MNI US OPEN - Payrolls Report Highlights Busy US Docket

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW - SOFTER DEMAND MEETS SUPPLY CONSTRAINT

- RULE VOTE ON OBBB PASSES 219-213 AS CONSERVATIVE HOLDOUTS OFFER BACKING

- STARMER SEEKS TO END SPECULATION ABOUT REEVES’ FUTURE

- BOJ’S TAKATA SAYS RATE HIKES TO RESUME AFTER TEMPORARY PAUSE

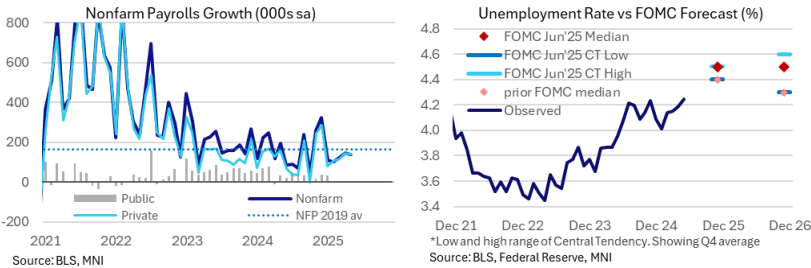

Figure 1: Recent US labour market developments

NEWS

MNI US PAYROLLS PREVIEW: Softer Demand Meets Supply Constraint

The June payrolls report sees a rare Thursday release at 0830ET owing to Independence Day on Friday, as part of a particularly heavy docket that also includes ISM Services. There are few alternative June labor indicators to go off as the release also lands early in the month, with the most notable being a pronounced uplift in jobless claims. Broad Bloomberg consensus sees nonfarm payrolls rising a seasonally adjusted 110k in June after 139k in May, with private dealer analysts a little lower at 103k and the Bloomberg Whisper currently at 100k.

US (MNI): Rule Vote on OBBB Passes 219-213 as Conservative Holdouts Offer Backing

Conservative holdouts among House Republicans have flipped their support on a rule vote, seen as a test run for the One Big Beautiful Bill, ensuring passage by a 219-213 margin. The final vote is expected at 08:00ET (13:00BST, 14:00ET). With the passage of the rule vote, there is now little jeopardy ahead of the final vote, with its passage all-but-assured.

US/CHINA (BBG): Top Chinese Official Softens Tone on US, Says War ‘Unimaginable’

A senior Chinese official said he was “optimistic” about the future of his nation’s ties with the US, among the most upbeat comments given by Beijing in recent weeks about a relationship upended by Donald Trump’s tariffs. Both the Chinese and the Americans are hoping for a “friendly, good” relationship between their countries, and politicians are expected to heed the will of the people, Liu Jianchao, head of the Communist Party’s International Department, said at the government-backed World Peace Forum on Thursday.

US/CHINA/VIETNAM (MNI): China Assessing US/Vietnam Deal - MOFCOM

MNI (Beijing) China is assessing the recent U.S. Vietnam trade agreement and will resolutely counter any party reaching a deal at the expense of China’s interests, said He Yongqian, spokesperson for the Ministry of Commerce on Thursday. The United States' imposition of reciprocal tariffs on global trading partners was typical unilateral bullying, He reiterated. The outcome of the upcoming China-EU Leaders’ Summit scheduled is likely to depend on Brussels' negotiations with Washington by the July 9 deadline to avoid steep U.S. tariffs, advisors in Beijing recently told MNI.

US/INDONESIA (BBG): US, Indonesia to Sign $34B Trade and Investment MoU: Minister

The US and Indonesia will sign a $34 billion trade and investment MoU on July 7, Indonesian Coordinating Economic Minister Airlangga Hartarto tells reporters in Jakarta. MoU covers investment plans in the US, as well as the purchase of agricultural goods and $15.5b of energy goods from the US, he says. Indonesian delegation already standing by in Washington. In response to questions about Indonesia’s negotiations over US tariffs, he says, “let’s just wait for the final announcement later.”

UK (BBC): Starmer Seeks to End Speculation About Reeves’ Future

Sir Keir Starmer has sought to calm the markets and end speculation about Rachel Reeves' future after the chancellor was seen crying in the House of Commons. The pound plummeted and government borrowing costs rose after the incident at prime minister's questions on Wednesday, when Sir Keir failed to guarantee that Reeves would keep her job. He later insisted that he and Reeves were in "lockstep", telling the BBC that "she will be chancellor for a very long time to come".

UK (MNI): When Could the Budget Be?

We think that the most likely dates for a UK Budget is 5 November (although 29 October remains plausible). There are a few constraints around the timing. The most obvious is that parliamentary recess is avoided. There are recesses in the autumn between 13 September to 6 October and between 7-10 November. Perhaps most importantly this year, benefits and pensions are based on the September CPI figures - which is not due for release until 22 October. This is relatively late (and a week later than last year). The Low Pay Commission also uses the September CPI figures as an input into its recommendations for the minimum / National Living Wage. This takes a little time to finalise in the numbers so the Budget being a week later than last year makes sense to us.

BOJ (BBG): BOJ Board Member Says Rate Hikes to Resume After Temporary Pause

The Bank of Japan’s rate hike cycle will resume after “only” a temporary pause, Board Member Hajime Takata warned, keeping his hawkish tone even after President Donald Trump clouded the economic outlook by threatening to impose tariffs on Japanese goods even higher than those previously touted. “I believe that the bank is currently only pausing its policy interest rate hike cycle and should continue to make a gear shift after a certain period of ‘wait and see,”’ Takata said Thursday in a speech to local business leaders in Mie, in central Japan.

JAPAN (BBG): Japan’s 2025 Wage Talks Conclude With Highest Gain in 34 Years

Japan’s annual wage negotiations concluded with the largest pay increase in 34 years, an outcome that supports the central bank’s view that a cycle of higher wages and prices is emerging. Workers at 5,162 companies affiliated with the nationa’s largest union federation Rengo secured an average wage increase of 5.25% in this year’s negotiations, according to the final update of pay deals announced by the union group on Thursday. While the figure came in lower than the preliminary 5.46% reported in March, it still marks the highest growth rate since 1991.

JAPAN (BBG): Japanese PM Ishiba’s Make-or-Break Election Campaign to Kick Off

Campaigning for Japan’s upper house election starts Thursday with the fate of Prime Minister Shigeru Ishiba and his minority government hanging in the balance. Since its inception last October, the Ishiba administration has had mixed success. While the premier managed to woo smaller parties to pass the budget, his administration also spent months trying to hash out a trade deal with Washington with seemingly little to show for it.

THAILAND (MNI): Opposition Parties Agree to Hold Off on Censure Motion

The Straits Times reported that Thai opposition parties agreed to hold off on triggering a no-confidence vote against suspended Prime Minister Paetongtarn Shinawatra until the Constitutional Court issues a verdict in her ethics case. This was the conclusion from a meeting of leaders of five opposition parties, including the Bhumjaithai Party (BJT), which recently pulled ouf of the ruling coalition. Main opposition People's Party (PP) leader Natthaphong Ruengpanyawut said that they will work together to prevent a political deadlock.

DATA

EUROZONE DATA (MNI): June Services PMI Revised Up, But Sluggish Downward Trend Intact

- EUROZONE JUNE SERVICES PMI 50.5 (50.0 FLASH, 49.7 MAY)

- GERMANY JUNE SERVICES PMI 49.7 (49.4 FLASH, 47.1 MAY)

- FRANCE FINAL JUNE SERVICES PMI 49.6 (FLASH 48.7, MAY 48.9)

Following upward revisions in France and Germany, the Eurozone-wide June services PMI was revised to 50.5 (vs 50.0 flash, 49.7 prior). We estimate the Germany/France services PMI at 49.7 (vs 49.1 flash, 47.9 prior) and the ex-Germany/France index at 51.9 (vs 51.5 flash, 52.8 prior). As such, services convergence between the outperforming semi-core/peripheral states and the two largest Eurozone economies is continuing. However, the Eurozone-wide services PMI remains on a sluggish, slightly downward, trend.

ITALY DATA (MNI): June Services/Composite PMI Expansionary But Export Demand Softens

- ITALY JUNE SERVICES PMI 52.1 (52.5 F'CAST, 53.2 MAY)

The Italian services PMI was slightly weaker than expected at 52.1 (vs 52.5 cons, 53.2 prior), while the composite reading slipped to a 3-month low of 51.1 (vs 51.6 cons, 52.5 prior). Like Spain, although the index remains in expansionary territory, there are some signs of softening demand, particularly from abroad.

UK DATA (MNI): Surprisingly Strong Expected Employment Growth

A mixed DMP report with realised employment growth soft but expected employment growth picking up surprisingly. Realised and expected price growth were broadly in line with previous values. The most notable part of this report is the expected employment growth, which puts a question mark over other recent data which showed the deceleration in the labour market if anything picking up pace. This is also clearly in contrast to the PMI data. Of course the single month data here are not a full sample - so the MPC will be careful not to overinterpret this data and will have another DMP reading before the MPR and their next policy decision, anyway.

UK DATA (MNI): Upward Revision to Services PMI, Sales Driven by Domestic Markets

- UK JUNE SERVICES PMI 52.8 (51.3 FLASH, 50.9 MAY)

The UK services PMI was revised up notably to 52.8 (vs 50.7 flash, 50.9 prior). Highlights from the services PMI release: "Survey respondents attributed rising output levels to organic sales growth, supported by generally improving business and consumer spending" "Renewed improvements in overall sales volumes were driven by greater demand in domestic markets. In contrast, export sales decreased for the third month running"

SWITZERLAND DATA (MNI): Swiss CPI Details Confirm Upside From Imported Goods

- SWISS JUN CPI +0.2% M/M, +0.1% Y/Y

Looking at the details of the June Swiss CPI print confirms that upside pressure came from (imported) core goods (non-energy industrial goods), with both the clothing and household items categories adding in contribution (alongside some hospitality upside contribution, which came mainly from the hotels category). Our reading is that today's print should, on the margin, take away from

imminent pressures for the SNB to further reduce its policy rate into negative territory.

SWEDEN DATA (MNI): Markets Discouting Strong Services PMI

The Swedish services PMI surged to 54.6 in June, above May's 50.9 for the highest since late-2022. The print comes in sharp contrast to the services sentiment series in the June Economic Tendency Indicator (ETI), which slipped to 92.9 (vs 95.5 prior). We are more inclined to focus on the signals from the ETI than the PMI, with the latter more volatile and less closely followed by the Riksbank. Markets seem to agree, with SEK once again underperforming the G10 despite the data.

JAPAN DATA (MNI): Offshore Investors Buy Both Local Bonds & Equities

In the week ending June 27 we saw offshore investors return to both Japan bond and equity markets, see the table below. The prior week (to end June 20) saw the first net selling of Japan stocks since the end of March, but with 651.3bn in net inflows last week we resumed positive trends in this space. Since the start of April, offshore net flows into local stocks have been over 7.3trln. Offshore investors also purchased local bonds last week in decent size. This markets the fourth out of the last five weeks we have seen positive inflows (cumulative inflows over this period are just over 2.5trln).

AUSTRALIA DATA (MNI): Trade Surplus Falters on Wekaer Exports, Import Rise

- AUSTRALIA MAY TRADE BALANCE A$+2238

Australia's May trade data was softer than forecast, with the trade surplus printing at A$2.24bn, versus the A$5bn forecast. The prior April surplus was revised down to a surplus of A$4.859bn. This was the lowest trade surplus since 2020. Exports fell -2.7%m/m, after a revised fall of 1.7% in April. Import momentum improved to +3.8%m/m, after a 1.6% gain in April. On the export side, some softness was evident in coal exports, along with other mineral fuels. Iron ore exports held up. Rural exports also fell.

TURKEY DATA (MNI): Favourable Headline Inflation Figure Bolsters Argument for July Rate Cut

- TURKEY JUN CPI +1.37% M/M

Consumer prices in Turkey rose +35.1% Y/Y in June from +35.4% in May, a slightly faster pace of disinflation compared to the +35.3% expected. Prices rose 1.37% on a month-on-month basis compared to 1.53% prior, while core inflation stood at an annual +35.64% (a touch above last month’s +35.37%). The data will bolster the argument for a restart of the rate cut cycle at the July 24 rate-setting meeting, at which policymakers were already expected to deliver a substantial cut to the one-week repo rate. We noted yesterday that local sell-side desks are expecting an easing step of as much as 350bps

FOREX: GBP Holds Bounce as Starmer Backs Up Chancellor, Affirms Fiscal Rules

- GBP is holding the entirety of the bounce off Wednesday lows, with GBP/USD over a point off yesterday's lows as the UK PM looks to bolster the Chancellor's position and reinforce to markets that she will remain in place for the long-term, despite rampant speculation over her departure during the Wednesday session.

- The durability of today's GBP strength will depend on the market buying into the view that the government have sufficient fiscal options to head off any market instability later this year, particularly as the fiscal headroom available into the Autumn Budget was much diminished by the passage of a watered down welfare bill earlier this week.

- GBP spot volatility this week serves as a further reminder that there remains a considerable political risk premium on the currency, and surprising political newsflow can still hold sway over both rates markets and the currency. This keeps markets on alert for further upside risks in EUR/GBP, which sees resistance at 0.8670 and 0.8715.

- The USD Index is flat-to-higher headed through the crossover. Markets are looking to test whether prices have successfully formed a base at 96.377 - this week's low - which could prompt a S/T correction and recovery for prices off oversold levels. With Fed pricing for the July meeting indicating 25% chance of a rate cut, the market may look to resolve this pricing one way or the other on today's jobs print.

- The US jobs report is the primary for the US session, brought forward by one day from its usual release due to the July 4th market holidays on Friday. Markets expect the US to have added 106k jobs over the month, but downside risks pervade after ADP Employment Change missed expectations and the market whisper number continues to drift: now at +95k.

EGBS: Bund Futures Follow Gilts Higher, Remain Below Initial Resistance

Bund futures have followed Gilts higher this morning, looking through early Spanish/French supply and an upward revision to the Eurozone June services PMI. Futures are +26 ticks at 130.21 at typing, but remain below clustered resistance at 130.50 (yesterday’s high) and 130.53 (50-day EMA). Global markets are focused on this afternoon’s US labour market report (alongside a swathe of other macro data).

- German yields are 1.5-3bps lower today, with the belly outperforming. A reminder that a BBG benchmark roll yesterday mechanically added ~4bps to the 10-year yield, which is currently at 2.631%.

- 10-year EGB spreads to Bunds are within 1bp of yesterday’s closing levels.

- Spanish and French supply was digested smoothly, with low prices in excess of pre-auction mids across lines.

- Following upward revisions in France and Germany, the Eurozone-wide June services PMI was revised to 50.5 (vs 50.0 flash, 49.7 prior). The composite PMI was 50.6 (vs 50.2 flash and prior), consistent with positive but weak growth.

GILTS: Most of Early Rally Holds After Starmer Supports Reeves

Gilts are off highs but have rallied after PM Starmer deployed firmer support for Chancellor Reeves overnight.

- Gilt futures ~100 ticks above yesterday’s low, last 92.60, ~20 ticks away from paring all the losses that were linked to questions surrounding the future of Chancellor Reeves.

- Bulls forced a brief move back above the 20-day EMA (92.71) this morning, as they look to regain technical control.

- Yields are 4-10bp lower across the curve, flattening.

- Cash 10s and 30s erased essentially all of the sell off that was driven by speculation surrounding Reeves’ future, before yields ticked away from session lows, aided by a firmer-than-expected final services PMI/

- The 10-Year gilt/Bund spread is ~5bp tighter on the day, last ~189.5bp after trading in a 183-196bp range yesterday. Yesterday’s widening probably cleared out some spread tightener positioning, which some sell-side desks believe had become crowded.

- SONIA futures flat to +7.0, strip flatter, aided by long end cues.

- BoE-dated OIS has returned to pricing ~55bp of cuts through year-end, with markets unable to push pricing of cuts meaningfully beyond that point in recent weeks.

- Offshore cues should dominate for the remainder of the day, with U.S. NFP & ISM services data due.

EQUITIES: Short-Term Trend Signals in Eurostoxx 50 Futures Remain Bearish

Short-term trend signals in Eurostoxx 50 futures remain bearish, however, the recovery from the Jun 23 low appears to be a reversal and the contract is holding on to its most recent gains. Price has traded through the 20- and 50-day EMAs. A clear break of both EMAs would strengthen a reversal theme. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of 5194.00, the Jun 23 low, reinstates a bearish theme. The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract continues to appreciate. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirms a resumption of the uptrend that started Apr 7. Note too that a key resistance and a bull trigger at 6277.50, the Feb 21 high, has been pierced. Clearance of this hurdle would open the 6300.00 handle. Key support is at the 50-day EMA - at 5987.53.

- Japan's NIKKEI closed higher by 23.42 pts or +0.06% at 39785.9 and the TOPIX ended 2.95 pts higher or +0.1% at 2828.99.

- Elsewhere, in China the SHANGHAI closed higher by 6.359 pts or +0.18% at 3461.151 and the HANG SENG ended 151.47 pts lower or -0.63% at 24069.94.

- Across Europe, Germany's DAX trades higher by 55.94 pts or +0.24% at 23846.24, FTSE 100 higher by 41.45 pts or +0.47% at 8815.95, CAC 40 up 5.3 pts or +0.07% at 7743.72 and Euro Stoxx 50 down 0.3 pts or -0.01% at 5318.42.

- Dow Jones mini up 17 pts or +0.04% at 44790, S&P 500 mini up 3.25 pts or +0.05% at 6278.25, NASDAQ mini up 26.75 pts or +0.12% at 22870.25.

Time: 10:00 BST

COMMODITIES: Gold Recovery Highlights Possible False Break of Trendline

WTI futures maintain a softer tone following the reversal from the Jun 23 high. Wednesday’s gains - for now - appear corrective. Support to watch is the 50-day EMA, at $64.75. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high. Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low. A clear break of both trend tools would signal scope for a deeper correction - this would expose $3245.5, the May 29 low. The metal has recovered from Monday’s low and for now, this highlights a possible false trendline break. Stronger gains would refocus attention $3451.3, Jun 16 high. The bear trigger is $3248.7, the Jun 30 low.

- WTI Crude down $0.45 or -0.67% at $66.98

- Natural Gas up $0.05 or +1.49% at $3.542

- Gold spot down $2.3 or -0.07% at $3355.67

- Copper up $0.1 or +0.02% at $520

- Silver up $0.49 or +1.34% at $37.0395

- Platinum down $14.06 or -0.99% at $1408.38

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 03/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 03/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 03/07/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/07/2025 | 1230/0830 | *** | Employment Report | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/07/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/07/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1400/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 03/07/2025 | 1400/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 03/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 03/07/2025 | 1500/1100 | Atlanta Fed's Raphael Bostic | ||

| 03/07/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 04/07/2025 | 2330/0830 | ** | Household spending | |

| 04/07/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/07/2025 | 0645/0845 | * | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Unemployment | |

| 04/07/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/07/2025 | 0800/1000 | * | Retail Sales | |

| 04/07/2025 | 0800/1000 | ECB Elderson Speech At IMF OEDNE/World Bank Meeting | ||

| 04/07/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/07/2025 | 0900/1100 | ** | PPI | |

| 04/07/2025 | 1500/1600 | BOE Taylor Speech On Natural Interest Rate |