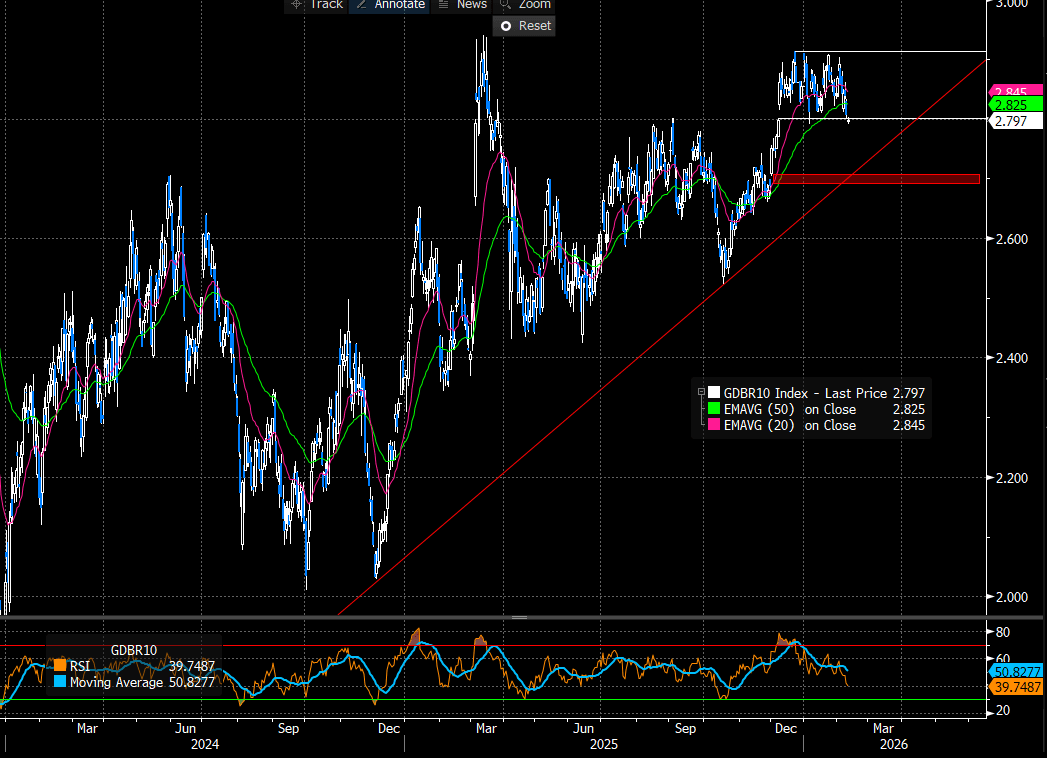

EGBS: 10-year Bund Yields Pierce 2.80% Ahead Of UK Labour Market Report

Core FI yields are biased marginally lower ahead of today’s key US labour market release. 10-year Bund yields have pierced 2.80% – a level that has contained downside on a closing basis since early December. While still some way off, the 2.70% level is interesting from a technical perspective. Alongside being a psychological round number, it aligns closely with trendline support drawn from the August 2022 low.

- Long-end supply has been in focus today, with France holding a 30-year syndication and Germany also selling 30-year Bunds. Slovakia is also holding a syndication today, while Greece and Portugal have held conventional auctions.

- 10-year EGB spreads to Bunds are little changed. The BTP/Bund spread continues to hover around 61bps, struggling to consolidate below the 60bp figure.

- Bund futures are +5 ticks at 128.69. The breach of 128.58, the Jan 19 high and a key short-term resistance, strengthens the short-term bullish condition. The break higher signals scope for an extension towards 128.89, a Fibonacci retracement point.

- In data, the ECB's forward looking wage tracker continues to indicate negotiated wage growth of just below 3% by the end of this year. Italian industrial production was broadly in line with consensus at -0.4% M/M (Vs -0.5% prior).

Figure 1: 10-year Bund Yields (Source: Bloomberg Finance L.P)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Soft REC Jobs Report Counters Some Of U.S. Tsy-Driven Sell Off

Gilt yields have edged higher on cues from the U.S. long end stemming from the latest threats to Fed independence.

- The U.S. DoJ served Fed Chair Powell with subpoenas threatening criminal indictment linked to the renovation of the central bank’s headquarters.

- There is some counter from signs of further softening in the UK labour market.

- Gilt futures traded as low as 92.30 before recovering, last -8 at 92.40.

- Initial support at the Jan 8 low (91.84), while Fibonacci resistance is clustered in above Friday highs (92.57, 92.72 & 92.91).

- Bulls remain in technical control despite this morning’s shallow pullback.

- Gilt yields 0.5-1bp higher, curve steeper.

- Bulls continue to look to the ’25 low in 10s (4.363%), which equates to 92.69 in futures today. That yield level protects rising triangle support (4.335% today).

- SONIA futures effectively unchanged, with the downtick in the long end reversing early dovish moves. ~46bp of BoE easing priced through December, next 25bp cut still not quite fully priced until the end of June.

- The latest KPMG-REC Report on Jobs showed a further deterioration on the quantities side, while there were some mixed signs on wage pressures.

- We think that the wage signal in this survey is of lesser importance to the MPC than the Agents' Pay Survey or the DMP data. Meanwhile, the continuing softening on the quantities side is notable.

- Little of note on the UK macro calendar for the remainder of the day. The BoE will sell GBP800mln of short bucket gilts from its APF this afternoon.

Fig. 1: UK 10-Year Gilt Yields (%)

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Feb-26 | 3.712 | -1.3 |

Mar-26 | 3.621 | -10.4 |

Apr-26 | 3.503 | -22.1 |

Jun-26 | 3.430 | -29.5 |

Jul-26 | 3.350 | -37.5 |

Sep-26 | 3.313 | -41.2 |

Nov-26 | 3.276 | -44.9 |

Dec-26 | 3.267 | -45.8 |

FOREX: USD Slips as DoJ Targets Powell

- Greenback has stabilised at the session's lower levels, helping keep EURUSD propped toward 1.1700 and GBPUSD above the Friday high of 1.3451. Resultantly, the USD is weaker against all others in G10. The sustainability, and potential extension, of this USD weakness will take the lead from the US curve - which trades bear steeper so far Monday. Following Powell's video statement, it seems Trump's next comments on the topic are the primary market risk - even as the President denied knowledge of the filings over the weekend.

- The primary beneficiaries have been CHF and EUR as today's move slows, but only partially reverses, the YTD rally in USDCHF and YTD weakness in EURUSD. EUR's growing status as a haven is clear in the today's market reaction - and this will likely remain the case through near-term periods of market fragility, even as the outside pricing of ECB hikes further out the curve has faded.

- Despite the broad USD weakness, JPY has failed to receive a meaningful boost to start the week, with a brief flurry down to 157.52 well supported during APAC hours. Domestic factors are certainly playing their part here, as Friday’s reports of PM Takaichi dissolving the Lower House and associated speculation that she could call for a snap election continues to rise. The Yomiuri newspaper has reported that Feb. 8 or Feb. 15 are likely dates for this to occur.

- Technically, last week’s breach of 157.89 for USDJPY was a meaningful development, confirming a resumption of the medium-term uptrend. The next significant topside target will be 158.87, last year’s high and a key resistance. Support to watch lies much lower down at 155.35, the 50-day EMA.

- Typically for a Monday, there are no major data releases scheduled. This should keep focus on any potential comments concerning the Fed's subpoenas from Trump. The President is due at several public events later today, and also holds a call with the Mexican President. Central bank speak today includes Fed's Bostic, Barkin & Williams as well as ECB's Villeroy.

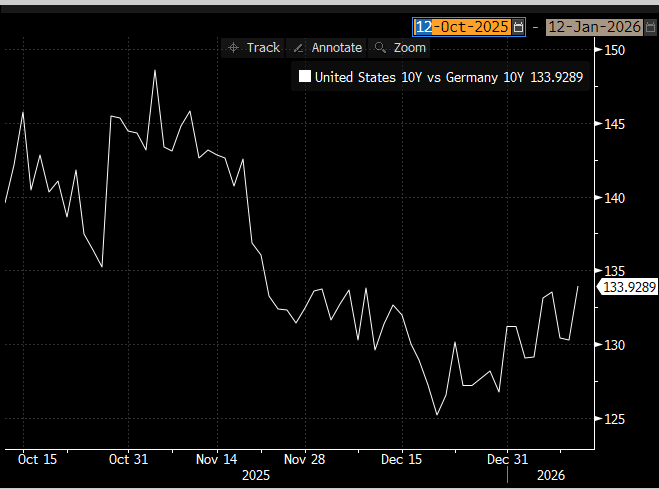

EGBS: Bunds Outperform Treasuries Amid Fresh Fed Independence Concerns

The German curve outperforms its US counterpart, with renewed concerns around Fed independence not spilling over into EGB markets. German yields are up to 1bp lower across the curve, with US yields flat to +5bps in a bear steepening move. The 10-year UST/Bund spread is 3.5bps wider at 134bps.

- Bund futures are unchanged at 127.95. The rally since last Monday does undermine the bear theme and attention is on resistance around the 50-day EMA, at 128.29. A clear break of this average would highlight a stronger reversal and signal scope for a continuation higher.

- The EFSF is holding a dual tranche syndication, launching a new 3- and 10-year bond. We expect a E5-7bln size.

- 10-year EGB spreads to Bunds are biased up to 0.5bps wider. Focus in France remains on budget negotiations, with scope for compromises seeming increasingly slim.

- Regional news flow hasn’t been too market moving. China and the EU have agreed on the need to provide guidance on price commitments for Chinese exporters of pure electric vehicles to the EU.

- Meanwhile, ECB’s Muller pushed back on near-term rate moves in either direction. In line with market pricing, he suggested a rate hike is possible “a few years ahead”.

- The Eurozone Sentix survey was stronger-than-expected at -1.8 (vs -5.0 cons, -6.2 prior).

Figure 1: 10-year UST/Bund Spread (Source: Bloomberg Finance L.P)