MNI US OPEN - Oil Reverses Gains on Lack of Iranian Response

EXECUTIVE SUMMARY

- OIL REVERSES SHARP ASIA GAINS ON LACK OF IRANIAN RESPONSE

- ISRAEL LAUNCHES FRESH ATTACK ON FORDOW NUCLEAR SITE

- TRUMP’S ‘BIG, BEAUTIFUL BILL’ GETS SLIMMED DOWN IN SENATE

- STRONGER GERMAN MANUFACTURING DEMAND MASKS FALL IN HIRING

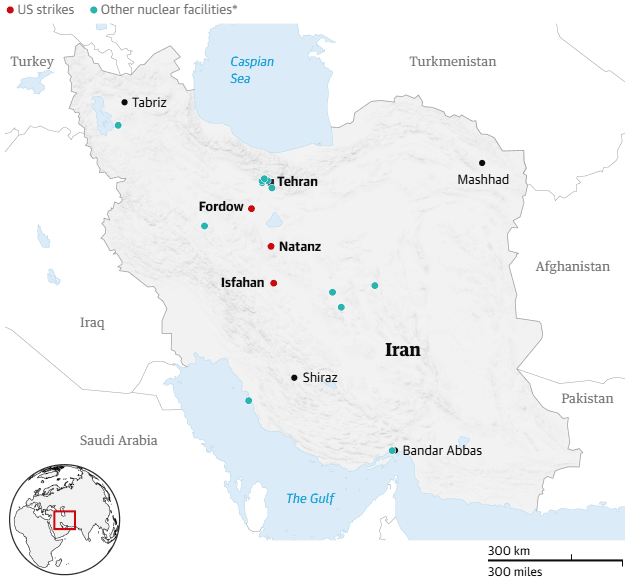

Figure 1: US strikes on Iran

Source: Guardian graphic via International Institute for Strategic Studies (IISS), The Nuclear Threat Initiative. Note: *Nuclear facilities include industrial and research sites

NEWS

OIL (MNI): Oil Reverses Sharp Asia Gains on Lack of Iranian Response

Crude oil benchmarks reverse the bulk of the near 6% early-APAC gains. The lack of immediate response from Iran/ongoing flow through the Strait of Hormuz at this stage allow overnight pricing of immediate supply disruptions to be unwound. The Iranian parliament has endorsed the closure of the Strait of Hormuz, although the final decision on that matter rests with Iran's Supreme National Security Council & the Ayatollah. Our commodities team notes that there are no signs that Iran is ready to follow through on threats to block oil shipments.

MIDEAST (BBG): Israel Launches Fresh Attack on Fordow Nuclear Site: Tasnim

Israel launched an attack on Iran’s Fordow nuclear site, semi-official Tasnim news agency reports, citing a spokesman for the crisis department of Qom province. The attack was carried out “moments ago” in the province, where the nuclear facility is located. Fordow was one of three nuclear sites that the US struck over the weekend.

MIDEAST (POLITICO): Iran’s Foreign Minister Heading to Russia to Meet With Putin After US Strikes

Iran’s Foreign Minister Abbas Araghchi on Sunday announced he will travel to Moscow in the coming hours for urgent talks with Russian President Vladimir Putin, shortly after the United States launched airstrikes against three Iranian nuclear sites. Araghchi emphasized the “strategic partnership” between Iran and Russia. “We always consult with each other and coordinate our positions,” he told reporters in Istanbul, according to media reports. Russia is a close ally of Iran. Tehran supplied Moscow with military drones to strike Ukraine and, in return, has received help with its civilian nuclear program. The Kremlin has also maintained warm relations with Israel.

US (WSJ): Trump’s ‘Big, Beautiful Bill’ Gets Slimmed Down in Senate

President Trump’s “big, beautiful bill” is getting smaller just as Republicans head into a crucial week, after the Senate’s rules arbiter decided several controversial provisions don’t qualify for the special procedure the GOP is using to bypass Democratic opposition. The tax-and-spending megabill centers on extending Trump’s 2017 tax cuts, delivering on the spirit of his campaign promises to eliminate taxes on tips and overtime, and providing big lump sums of money for border security and defense. Those new costs are partially offset by spending cuts, in particular to Medicaid.

EU/CANADA (BBG): EU and Canada Prepare to Sign Security Pact Ahead of NATO Summit

The European Union and Canada are expected to sign a security and defense partnership on Monday at a summit that will kick off a range of discussions about how they can work closer together. Canadian Prime Minister Mark Carney landed in Brussels late Sunday for the meetings, and one of his government’s objectives is to see Canada participate in SAFE, the EU’s €150 billion ($173 billion) joint military procurement loan fund.

SPAIN (BBG): Spain Wins Exemption From NATO’s 5% Defense Spending Goal

Spain obtained an exemption from NATO’s ambitious defense spending target of 5% of GDP after several days of diplomatic wrangling that drew scorn from Donald Trump, right before leaders of the military alliance gather on Tuesday. “We fully respect the legitimate desire of other countries of increasing their defense investment but we won’t do it,” Spanish Prime Minister Pedro Sanchez said on Sunday afternoon. The country can get defense expenditure up to 2.1%, “nothing more, nothing less.”

UK (FT): Energy Prices Cut for Business as Part of UK Industrial Strategy

Sir Keir Starmer will invest £2bn over four years to cut energy prices by up to a quarter for thousands of businesses, as part of his long-awaited industrial strategy. A new “British Industrial Competitiveness Scheme” would reduce electricity costs for more than 7,000 energy-intensive businesses in sectors including automotive, aerospace and chemicals, the government said. Details of the businesses eligible for the scheme — which will exempt companies from paying various green levies and will come into force in 2027 — will be determined after a consultation.

JAPAN (MNI): LDP's Tokyo Assembly Election Debacle Bodes Ill for Upper House Race

The ruling Liberal Democratic Party's (LDP's) dismal showing in yesterday's Tokyo Metropolitan Assembly Election is seen as a bad prognostic for the party ahead of the looming upper house election. The LDP secured a record-low number of 22 seats in the 127-member Tokyo legislature, falling behind Tomin First no Kail, a regional party founded by Governor Yuriko Koike, which won 32 seats. Three of these 22 assembly members were candidates who were not officially endorsed by the LDP due to their

links to the political funding scandal. The results are a warning sign for the LDP ahead of the July 20 poll in which voters will elect half of the 248-member House of Councillors, the upper house of the National Diet, for a six-year term.

JAPAN (MNI): PM to Skip NATO Summit Amid IP-4 Sidelining & LDP Election Woes

In the latest blow to the already ill-fated NATO summit taking place on 24-25 June, the Japanese Foreign Ministry has confirmed earlier headlines reporting that PM Shigeru Ishiba may not attend the summit. The expected cancellation of the IP-4 (Indo-Pacific Four: Australia, Japan, South Korea and New Zealand) meeting with US President Donald Trump has already seen South Korean President Moon Jae-in and Australian PM Anthony Albanese pull out of the event. Japan's Foreign Minister Takeshi Iwaya will instead represent Tokyo at the summit.

BOJ (MNI INTERVIEW): Jan Hike Likely, Dec Not Ruled Out - Ex BOJ

MNI discusses the BOJ's hiking strategy with a former chief economist. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI): China Should Improve Consumption Subsidy

MNI (Beijing) China must enhance the targeting of consumer subsidies, strengthen support for exporters, and step up efforts to stabilise the property market in the second half of the year, according to a report by the China Macroeconomy Forum. Authorities should introduce more targeted subsidies for students with high consumption willingness as well as urban retirees with strong spending power, and expand subsidies to the service sector, the report said, noting that the CNY330 billion consumer goods trade-in scheme is expected to drive 1.5-2% of retail sales growth this year.

DATA

EUROZONE DATA (MNI): Convergence in Services Activity

- EUROZONE FLASH JUNE MANUF PMI 49.4 (49.8 F'CAST, 49.4 MAY)

The Eurozone flash June services PMI ended up in line with consensus at 50.0 (vs 49.7 prior), somewhat surprising given the German reading was 1.6 points stronger-than-expected and France was only 0.3 points below consensus. This suggests that although the Eurozone ex-Germany and France continues to outperform the two largest economies, momentum in activity levels appears to be converging. We estimate the Germany/France services PMI at 49.1 (vs 47.9 prior), with the ex-Germany/France measure falling to 51.5 (vs 52.8 prior).

GERMANY DATA (MNI): Stronger Manufacturing Demand Masks Fall in Hiring

- GERMANY JUNE FLASH MANUF PMI 49.0 (49.0 F'CAST, 48.3 MAY)

The German flash June services PMI more than unwound May's fall, exceeding consensus at 49.4 (vs 47.8 cons, 47.1 in May, 49.0 in April). The manufacturing PMI was in line with expectations at 49.0, up from 48.3 prior for the strongest reading in 34 months. That helped the composite reading return to (slightly) expansionary territory at 50.4 (vs 48.5 prior). Details of the report highlight improved demand amongst manufacturers, but this did not stop overall manufacturing employment from falling. Meanwhile,

services business confidence dipped in June. As such, the details of the report still display some signs of softness for Europe's largest economy, despite the stronger-than-expected headline readings.

FRANCE DATA (MNI): Bleak Flash PMI Details, But 12m Ahead Confidence Rises

- FRANCE FLASH JUNE MANUF PMI 47.8 (49.8 F'CAST, 49.8 MAY)

Both the flash French manufacturing and services PMIs were weaker than expected in June, with manufacturing index falling two points to 47.8 (vs 49.8 cons) - the lowest since February - and services printing at 48.7 (vs 49.1 cons, 48.9 prior). A reminder that the INSEE June manufacturing survey (released last week) was quite soft, so the weaker-than-expected PMI print isn't too much of a surprise. The details of the flash report are bleak, though 12-month ahead confidence surprisingly rose to the highest since October.

UK DATA (MNI): Dovish Undertones to Report Despite Manufacturing Beat

- UK JUNE FLASH MANUFACTURING PMI 47.7 (46.9 F'CAST, 46.4 MAY)

The UK PMI was in line with expectations for services at 51.3 but the manufacturing PMI was a little higher than expected at 47.7 (46.9 exp, 46.4 prior). However, the underlying conditions still had a dovish undertone for future monetary policy with both input prices and prices charged increasing at slower paces while private sector employment decreased at a faster pace than in May.

AUSTRALIA DATA (MNI): Pickup in June Activity But Manufacturing Environment Difficult

The preliminary June S&P Global PMIs showed that services activity in Australia ended Q2 on a more positive note with the index up to 51.3 from 50.6. Manufacturing was stable at 51.0 as the global market becomes more challenging, which left the composite up to 51.2 from 50.5, the highest since March. The Q2 average composite PMI was 50.9 down slightly from Q1's 51.1, signalling that growth was little changed and remained positive but lacklustre.

FOREX: USD Rallies Despite More Benign Market Backdrop

- Despite a more benign-than-expected market reaction to the US strikes on Iran - particularly in the oil market - the USD is firmer against all others in G10 headed through to the crossover, staying favoured against all others amid higher geopolitical tensions. There remain several questions over the efficacy of strikes on Iran's nuclear sites over the weekend, but there are few signs of material retaliation from Tehran, despite full-throated threats and even warnings of the closure of the Strait of Hormuz in the hours after the attacks.

- For now, Trump's goals remain a return of Tehran to the negotiating table, or regime change away from the hardline approach of the current government.

- This price actions plays into the signals of a short-term base of the USD here - and a possible buy-on-dips pattern forming. We noted last week the importance of the USD Index showing above the downtrendline that's defined dollar weakness across Trump's term so far - and noted that even de-escalation headlines were proving insufficient to trigger any material weakness in the USD. This leaves 100.481 - 100.569 area as the next upside target and plausible resistance for a short-term bounce.

- With oil prices fully reversing their initial surge to start the week, and equity benchmarks remaining resilient to geopolitical developments, Japanese Yen weakness is continuing to standout. The break of a confluence of technical parameters has been assisting the move higher, namely the breach of the downtrend (drawn from the January highs) and the clean break of the May 29 high, cancelling the recent bearish theme.

- Preliminary June PMI data from the US is expected to confirm a slowing manufacturing sector but resilience from services, with existing home sales set to follow. Central bank speak Monday is headlined by ECB's Lagarde, who addresses EU parliament at 1400BST/0900ET, while Fed's Bowman speaks on monetary policy shortly afterward. ECB's Nagel, Fed's Goolsbee, Williams and Kugler also make appearances.

EGBS: Bund Futures Remain Sensitive to Mid-East Developments

Bund futures are -7 ticks at 130.86, with markets still sensitive to developments in the Middle East after the US attacked Iranian missile sites over the weekend. Israeli attacks on Tehran and the Fordow nuclear facility have continued today, but our commodities team notes that there are no signs that Iran is ready to carry out threats to block oil shipments.

- Bunds remain in consolidation mode and continue to trade below the Jun 13 high. For now, the latest move down appears to be a correction. Key short-term support to watch lies at 130.12, the Jun 5 low.

- German yields are 1-2bps higher, with the 5-year tenor underperforming.

- 10-year EGB spreads to Bunds are within 0.5bps of Friday’s closing levels (with the exception of GGBs, +1.5bps wider). Early narrowing has unwound with European equity futures now off session highs.

- The EU sold 5/10/25-year EU-bonds this morning, with Belgium also scheduled to sell OLOs at 1100BST. Slovenia announced a mandate for a 10-year benchmark.

- The Eurozone flash June services PMI ended up in line with consensus at 50.0 (vs 49.7 prior), somewhat surprising given the German reading was 1.6 points stronger-than-expected and France was only 0.3 points below consensus. This suggests that although the Eurozone ex-Germany and France continues to outperform the two largest economies, momentum in activity levels appears to be converging.

- ECB President Lagarde speaks at EU Parliament at 1400BST, with Nagel speaking on regulation at 1600BST.

- Elsewhere, there is some attention on the outcome of today’s French pension reform negotiations and tomorrow’s German budget/issuance plan.

GILTS: Off Lows as Geopolitics Continues to Dominate

Gilts have pared early losses, with questions surrounding the location of some Iranian uranium and hardline rhetoric out of the country allowing the recovery from session lows to extend in recent trade.

- Crude oil briefly traded ~$5 off overnight highs as it moved into negative territory but has recovered ~$1 from session lows.

- Futures back to ~92.70, little changed on the day, after printing as low as 92.25.

- Initial support at the 20-day EMA (92.34) was breached but the June 16 low (92.23) held.

- Bulls hold the upper hand from a technical perspective, but the break of the 20-day EMA presents heightened risk to that outlook.

- Yields are flat to -1bp on the day, 3-4bp off session highs.

- Major curves essentially unchanged on the day, with recent ranges in benchmark yields intact.

- Macro/geopolitical risk dominates local matters, with no meaningful impact from the inline to slightly firmer-than-expected flash PMIs.

- BoE-dated OIS showing 47bp of cuts through Dec, with the next 25bp move almost fully discounted through the September meeting. Pricing for ’25 meetings is ~1bp more hawkish on the day.

- BoE Governor Bailey appears at the Insurance Chairs Dinner this evening.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.027 | -19.0 |

Sep-25 | 3.970 | -24.7 |

Nov-25 | 3.816 | -40.1 |

Dec-25 | 3.745 | -47.2 |

Feb-26 | 3.637 | -58.0 |

Mar-26 | 3.612 | -60.5 |

EQUITIES: Short-Term Bear Cycle in Eurostoxx 50 Futures Still in Play

A short-term bear cycle in Eurostoxx 50 futures remains intact and the contract has traded to a fresh cycle low today. Recent weakness has resulted in a breach of the 50-day EMA. Price has also traded through 5279.00, May 23 low. The clear break of both support points signals a S/T top and scope for a deeper retracement. Sights are on 5182.00, the May 2 low and 5100.94, a Fibonacci retracement. Initial resistance is 5343.47, the 20-day EMA. The trend condition in S&P E-Minis is unchanged, it remains bullish. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6007.80, the 20-day EMA. A clear breach of this average would suggest potential for a deeper retracement and expose the 50-day EMA, at 5906.79. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

- Japan's NIKKEI closed lower by 49.14 pts or -0.13% at 38354.09 and the TOPIX ended 10.08 pts lower or -0.36% at 2761.18.

- Elsewhere, in China the SHANGHAI closed higher by 21.686 pts or +0.65% at 3381.582 and the HANG SENG ended 158.65 pts higher or +0.67% at 23689.13.

- Across Europe, Germany's DAX trades lower by 0.7 pts or 0% at 23348.23, FTSE 100 higher by 3.44 pts or +0.04% at 8778.08, CAC 40 down 1.39 pts or -0.02% at 7587.47 and Euro Stoxx 50 up 8.75 pts or +0.17% at 5241.86.

- Dow Jones mini up 51 pts or +0.12% at 42565, S&P 500 mini up 14.25 pts or +0.24% at 6032, NASDAQ mini up 61.25 pts or +0.28% at 21904.5.

Time: 10:00 BST

COMMODITIES: WTI Futures Hit Fresh Cycle High, Bull Cycle Remains Intact

A bull cycle in WTI futures remains intact and the contract has delivered a fresh cycle high today. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend remains in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted at $67.11, the Jun 13 low. A breach of this level would signal scope for a deeper retracement. A bullish theme in Gold remains intact and last week’s pullback is considered corrective. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has recently been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3282.7, the 50-day EMA.

- WTI Crude down $0.2 or -0.27% at $73.61

- Natural Gas up $0.02 or +0.62% at $3.871

- Gold spot down $6.07 or -0.18% at $3361.99

- Copper down $2.5 or -0.51% at $485.95

- Silver up $0.19 or +0.53% at $36.2127

- Platinum up $28.23 or +2.23% at $1296.87

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 23/06/2025 | - | BOE Bailey At Insurance Chairs Dinner | ||

| 23/06/2025 | 1300/1500 | ECB Lagarde At ECON Hearing | ||

| 23/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/06/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/06/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/06/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 23/06/2025 | 1720/1320 | Chicago Fed's Austan Goolsbee | ||

| 23/06/2025 | 1830/1430 | Fed Governor Adriana Kugler | ||

| 24/06/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/06/2025 | 0800/0900 | BOE Bailey At Gold Standard Conference | ||

| 24/06/2025 | 0845/1045 | 2025 Budget Press Conference | ||

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0930/1030 | BOE Green On CB Balance Sheet Mgmt | ||

| 24/06/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/06/2025 | 1115/1315 | ECB de Guindos At XLII APIE seminar | ||

| 24/06/2025 | 1230/0830 | *** | CPI | |

| 24/06/2025 | 1230/0830 | * | Current Account Balance | |

| 24/06/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 24/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 24/06/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/06/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/1500 | ECB Lagarde Accepts De Sanctis Award "Europa" | ||

| 24/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 24/06/2025 | 1335/1435 | BOE Ramsden At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1355/1555 | ECB Lane Keynote At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 24/06/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 24/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 24/06/2025 | 1400/1500 | BOE Bailey At Lords Econ Affairs Committee | ||

| 24/06/2025 | 1540/1640 | BOE Pill At Gold Standard Conference | ||

| 24/06/2025 | 1550/1650 | BOE Breeden At UK Finance Digital Innovation Summit | ||

| 24/06/2025 | 1630/1230 | New York Fed's John Williams | ||

| 24/06/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 24/06/2025 | 1805/1405 | Boston Fed's Susan Collins | ||

| 24/06/2025 | 2000/1600 | Fed Governor Michael Barr |