MNI US OPEN - Nvidia Earnings Ease Fears of AI Bubble Burst

EXECUTIVE SUMMARY

- NVIDIA’S UPBEAT FORECAST SOOTHES FEARS OF AI SPENDING BUBBLE

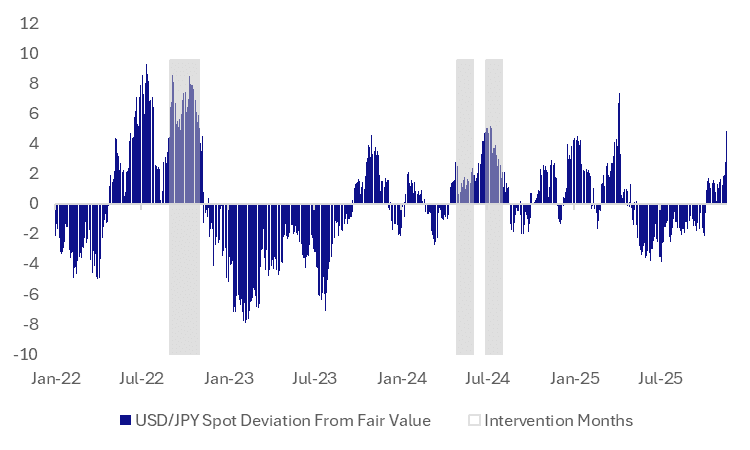

- JAPAN’S KIHARA SAYS HE SEES WORRYING ONE-WAY, SUDDEN YEN MOVES

- JAPAN IS SET TO UNVEIL $112 BILLION IN FRESH STIMULUS

- CHINA WEIGHS NEW PROPERTY STIMULUS PACKAGE AS CRISIS LINGERS

Figure 1: USD/JPY deviation from simple fair value (%) and intervention episodes

Source: Bloomberg Finance L.P., MNI

NEWS

US (BBG): Nvidia’s Upbeat Forecast Soothes Fears of AI Spending Bubble

Nvidia Corp. delivered a surprisingly strong revenue forecast and pushed back on the idea that the AI industry is in a bubble, easing concerns that had spread across the tech sector. The world’s most valuable company expects sales of about $65 billion in the January quarter — roughly $3 billion more than analysts predicted. Nvidia also said that a half-trillion-dollar revenue bonanza due in coming quarters may be even bigger than anticipated.

US (BBG): White House Asks Congress to Reject Bill Curbing Nvidia Exports

White House officials are urging members of Congress to reject a measure that would limit Nvidia Corp.’s ability to sell AI chips to China and other adversary nations, according to people familiar with the matter, dimming prospects for legislation opposed by the world’s most valuable company. The so-called GAIN AI Act would create a system that requires chipmakers to give Americans first dibs on AI chips that are controlled for export to China and other arms-embargoed countries — an “America first” framing designed to appeal to the Trump administration.

US/CANADA (BBG): Trump’s Canada Envoy Sees Trade Talks Resuming After Sudden Halt

The US ambassador in Ottawa said Canada and the US have a chance to reach an agreement to reduce tariffs despite last month’s diplomatic blowup when President Donald Trump angrily halted negotiations. Until about a month ago, the two countries had been making progress on a limited deal to address certain trade frictions, Ambassador Pete Hoekstra told a conference of manufacturers in Ottawa on Wednesday. The talks will resume, he predicted, though he’s not sure when.

EU/RUSSIA (MNI): Foreign Ministers Meet w/20th Sanctions Package on Agenda

EU foreign ministers are holding a Foreign Affairs Council meeting in Brussels, with the planned 20th package of sanctions on Russia one of the agenda items. Bloomberg News reports that Russia's 'shadow fleet' of oil tankers remains in the sights of the EU with regard to further sanctions. Ministers are "expected to explore stepping up engagements with countries that register the vessels in an effort to clamp down on these ships Russia uses to circumvent the bloc's sanctions..." The other major topic of debate regarding Ukraine will be continued efforts to find an acceptable funding package for Kyiv.

UK (FT): Rachel Reeves Under Pressure to Scale Back Budget Raid on Expensive Homes

Chancellor Rachel Reeves is facing last-minute pressure from Labour MPs in London and the south-east to scale back the scope of a “mansion tax” amid warnings that a possible £1.5mn threshold for the levy would be too low. Labour MPs have warned Reeves that a council tax surcharge on the most expensive homes could hit the party’s support, especially in the capital. They want the threshold to be set at a higher level, potentially at up to £2mn. People briefed on Budget preparations said the details of the high-end property charge were still “live”, with only a week until Reeves presents her financial package on November 26.

UK (FT): UK Investors Pull Out of London Stock Market at Record Pace

Domestic investors have fled the UK stock market at a record rate this year, missing out on a storming rally in which London’s equity market has outpaced both US and European bourses. UK investors have pulled about £26bn from London-listed equities so far in 2025, according to EPFR data, the highest level on record for a calendar year, as measured by outflows from funds investing in the UK.

JAPAN (BBG): Japan Is Set to Unveil $112 Billion in Fresh Stimulus

Japanese Prime Minister Sanae Takaichi is set to unveil an economic package funded by an extra budget about 27% bigger than what was pledged in her predecessor’s spending plan a year ago, underscoring her commitment to an expansive fiscal policy. The package will incorporate ¥17.7 trillion ($112 billion) of spending from the general account, according to documents seen by Bloomberg Thursday. That tops the ¥13.9 trillion former Primer Minister Shigeru Ishiba unveiled last year, and is set to effectively be the size of the upcoming extra budget.

JAPAN (BBG): Japan’s Kihara Says He Sees Worrying One-Way, Sudden Yen Moves

The yen is experiencing sudden, one-way movements that are concerning and which require close monitoring, Japan’s chief cabinet secretary said. Excessive fluctuations and disorderly movements in exchange rates must be monitored with vigilance, Minoru Kihara said during a press conference on Thursday. “We are concerned about the recent one-way and sudden movements in the foreign exchange market,” Kihara said. “It’s important for exchange rates to remain stable, reflecting fundamentals.”

BOJ (MNI): BOJ Committed to Stable Rates, Yields - Koeda

Bank of Japan board member Junko Koeda said Thursday the Bank will implement necessary measures, including increasing bond-buying operations, to stabilise interest rates if long-term yields rise sharply. The BOJ’s stance toward addressing a sudden spike in long-term rates remains unchanged, Koeda told reporters in Niigata City. The 10-year JGB yield climbed to 1.835% this week, the highest level since June 2008. Koeda, who joined the board in March, said the BOJ continues to monitor the impact of dollar/yen movements on import prices closely.

JAPAN/CHINA (MNI): Japan PM Comments Have Hurt Trade With China - MOFCOM

MNI (Beijing) Remarks regarding Taiwan by Japan's Prime Minister Sanae Takaichi has had a serious negative impact on economic and trade exchanges between Beijing and Tokyo, He Yongqian, spokesperson for the Ministry of Commerce said on Thursday.

He said China is urging Japan to retract its comments, and help create a sound environment for bilateral economic and trade cooperation.

EU/CHINA (MNI EXCLUSIVE): Rare Earths Deadlock as EU Elevates China Economic Risk

EU sources and Chinese policy advisors sketch out the prospects for EU-China trade agreements. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (BBG): China Weighs New Property Stimulus Package as Crisis Lingers

China is considering new measures to turn around its struggling property market, as concerns mount that a further weakening of the sector will threaten to destabilize its financial system, according to people familiar with the matter. Policymakers including the housing ministry are considering a slew of options, such as providing new homebuyers mortgage subsidies for the first time nationwide, said the people, asking not to be identified discussing a private matter. Other measures being floated include raising income tax rebates for mortgage borrowers and lowering home transaction costs, one of the people said.

CHINA (MNI): Nov LPR Remains Unchanged

MNI (Beijing) China’s Loan Prime Rate was left unchanged on Thursday, as expected, with the central bank maintaining its stance amid ongoing pressure on banks’ interest margins and confidence that the 5% annual GDP growth target remains within reach. The People’s Bank of China said on its website that the one-year LPR stayed at 3.0% and the five-year-and-above rate at 3.5%. Both were cut by 10bp in May after the PBOC lowered its 7-day reverse repo rate — the benchmark policy rate — by 10bp to 1.4% on May 8, followed by a 50bp reduction to the reserve requirement ratio on May 15.

RUSSIA (MNI): Kremlin Offers No Response to Claims on 28-Point Ukraine Peace Plan

Kremlin spox Dmitry Peskov, speaking to reporters, says that Russia has "nothing new to say in addition to what was said at the Putin-Trump summit in Alaska". Comes in the aftermath of Axios' report earlier in the week claiming that the US and Russia were working on a 28-point peace plan for Ukraine that effectively removes Kyiv, as well as Ukraine's European allies, from the decision-making process. Asked whether President Vladimir Putin has been briefed on the plan, Peskov says he has nothing to add to the matter.

DATA

GERMANY DATA (MNI): Unusual Drop In Non-durable Goods in October PPI

- GERMANY OCT PPI +0.1% M/M, -1.8% Y/Y

The drop in non-durable goods was the most striking part of the softer-than-expected October PPI. This subcomponent is worth monitoring next month if this was only a one-off or is starting to become more persistent. Non-durable goods fell from 3.2% Y/Y to 2.3% Y/Y in October, driven by a 0.7% M/M decline in the (non seasonally-adjusted) price index. The M/M reading was the lowest since May 2020 and the second lowest since November 2008. Looking at a category split, less expensive food and animal feed as well as coal may have put downside pressure here.

FOREX: USD Index Consolidating Close to Recovery Highs

- Broad strength for the greenback on Wednesday prompted an impressive lurch higher for the DXY, which has traded to within four pips of the recovery highs overnight. Safe haven dynamics were behind much of the move during yesterday’s session, however, gains were exacerbated by confirmation that the Fed will not receive any additional jobs reports before the December meeting.

- On data fog grounds, front-end rates now price a smaller chance of a December Fed cut (around 35%), cementing the bullish short-term theme for the greenback.

- Uncertainty over a Fed cut combines within uncertainty over a BOJ hike in December, continuing to drive the USDJPY rally overnight. The spike to 157.78 had additional tailwinds contributing, that being the ongoing fiscal concerns and associated pressure on JGBs as well as global technology stocks advancing after Nvidia reported better than expected chip sales.

- USDJPY has pulled back 60 pips or so, with some citing the moderate hawkish tilt to BOJ Koeda’s remarks overnight, however, this is more likely some profit taking given the 2% surge this week, and the upcoming US data.

- For NZDUSD, spot has stabilised back above 0.5600 today after falling over 1% on Wednesday to the lowest level since April. Despite the stabilisation, we remain at very depressed levels, and the bearish trend remains firmly entrenched. Support appears scant until the year’s lows at 0.5486.

- GBPUSD support was found around 1.3040 overnight and the pair is currently pushing fresh session highs around 1.3080. Yesterday’s sharp sell-off reinforces a bearish theme and highlights the fact that gains since Nov 4 have been corrective. A move through 1.3010, the Nov 4 / 5 low, would confirm the next phase lower, increasing in significance ahead of next week’s budget.

- September US payrolls will be the main event of the day, while BoE's Dhingra and Mann are scheduled to speak alongside Fed's Hammack, Barr, Cook, Goolsbee, Miran, and Paulson.

EGBS: 10-Year Bund Yields Push to Fresh Multi-Week High

10-year Bund yields trade at a fresh multi-week high of 2.72%, extending the upward trend that began in mid-October. The 2.75% level presents the next area of interest on the topside, but a push towards 2.80% may require a catalyst such as Germany’s 2026 issuance plan. We’ll follow up with more details on Germany’s monthly fiscal update later today.

- The German curve is marginally steeper, with yields up to 1bp higher across the curve. Upward pressure since yesterday afternoon looks to be a function of the recovery in risk assets (prior to and following Nvidia’s earnings) and a cautious set of FOMC minutes.

- Bund futures are -11 ticks at 128.56, albeit off lows of 128.48. Support remains unchanged at 128.41.

- 10-year EGB spreads to Bunds are up to 1bp narrower, with PGBs underperforming a little. Details of Greece’s 2026 budget reaffirmed well-documented fiscal resilience, while French and Spanish auctions were digested smoothly.

- ECB Governing Council member Makhlouf suggested the bar to another rate change is high, seemingly aligning with the median Governing Council member’s view.

- Global focus remains on today’s US labour market data (payrolls and IJC at 1330GMT).

GILTS: Swap Spreads Hold Lower, 80bp Limits 2s10s Steepening

Gilts hold off early session lows, with global benchmark equities edging away from highs that followed Nvidia earnings.

- No lasting spill over from the hawkish Fed meeting minutes and weakness in JGBs.

- Futures last little changed at 91.71 (91.51-85 range)

- Initial support and resistance of note located at 91.12 & 91.94.

- The recent bear cycle deepened yesterday, overriding the bullish technical conditions that were in place.

- Yields -/+0.5bp across the curve, light twist flattening.

- 10- & 30-Year swap spreads trade within 1bp of yesterday’s lows. Questions surrounding the future of PM Starmer’s position as Labour leader have increased political/fiscal risk premium in gilts ahead of next week’s Budget.

- The recent steepening on the 2s10s curve has stalled at 80bp, with the round number protecting the year-to-date closing high (81.63bp).

- Gilt/Bund spread 188bp (-1bp) after a failed break above 190bp yesterday.

- This morning’s I/L gilt supply passed smoothly.

- BoE-dated OIS pricing ~21bp of easing for December after yesterday’s CPI data lowered the bar for a cut at that event.

- SONIA-implied terminal rate pricing Implied ~3.40%, holding comfortably within the multi week ~3.30-3.45% range.

- Lower tier CBI data and comments from BoE’s Dhingra (dove) & Mann (hawk) are due today.

- A reminder that we do not expect much market vol. to stem from any non-Bailey BoE comments in the lead up to the December decision, given the entrenched views of the other MPC members (Bailey is deemed the key swing voter).

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.762 | -20.7 |

Feb-26 | 3.695 | -27.4 |

Mar-26 | 3.617 | -35.3 |

Apr-26 | 3.522 | -44.7 |

Jun-26 | 3.478 | -49.1 |

Jul-26 | 3.420 | -55.0 |

Sep-26 | 3.405 | -56.4 |

EQUITIES: Eurostoxx 50 Futures Recovery Places Contract Back Above 50-Day EMA

A medium-term bull trend in Eurostoxx 50 futures remains intact, however, recent weakness highlights a stronger corrective cycle. The contract has breached two key support points; 5601.75, the 50-day EMA, and 5615.50, the base of a bull channel drawn from the Aug 1 low. The breach signals scope for a deeper pullback and opens 5503.00, a Fibonacci retracement. Initial firm resistance to watch is 5652.52, the 20-day EMA. S&P E-Minis maintain a softer S/T tone - for now - despite the recovery from Tuesday’s low. The recent breach of 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the current corrective cycle. Note that price has also traded through support at the 50-day EMA. A resumption of weakness would open 6540.25, the Oct 10 low and the next key support. Initial firm resistance to watch is 6767.81, the 20-day EMA.

- Japan's NIKKEI closed higher by 1286.24 pts or +2.65% at 49823.94 and the TOPIX ended 53.99 pts higher or +1.66% at 3299.57.

- Elsewhere, in China the SHANGHAI closed lower by 15.691 pts or -0.4% at 3931.051 and the HANG SENG ended 4.92 pts higher or +0.02% at 25835.57.

- Across Europe, Germany's DAX trades higher by 196.37 pts or +0.85% at 23358.91, FTSE 100 higher by 57.21 pts or +0.6% at 9564.24, CAC 40 up 59.7 pts or +0.75% at 8012.65 and Euro Stoxx 50 up 49.41 pts or +0.89% at 5591.15.

- Dow Jones mini up 185 pts or +0.4% at 46395, S&P 500 mini up 66.75 pts or +1% at 6728.5, NASDAQ mini up 338.5 pts or +1.37% at 25060.25.

Time: 10:00 GMT

COMMODITIES: WTI Futures Remain Contained Within The Month's Tight Range

WTI futures are trading in a range. A sell-off on Nov 12 strengthens a bearish theme. A resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction. The bearish phase in Gold between Oct 20 and 28 appears to have been a correction and has allowed a recent overbought condition to unwind. The recovery since Oct 28 suggests that correction is over. Key support to watch lies at the 50-day EMA, at $3943.0. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

- WTI Crude up $0.48 or +0.81% at $59.92

- Natural Gas down $0 or -0.07% at $4.549

- Gold spot down $11.71 or -0.29% at $4066.72

- Copper down $1 or -0.2% at $508.7

- Silver down $0.4 or -0.79% at $50.9742

- Platinum down $0.23 or -0.01% at $1547.23

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 20/11/2025 | 1000/1100 | ** | EZ Construction Output | |

| 20/11/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 20/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 20/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 20/11/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1345/0845 | Cleveland Fed's Beth Hammack | ||

| 20/11/2025 | 1430/0930 | Fed Governor Michael Barr | ||

| 20/11/2025 | 1500/1000 | *** | NAR existing home sales | |

| 20/11/2025 | 1500/1000 | * | Services Revenues | |

| 20/11/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 20/11/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 20/11/2025 | 1600/1100 | Fed Governor Lisa Cook | ||

| 20/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 20/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 20/11/2025 | 1740/1240 | Chicago Fed's Austan Goolsbee | ||

| 20/11/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 20/11/2025 | 1830/1830 | BOE Dhingra Speech on Trade and Tariffs | ||

| 20/11/2025 | 2100/2100 | BOE Mann at IMF Statistical Forum | ||

| 21/11/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 20/11/2025 | 2315/1815 | Fed Governor Stephen Miran | ||

| 21/11/2025 | 2330/0830 | *** | CPI | |

| 20/11/2025 | 2345/1845 | Philly Fed's Anna Paulson | ||

| 21/11/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 21/11/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/11/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/11/2025 | 0700/0700 | *** | Retail Sales | |

| 21/11/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/11/2025 | 0800/0900 | ECB de Guindos Remarks/Q&A at Foro Gran Via | ||

| 21/11/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ECB Lagarde Speech at European Banking Congress | ||

| 21/11/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 21/11/2025 | 1000/1100 | Negotiated Wage Growth | ||

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson | ||

| 21/11/2025 | 1400/0900 | Dallas Fed's Lorie Logan | ||

| 21/11/2025 | 1400/0900 | Boston Fed's Susan Collins | ||

| 21/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/11/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 21/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 21/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 21/11/2025 | 1540/1540 | BOE Pill in Panel at Swiss National Bank | ||

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |

Note: US Government data releases are still TBD pending an official release schedule.