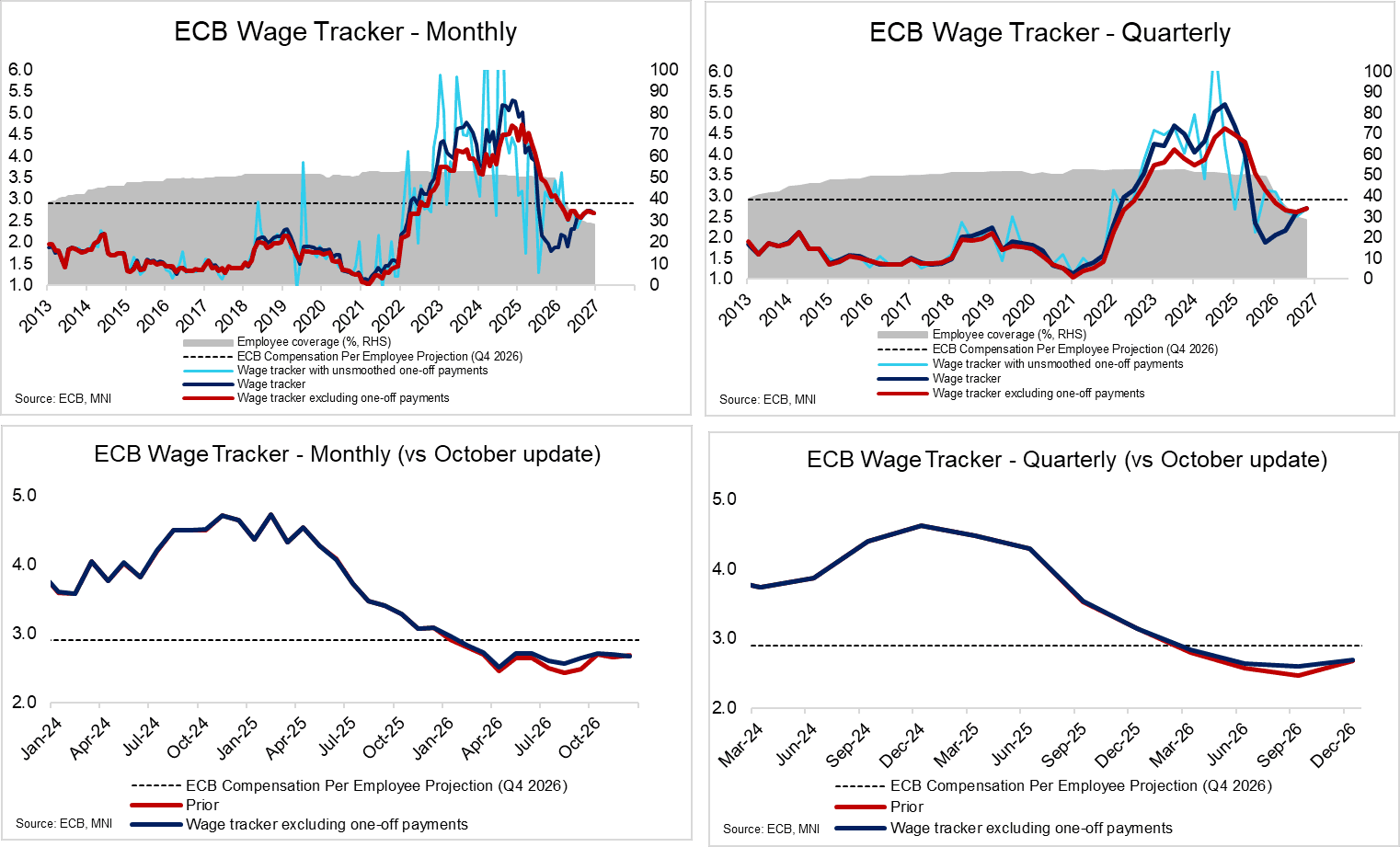

ECB: Negotiated Wage Growth Still Below 3% By End-26, Another Upward Revision

The ECB’s forward looking wage tracker continues to indicate negotiated wage growth of just below 3% by the end of this year. Note that at last week’s press conference, President Lagarde stressed that “the contribution to overall wage growth from payments over and above the negotiated wage component remains uncertain” – this followed the stronger-than-expected compensation per employee reading in Q4 2025.

- The wage tracker excluding one-off payments was 2.693% in the February updated, up from 2.681% in December.

- Note that upward revisions have become common in this series. For example, the Q2 2026 reading of 2.650% was 2.582% in December and 2.489% in October.

- From the ECB’s press release: “The rise in the wage path over the course of the year is related to the dissipation of the mechanical downward effect of large one-off payments that were made in 2024 but not in 2025. These mechanical effects are expected to virtually disappear over the course of 2026, and the wage trackers with one-off payments (smoothed and unsmoothed) and without one-off payments are expected to converge as such payments become less relevant. The ECB wage tracker also suggests that there is less dispersion in negotiated wage pressures across the different euro area countries in 2026 than in previous years.”

- “As new agreements are being signed and coverage of contracts reaching beyond 2026 is gradually increasing, the forward-looking horizon of the wage tracker will be extended to the first quarter of 2027 in the July 2026 data release.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

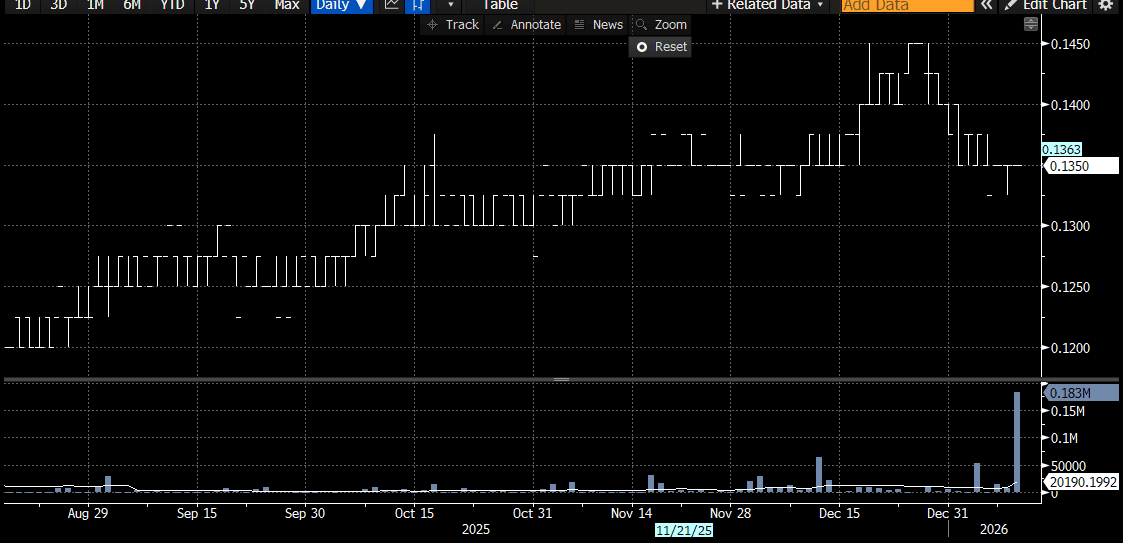

EURIBOR: Another huge ESTR vs Euribor spread

Another HUGE ESTR vs Euribor trades this Morning.

- ESTR/ERM7 trades at 13.5 in some 182k, these are all cumulative and a record volume trade.

Recall on Friday, ESTR/ERH7 was bought for 13.5 in 230k, said to have been related to a rebate.

(Chart source: MNI/Bloomberg Finance LP).

EGBS: Familiar Themes In Sell-Side Views After Initial '26 Trade

Sell-side notes that we have seen generally maintain a bias for higher long end yields in Germany over the medium-term, alongside the potential for ongoing, albeit more limited, instances of peripheral outperformance vs. semi-core/core. Elsewhere, most don’t expect meaningful fresh widening for OATs.

- Goldman Sachs: They think improving growth will outweigh structural challenges for Bunds and expect 10s to end the year at 3.25%. They think sovereign credit longs represent opportunity for returns in the current macro environment. For OATs, they argue that the likely passing of a formal budget in France in H126 should catalyse a further reduction in idiosyncratic risk premium. They caution that H226 may see spreads wider as markets look to the end of NGEU support and 2027 elections in Italy and France.

- J.P.Morgan: They write “Greek bonds have outperformed sharply vs. Spain and have moved from trading too wide to too tight”. As a result, they recommend closing overweight GGBs 10s vs. SPGBs, further aided by their expectations for the launch of a new 10-Year benchmark GGB in the coming weeks. They await better levels to scale into fresh overweight exposure in both GGBs & SPGBs.

- Natixis: Hold a marginal long near-term bias for duration after Bund yields moved back towards ’25 highs and investors showed demand ahead of those levels, albeit retaining a medium-term view for a gradual rise in Bund yields. They argue that the EUR short end should price the risk of rate cuts in ’26, while holding a curve steepening view driven by the ongoing rebuild of German term premium. They also suggest that hedge funds appear to have less interest in short OATs. They believe that related pressure is contained and expect the idiosyncratic risk in OATs to decline further once the markets have clarity on the 2026 budget. They continue to expect limited tightening in peripheral spreads, supported by sustained investor demand and gradually improving fundamentals, maintaining a long SPGB 04/34 vs. RAGB 05/34 recommendation.

- Societe Generale: They continue to expect Italian outperformance within EGBs this year and favour being long Italy vs. Germany. They think longs in the 5-/10-/30-Year BTP fly looks appealing. They also like 5-/15-Year BTP flatteners vs. Bund with a focus on supply dynamics (having previously recommended a similar 10-/30-Year box). Elsewhere, they recommend Bund or EUR swap 5-/10-Year+ curve steepeners as “ECB rate hikes expectations are being postponed”, with a focus on geopolitical risks and rebuilding term premia.

SONIA OPTIONS: Call Spread vs Put Spread

SFIZ6 96.90/97.00cs vs 96.50/96.40ps, bought the cs for 1 in 10k.