 Eases BOJ Jitters

The strongest demand at Japan’s 30-year bond sale since 2019 suggested that investors are finally stepping back in due to higher yields, bringing some respite to a market that’s bracing for a rate hike. The 30-year yield dropped three basis points to 3.39% after the bid-to-cover ratio at the Ministry of Finance’s offering jumped to 4.04, higher than that at the previous auction and comfortably above the average for the past year.

CHINA (RTRS): China State-Owned Banks Soak Up Dollars to Slow Yuan Gains, Sources Say

China's major state-owned banks bought dollars in the onshore spot market this week and held on to them in an unusually strong effort to rein in yuan strength, according to people with knowledge of the matter. But unlike their usual trading strategy, the lenders did not appear to recycle the dollars into the swap market, market sources said, noting the move was likely aimed at tightening dollar liquidity and so raising the cost of long yuan bets.

CHINA (MNI): PBOC to Control Pace to Prevent Side Effects: Pan

MNI (Beijing) The People's Bank of China will calibrate the intensity and pace of its policy to avoid excessive moves from reducing policy effectiveness and causing long-term side effects, while taking measures to smooth out economic fluctuations, Governor Pan Gongsheng said in an article in People's Daily on Thursday. Due to economic restructuring and credit structure changes, the credit demand of the real economy is evolving, therefore, enhancing the utilisation efficiency of existing funds and optimising fund allocation are equally important as increasing new loans, he noted, pointing out the need of balancing support for economic growth and the health of financial institutions.

CHINA (MNI): PBOC Flags Risk Prevention as a Major Mandate: Pan

MNI (Beijing) The People's Bank of China will take measures to curb the buildup of financial risks, address idle funds circulating in the financial sector, and strengthen the coordination between monetary policy and fiscal, industrial policies, said Governor Pan Gongsheng in an article on People’s Daily on Thursday. The central bank has dual objectives of maintaining both currency stability and financial system stability, meaning the monetary policy framework aims to support stable currency value, economic growth, full employment and balance of international payments, he said.

DATA

EUROZONE DATA (MNI): Retail Sales Continue to Stagnate on June Levels

- EUROZONE OCT RETAIL SALES +0.0% M/M, +1.5% Y/Y (VS +0.1% M/M, +1.2% Y/Y SEP)

Eurozone real retail sales came in in line with expectations in October on the sequential reading, at 0.0% M/M (0.0% cons) following an upwardly revised September (0.1%, revised from -0.1%). On a bigger picture, Eurozone retail sales continue to stagnate since June. Across sectors, October saw food, drinks, tobacco at 0.3% M/M (-0.2% Sep), Non-food products (excl. car fuel) at -0.2% (0.0% Sep) and car fuels at 0.3% (0.0% Sep). None of these categories saw a major directional trend over the last couple of months.

UK DATA (MNI): DMP: Employment Falls More Significantly

The big story from the DMP data is how soft the employment data looks, both on the realised and expected measures. This will give confidence to the doves on the MPC that the labour market is indeed weakening. The wage growth data was not too surprising (and as we noted in our preview the 3-month average expected number increased a tenth - but the single month print was softer). Employment growth was soft: both realised and expected. Realised employment growth was -1.8%Y/Y on the single month measure in November. This is the first print below -0.6% since July 2021. Expected employment growth was -0.7%Y/Y on the single month print, bringing the 3-month average down a tenth to -0.2%Y/Y (after last month rounding to a negative number for the first time since December 2020).

UK DATA (MNI): Construction PMI Falls, Details Terrible; Budget Uncertainty the Driver

- UK NOV CONSTRUCTION PMI 39.4 (44.6 FCAST, 44.1 OCT)

UK construction PMI data was pretty awful, falling 5 points below consensus to 39.4, but new orders falling off ahead of the Budget can explain much of the move. It might therefore see a bit of a rebound next month but the details are not great. From the press release: "Many construction companies commented on weak client confidence, alongside delayed spending decisions linked to uncertainty ahead of the Budget."

SWEDEN DATA (MNI): CPIF Ex-energy Inflation Soft, but No Details Available

- SWEDEN FLASH NOV CPIF +2.27% Y/Y (vs 3.07% prior, 2.09% Riksbank, 2.5% cons)

- SWEDEN FLASH NOV CPIF EX-ENERGY +2.36% Y/Y (vs 2.76% prior, 2.45% Riksbank, 2.6% cons)

November flash CPIF ex-energy inflation was two tenths below consensus on a rounded basis and one-tenth below the Riksbank's September MPR forecasts. That's notable given underlying inflation was tracking two tenths above the September projections in October. The "low" unrounded reading adds to the downward surprise. That said, there's little net impact in SEK FX - the inflation reading doesn't change the near-term Riksbank outlook. The policy rate is likely to be kept on hold at 1.75% for "some time".

SWITZERLAND DATA (MNI): Little Net Change in Labour Market Data Ahead of SNB

- SWISS NOV UNEMPLOYMENT RATE 3.0%

- SWISS NOV UNEMPLOYMENT CHANGE +2.7% M/M, +14.7% Y/Y

The Swiss labour market has seen little net move in November after seeing less impact by a softer external sector (than GDP) in Q3. This should support the case for a hold at the upcoming (Dec 11) SNB meeting. The seasonally adjusted unemployment rate, as expected, remained at 3.0% in November. It remains on a gradual uptrend since 2023. Vacancies meanwhile increased slightly since October, now standing at 36,880 (35,994 September, 36,841 November 2024) in seasonally adjusted terms.

AUSTRALIA DATA (MNI): Higher Gold Prices Supportive But Imports & Exports Rising

- AUSTRALIA OCT TRADE BALANCE A$+4385

The October merchandise trade surplus widened to $4.385bn after a downwardly-revised $3.71bn but it remains in the range it has been in since the start of 2024. The move was driven by monthly export growth exceeding imports for the second consecutive month and both are showing upward momentum. Stronger exports add to activity while imports signal that domestic demand is robust. The RBA is likely to be on hold beyond the 9 December decision.

AUSTRALIA DATA (MNI): Consumer Recovery in Place, RBA on Hold

October household spending is another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. With Governor Bullock saying yesterday that the output gap has likely closed, this strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision given that inflation is above the top of the band. Spending rose 1.3% m/m, highest since January 2024, to be up 5.6% y/y, fastest since September 2023 and up from the previous month's 5.1% y/y. The increase was broad-based across Australia.

FOREX: USD Index Weakness Persists, Extends Weekly Decline to 0.65%

- Broad dollar declines are persisting this week, prompting the USD index to print fresh pullback lows at 98.80. This extends the week’s decline to around 0.65%, and the two-week selloff now stands around 1.6%. Greenback weakness continues to be a reflection of a more dovish profile for the Fed under potential Kevin Hassett leadership and an associated more optimistic risk backdrop.

- The DXY posted a significant technical close on Wednesday, with the first daily close below the 50-day exponential moving average since early October. This impulse has generated several bullish signals across the rest of the G10 basket, and continues to bolster the optimistic sentiment for EM FX.

- The JPY is outperforming on the session, amid headlines suggesting key members of PM Takaichi’s government wouldn’t try to stop the BOJ if it decides to raise interest rates in December, a stance that makes a move more likely. The move lower for USDJPY remains shy of Monday's low at 154.67, the immediate support. Below here, the 50-day EMA at 153.34 is a more meaningful chart point.

- AUDUSD has also bridged the gap to 0.6618 resistance amid household spending providing another piece of data signalling robust domestic demand in Australia. The cautious RBA and firm risk backdrop is underpinning renewed AUD optimism.

- Elsewhere, Swedish Nov flash CPIF ex-energy inflation came in slightly below expectations, but should not change the near-term Riksbank outlook. USDSEK hovers within close range of a cluster of lows from October around 9.34. GBPUSD has also spent the session consolidating its impressive 1% rally yesterday, as pre-budget positioning was further squeezed.

- US weekly claims and September factory orders are on the calendar today alongside the Canadian Ivey PMI.

EGBS: Supply Contains Upside In Bunds, Bear Cycle Intact

- Supply from Spain and France has contained upside in major EGB futures this morning. Bunds (RXH6 is now the front contract) are -8 ticks at 128.54. Initial support is Tuesday’s low of 128.40. A bear cycle remains intact.

- The German curve is slightly bear flatter intraday. Broader focus into year-end remains on whether 10s30s can retest year-to-date highs of 66bps (currently 63.5bps). Germany’s 2026 issuance plan (usually released mid-December) may be an important catalyst here.

- 10-year OAT/Bund is down 1bp to 73.5bps. Today’s MT/LT auction saw mixed results, with the bid-to-cover ratio for the 10-year on-the-run line below last month’s outing. In politics, focus remains on the December 9 vote on the 2026 Social Security budget.

- The 10-year BTP/Bund spread consolidates yesterday’s narrowing below the 70bp handle, which seemingly came in response to stronger November PMI data.

- Meanwhile, Gilts have recovered from session lows in the wake of the much softer-than-expected construction PMI data and soft employment signals from the BoE DMP survey. BoE-dated OIS still pricing ~22bp of easing for this month’s meeting.

EQUITIES: E-Mini S&P Continues to Trade Close to Its Recent Highs

Recent gains in Eurostoxx 50 futures undermine a recent bearish theme and the contract continues to appreciate. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next, the 76.4% retracement of the Nov 13 - 21 bear leg. A break would open 5825.00, the Nov 13 high and a key resistance. First support lies at 5612.78, the 50-day EMA. A bullish theme in S&P E-Minis is intact and the contract is trading at its recent highs. Price also remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

- Japan's NIKKEI closed higher by 1163.74 pts or +2.33% at 51028.42 and the TOPIX ended 63.89 pts higher or +1.92% at 3398.21.

- Elsewhere, in China the SHANGHAI closed lower by 2.207 pts or -0.06% at 3875.793 and the HANG SENG ended 175.17 pts higher or +0.68% at 25935.9.

- Across Europe, Germany's DAX trades higher by 165.92 pts or +0.7% at 23859.92, FTSE 100 higher by 4.75 pts or +0.05% at 9697.11, CAC 40 up 32.54 pts or +0.4% at 8119.96 and Euro Stoxx 50 up 23.92 pts or +0.42% at 5718.48.

- Dow Jones mini up 53 pts or +0.11% at 48006, S&P 500 mini up 4.75 pts or +0.07% at 6866.5, NASDAQ mini up 19.25 pts or +0.08% at 25676.

Time: 10:00 GMT

COMMODITIES: Short-Term Gains for WTI Still Considered Technically Corrective

Short-term gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold is unchanged and remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4016.8. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $0.27 or +0.46% at $59.22

- Natural Gas up $0.01 or +0.16% at $5.005

- Gold spot down $2.94 or -0.07% at $4200.46

- Copper down $3.85 or -0.71% at $535.05

- Silver down $1.1 or -1.88% at $57.4095

- Platinum down $23.89 or -1.43% at $1651.75

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference | ||

| 04/12/2025 | 1300/1400 | ECB Cipollone Chairs Panel on Fiscal Policy | ||

| 04/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 04/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 04/12/2025 | 1500/1000 | * | Ivey PMI | |

| 04/12/2025 | 1500/1600 | ECB Lane at Fiscal Policy Conference | ||

| 04/12/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 04/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/12/2025 | 1730/1230 | Fed Vice Chair Michelle Bowman | ||

| 04/12/2025 | 1800/1900 | ECB de Guindos Speech at Business Innovation Awards | ||

| 05/12/2025 | 2330/0830 | ** | Household spending | |

| 05/12/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/12/2025 | 0730/0730 | DMO to publish issuance calendar for FQ4 | ||

| 05/12/2025 | 0745/0845 | * | Industrial Production | |

| 05/12/2025 | 0745/0845 | * | Foreign Trade | |

| 05/12/2025 | 0800/0900 | ** | Industrial Production | |

| 05/12/2025 | 0900/1000 | * | Retail Sales | |

| 05/12/2025 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit |