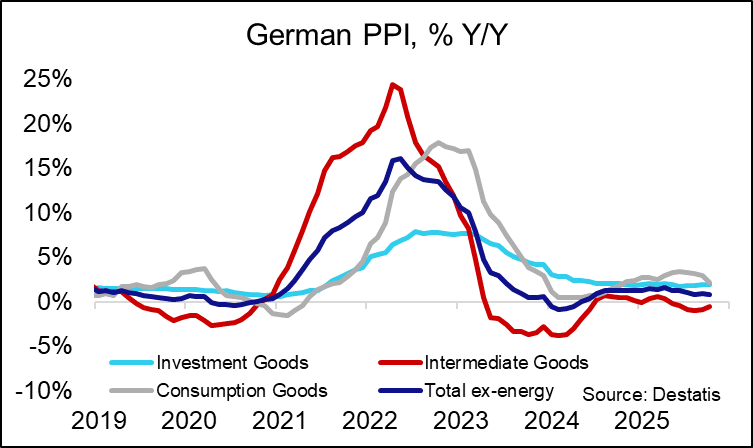

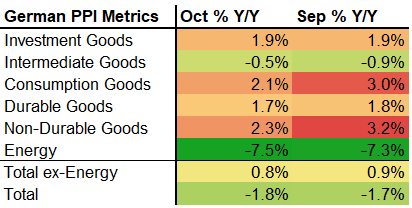

GERMAN DATA: Unusual Drop In Non-Durable Goods In October PPI

The drop in non-durable goods was the most striking part of the softer-than-expected October PPI. This subcomponent is worth monitoring next month if this was only a one-off or is starting to become more persistent.

- Non-durable goods fell from 3.2% Y/Y to 2.3% Y/Y in October, driven by a 0.7% M/M decline in the (non seasonally-adjusted) price index. The M/M reading was the lowest since May 2020 and the second lowest since November 2008. Looking at a category split, less expensive food and animal feed as well as coal may have put downside pressure here.

- Elsewhere, the consumption goods drop to 2.1% Y/Y from 3.0% also stood out but the category overlaps with non-durable goods to a decent extent, meaning its underlying drivers will likely have been the same.

- Intermediate goods countered that to some extent, accelerating to -0.5% Y/Y in October from -0.9%, but that was mostly driven by base effects as the monthly reading was a mere 0.1%. Investment goods (1.9% Oct vs 1.9% Sep), durable goods (1.7% Oct vs 1.8% Sep) and energy (-7.5% Oct vs -7.3%) all saw no unusual fluctuations, meanwhile.

- German manufacturing selling price expectations stand at 5.8 in October (5.5 Sep), below their long-term average.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: Estoxx Calendar Call Fly

SX5E (11th Nov) 5600c, (19th Dec) 5800c, (20th Mar) 6000c, bought as a calendar fly for 86 in 2k.

FOREX: EURCHF Extending Move South, Testing Key Cluster of Support

- The Swiss Franc has outperformed on Tuesday in a move potentially underpinned by a rotation of some investors out of the Yen following the parliament electing Takaichi as the new PM in Japan. Evidence of this is the strong move higher for CHFJPY, which closely matched the 191.17 all-time highs earlier in the session.

- Weakness for EURCHF today represents a sixth consecutive losing session. Lows today came within 4 pips of key medium-term support at 0.9206, clearance of which would place EURCHF at its lowest since the peg removal. Given the illiquidity back in 2015, support levels below 0.9200 are hard to pin-point, however, projection levels based on the Mar 14 - Apr 11 - Aug 18 price swing would place immediate attention on 0.9121 and 0.9017.

- JP Morgan wrote yesterday on Friday's EURCHF 0.9217 lows "with the VIX coming ‘off the boil’ [...] the bottom may be temporarily in the cross, but not the case in USDCHF. Until we see a close back above 0.7965, USDCHF looks vulnerable to a test of the mid-Sept. lows (0.7830)."

- BBVA meanwhile today repeat they "believe the recent appreciation of the CHF presents a good opportunity to enter short positions". They entered a EURCHF 0.9285 Oct-26 call last week (spot ref 0.9285).

- As a reminder, the inaugural edition of the SNB meeting minutes will be published this Thursday. In the minutes, alongside any view on FX valuations, we will look for more insight on whether Chairman Schlegel's non-mention of side effects of potential negative rates in his September opening remarks was intended to provide a policy signal.

JAPAN: New Fin Min: Not Unnatural To Push For Abenomics v.2025

Newly-appointed Finance Minister Satsuki Katayama has been speaking to the press. Says that she is committed to cooperation on tax within the governing coalition. The libertarian-federalist Japan Innovation Party (Ishin), which sits alongside PM-designate Sanae Takaichi's conservative Liberal Democratic Party (LDP) in gov't, laid out the elimination of sales tax on food for two years as one of its key demands to support Takaichi's gov't. Katayama expresses commitment to openly discussing the prospect of a reduction with Ishin.

- Katayama, who served as Minister for Regional Revitalization and Gender Equality from 2018-19, was previously part of the conservative-nationalist Seiwa Seisaku Kenkyukai faction led by the late PM Shinzo Abe. During her comments, Katayama says that it is "not unnatural to push forward a 2025 version of Abenomics". The 'three arrows' of aggressive monetary easing, fiscal stimulus, and structural reforms to enhance competitiveness defined Abe's second stretch in office. It is unclear at present how the 2025 version would differ from the initial formula.

- Katayama does not comment when asked on BoJ rate hikes, saying only that the yen should 'move stably, reflecting fundamentals'. On JGBs, says the Ministry of Finance, is 'effectively managing' Japan's debt 'with the highest level of diligence'.