MNI US OPEN - Private Payrolls Expected to Drive NFP Increase

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW: WATCH THE FOREST, NOT JUST THE TREES

- ZELENSKYY PLANNING ELECTIONS IN UKRAINE AND VOTE ON PEACE DEAL: FT

- STREETING STILL READY TO CHALLENGE STARMER DESPITE SHOW OF UNITY: GUARDIAN

- CHINA CPI GROWTH SLOWS TO 3-MONTH LOW IN JANUARY

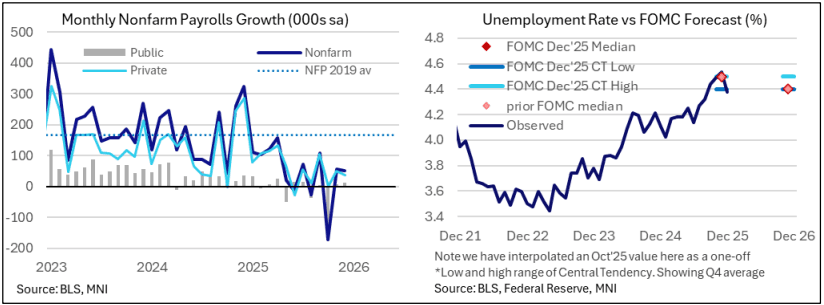

Figure 1: Recent US labour market developments

NEWS

MNI US PAYROLLS PREVIEW: Watch the Forest, Not Just the Trees

Wednesday sees an unusual BLS nonfarm payrolls report after a brief delay following last week’s government shutdown, with January details released at 0830ET. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take. Consensus looks for a circa 70k increase in nonfarm payrolls coming almost entirely from private payrolls. The unemployment rate is expected to hold at 4.4% after last month’s surprise drop to 4.38% from 4.54%, leaving a profile of broad stabilization on net since Aug/Sept. In doing so it ruled out a more dovish base case that seven FOMC members had pencilled in at the December SEP.

US (WSJ): House Rejects Speaker Johnson’s Effort to Block Tariff Votes

House lawmakers on Tuesday rejected an attempt by Speaker Mike Johnson (R., La.) to block votes on resolutions disapproving of President Trump’s tariffs—a stinging blow to his leadership that paves the way for lawmakers to potentially rebuke Trump’s signature economic policy. The procedural step failed with 217 opposed and 214 in favor, with three Republicans joining all 214 Democrats in voting against the measure, enough to sink it in the narrowly divided chamber.

US/ISRAEL/IRAN (BBG): Netanyahu, in Hasty Trip, to Warn Trump Against Narrow Iran Deal

Benjamin Netanyahu is set to meet Donald Trump in the White House on Wednesday as Israel’s concerns over a potential diplomatic deal between Iran and the US mount. The Israeli prime minister will use the hastily arranged visit to Washington to urge the US president to push for a sweeping roll-back of Iran’s military activities in the Middle East and its ballistic missile program, rather than settle for a narrower nuclear agreement.

US/IRAN (WaPo): Trump Mulls Second Aircraft Carrier Off Iran, as Netanyahu Flies to D.C. for Talks

On the eve of a visit from Israeli Prime Minister Benjamin Netanyahu, President Donald Trump said Tuesday that he was “thinking” of sending a second aircraft carrier to the Middle East, joining the U.S. armada already in the region that could bolster a strike on Iran if bilateral talks begun last week fail.

US/INDIA (BBG): US Changes India Trade Deal Statement, Sparking Confusion

The White House revised its fact sheet on the US-India trade agreement to adjust language around agricultural goods, adding to confusion about the deal already raised by farmer groups. In a revised statement, the US removed a reference to pulses — a staple food in India that includes lentils and chickpeas — and changed some phrasing around India’s offer to buy more American goods. An earlier version on Monday released by the White House said India would “eliminate or reduce tariffs” on a wide range of US food and agricultural products, including certain pulses.

UKRAINE (FT): Zelenskyy Planning Elections in Ukraine and Vote on Peace Deal

Ukraine has begun planning presidential elections alongside a referendum on any peace deal with Russia, after the Trump administration pressed Kyiv to hold both votes by May 15 or risk losing proposed US security guarantees. The move, according to Ukrainian and western officials and others familiar with the matter, comes amid intense pressure on Kyiv by the White House to wrap up peace negotiations between Ukraine and Russia in the spring. The plan aligns with a US push, outlined by Volodymyr Zelenskyy to reporters last Friday, to have all documents signed to bring Europe’s largest conflict since the second world war to an end by June.

UK (The Guardian): Streeting Still Ready to Challenge Starmer Despite Show of Unity, Allies Say

Allies of Wes Streeting expect him to try to challenge Keir Starmer’s leadership within weeks, despite the health secretary insisting he backs the prime minister and is not intending to move against him, the Guardian has been told. Starmer attempted to regain authority over his party on Tuesday after a tumultuous day in Westminster during which he was denounced by the Scottish Labour leader Anas Sarwar and lost his director of communications. The prime minister said on Tuesday he would “never walk away” from his task of changing the UK, and was bolstered further by public displays of support from both Streeting and the Greater Manchester mayor, Andy Burnham.

UK (Politico): Rebuilding EU Ties ‘The Biggest Prize’ for British Economy, Reeves Says

Britain's chief finance minister will argue closer integration with the EU offers the U.K. the best opportunity for higher economic growth — ahead of links with the U.S. and China. Rachel Reeves will say Wednesday evening that stronger ties with the European bloc are “the biggest prize” for Britain, while stressing that calculation isn't “about choosing sides but about geography.” “There are three big economic blocks: U.S., China and Europe,” Reeves will say, according to extracts shared with POLITICO.

EU/AUSTRALIA (BBG): Australia and EU Enter Final Stretch in Long-Running Trade Talks

Australia’s trade minister is headed to Brussels for talks with European counterparts in an attempt to successfully conclude long-running talks on a trade deal, with both sides keen to sign an agreement and tighten ties in an increasingly unpredictable global environment. Don Farrell will meet with European Union Commissioner for Trade and Economic Security Maros Sefcovic and EU Commissioner for Agriculture and Food Christophe Hansen on Thursday for formal talks. “Australia is ready to do a deal, but we don’t do deals for deals sake,” Farrell said in a statement before departing.

RBA (MNI): Stronger Demand Drove Hike - RBA's Hauser

The Reserve Bank of Australia’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply, Deputy Governor Andrew Hauser said at an industry event Wednesday. “The reason policy turned around in February is because the facts changed,” he said, referring to last week’s decision. The RBA had been surprised by the rebound in the global economy over 2025, which lifted demand for Australian exports, Hauser noted.

CORPORATE (WSJ): Activist Investor Pushes Warner to Walk Away From Netflix Deal

Activist investor Ancora Holdings has built a roughly $200 million stake in Warner Bros. Discovery and is planning to oppose Warner’s deal to sell its movie and television studios and HBO Max streaming service to Netflix, according to people familiar with the matter. Ancora, which could announce its position as soon as Wednesday, believes that Warner failed to adequately engage with David Ellison’s Paramount Skydance after it made a rival all-cash offer for the entire business, including its cable-network group, at $30 a share, the people said.

DATA

ECB DATA (MNI): Negotiated Wage Growth Still Below 3% by End-26, Another Upward Revision

The ECB's forward looking wage tracker continues to indicate negotiated wage growth of just below 3% by the end of this year. Note that at last week's press conference, President Lagarde stressed that "the contribution to overall wage growth from payments over and above the negotiated wage component remains uncertain" - this followed the stronger-than-expected compensation per employee reading in Q4 2025. The wage tracker excluding one-off payments was 2.693% in the February updated, up from 2.681% in December. Note that upward revisions have become common in this series.

CHINA DATA (MNI): January CPI Growth Slows to 3-Month Low

- CHINA JAN CPI +0.2% Y/Y VS MEDIAN +0.4%; DEC +0.8%

China’s Consumer Price Index rose 0.2% y/y in January, down from December's 0.8% growth to hit a three-month low, missing expectations for a 0.4% gain, according to data from the National Bureau of Statistics released Wednesday. The slower growth was mainly due to a higher comparison base, as January of last year was the month of the Spring Festival, the NBS said, also citing fluctuations in international oil prices that led to a wider decline in energy prices. On a monthly basis, CPI rose 0.2%, the same as the previous 0.2% gain. Core CPI, which excludes food and energy, rose 0.3% m/m to hit a 6-month high.

FOREX: DXY Extends Reversal Lower, USDJPY Approaching 152.10 Support

- Although much of the focus has been on the yen over the past two sessions, the Ice USD index has been gradually edging lower, approaching 96.50 as we await the key US employment figures later today. It’s been well noted that the DXY’s recovery to the December lows around the 98.00 mark appears to have provided an attractive entry point for those looking to reengage shorts.

- Yesterday’s retail sales data has certainly added to the renewed greenback pessimism, alongside the dovish repricing across the US curve. This dynamic provides an important backdrop for today’s payrolls report, as weak figures may bolster bets on imminent easing from the Fed. The data will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

- With Japan out for a national holiday today, the JGB stabilisation theme has allowed the yen to extend its post-election upswing, with the US data assisting the squeeze. USDJPY broke swiftly through the 100-day MA on Tuesday, and spot has traded down to 152.80 overnight, narrowing the gap substantially to 152.10 support.

- The sharp downswing for GBPJPY has seen spot extend below the 50-day EMA to fresh 2026 lows. The average has been a notable pivot given the fact we have not posted a daily close below it since October, and it acted as perfect support on Jan 26. Next support is seen at 206.78, the Dec 16 low.

- Elsewhere, AUDUSD broke above the 0.71 handle overnight after RBA's Hauser said the country's inflation rate is too high and the RBA will take all necessary measures to bring it under control. 0.7128 highs bring us closer to the 2023 peak, at 0.7158.

- MBA Mortgage Applications are scheduled ahead of payrolls. Fed's Schmid, Bowman and Hammack will appear while ECB hawk Schnabel is also scheduled.

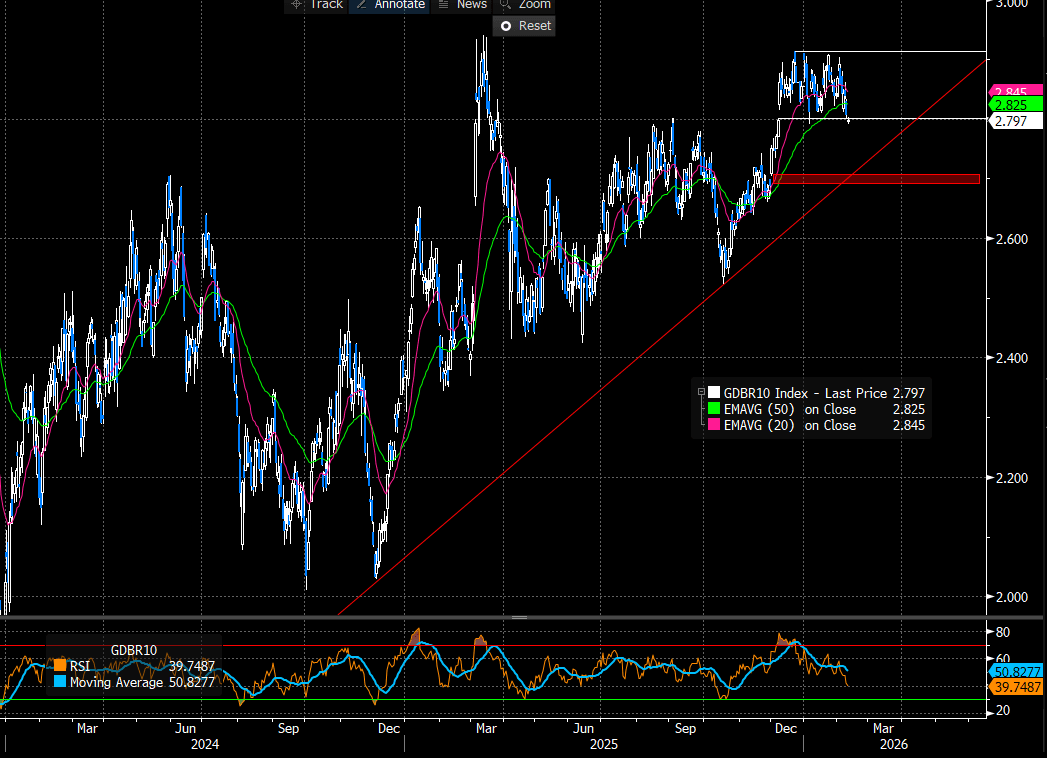

EGBS: 10-Year Bund Yields Pierce 2.80% Ahead of UK Labour Market Report

Core FI yields are biased marginally lower ahead of today’s key US labour market release. 10-year Bund yields have pierced 2.80% – a level that has contained downside on a closing basis since early December. While still some way off, the 2.70% level is interesting from a technical perspective. Alongside being a psychological round number, it aligns closely with trendline support drawn from the August 2022 low.

- Long-end supply has been in focus today, with France holding a 30-year syndication and Germany also selling 30-year Bunds. Slovakia is also holding a syndication today, while Greece and Portugal have held conventional auctions.

- 10-year EGB spreads to Bunds are little changed. The BTP/Bund spread continues to hover around 61bps, struggling to consolidate below the 60bp figure.

- Bund futures are +5 ticks at 128.69. The breach of 128.58, the Jan 19 high and a key short-term resistance, strengthens the short-term bullish condition. The break higher signals scope for an extension towards 128.89, a Fibonacci retracement point.

- In data, the ECB's forward looking wage tracker continues to indicate negotiated wage growth of just below 3% by the end of this year. Italian industrial production was broadly in line with consensus at -0.4% M/M (Vs -0.5% prior).

Figure 2: 10-year bund yields

Source: Bloomberg Finance L.P

GILTS: Firmer as Equities Soften, Politics Still Dominates Headlines

Downticks in equities support gilts through early London trade, with solid demand at the GBP300mln 4.25% Dec-49 gilt tender also noted.

- Futures +7 at 90.95, respecting yesterday’s high (91.00).

- Bears remain in technical control after piercing key support earlier in the week. Initial support at this week’s low (89.76), while initial resistance is located at the 20-day EMA (91.07).

- Yields ~1.5bp lower across most of the curve.

- Short end pricing steady, showing ~45bp of easing through November.

- Political matters remain at the fore after PM Starmer received public ministerial support on Monday, calming speculation surrounding an expedited leadership challenge/confidence vote.

- The latest press speculation, via Guardian source reports, suggests that Health Secretary Streeting could challenge PM Starmer within weeks (after the Gorton & Denton by-election). Most still expect any serious leadership challenge to come after the local elections in May.

- Little of note on the UK economic calendar, with preliminary Q4 GDP data due tomorrow.

- The delayed U.S. NFP release will headline the wider calendar today, with the recent run of soft U.S. jobs data conditioning markets for a softer-than-expected print.

- Outside of the tender, the DMO has noted that it will launch a new green gilt maturing on 7 March 2037 in the week commencing 9 March. We expect a GBP6.5bln transaction size for now.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.557 | -17.0 |

Apr-26 | 3.499 | -22.8 |

Jun-26 | 3.412 | -31.5 |

Jul-26 | 3.349 | -37.8 |

Sep-26 | 3.315 | -41.2 |

Nov-26 | 3.278 | -44.9 |

Dec-26 | 3.286 | -44.2 |

EQUITIES: Tuesday's Cycle High for EuroStoxx Futures Reinforces Bullish Theme

The medium-term trend condition in EuroStoxx 50 futures remains bullish and yesterday's fresh cycle high reinforces the bull theme. The move higher paves the way for a climb towards 6100.00 and 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5890.56, the 50-day EMA. Clearance of this average would highlight a short-term top and signal scope for a deeper pullback. The firm reversal higher on Feb 6 in S&P E-Minis refocuses attention on the primary uptrend and key resistance at 7043.00, the Jan 28 high. Clearance of this level would confirm a resumption of the primary uptrend and mark the end of a flat correction in the contract. Key short-term support has been defined at 6751.50, the Feb 6 low, where a break is required to highlight a top and a stronger short-term reversal.

- In China the SHANGHAI closed higher by 3.611 pts or +0.09% at 4131.985 and the HANG SENG ended 83.23 pts higher or +0.31% at 27266.38.

- Across Europe, Germany's DAX trades lower by 80.22 pts or -0.32% at 24908.04, FTSE 100 higher by 38.7 pts or +0.37% at 10392.8, CAC 40 down 42.19 pts or -0.51% at 8285.69 and Euro Stoxx 50 down 23.81 pts or -0.39% at 6023.25.

- Dow Jones mini up 37 pts or +0.07% at 50308, S&P 500 mini down 2.5 pts or -0.04% at 6959, NASDAQ mini down 43.5 pts or -0.17% at 25172.5.

Time: 10:30 GMT (05:30 ET)

COMMODITIES: WTI Futures Narrow Gap to Bull Trigger at $66.48

A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $62.33. The 50-day EMA lies at $60.63. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger to watch has been defined at $66.48, the Jan 30 high. The latest bounce in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude up $0.9 or +1.41% at $64.85

- Natural Gas up $0 or +0.13% at $3.12

- Gold spot up $44.51 or +0.89% at $5071.67

- Copper up $7.5 or +1.27% at $598.85

- Silver up $4.08 or +5.05% at $84.9387

- Platinum up $91.98 or +4.41% at $2179.76

Time: 10:30 GMT (05:30 ET)

| Date | GMT/Local | Impact | Country | Event |

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture at Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada Meeting Minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack | ||

| 11/02/2026 | - | *** | New Loans | |

| 11/02/2026 | - | *** | Money Supply | |

| 11/02/2026 | - | *** | Social Financing | |

| 12/02/2026 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/02/2026 | 0700/0700 | ** | Index of Services | |

| 12/02/2026 | 0700/0700 | *** | GDP First Estimate | |

| 12/02/2026 | 0900/1000 | ECB's Cipollone at Commissione Europa Conference | ||

| 12/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 12/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 12/02/2026 | 1345/0845 | BOC's Rogers Panel Talk on Productivity | ||

| 12/02/2026 | 1500/1000 | *** | NAR Existing Home Sales | |

| 12/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 12/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 12/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 12/02/2026 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/02/2026 | 1830/1930 | ECB's Lane at the World Ahead 2026 Gala Dinner |