MNI US OPEN - Japan's Komeito Party Wish to 'Reset' Coalition

EXECUTIVE SUMMARY

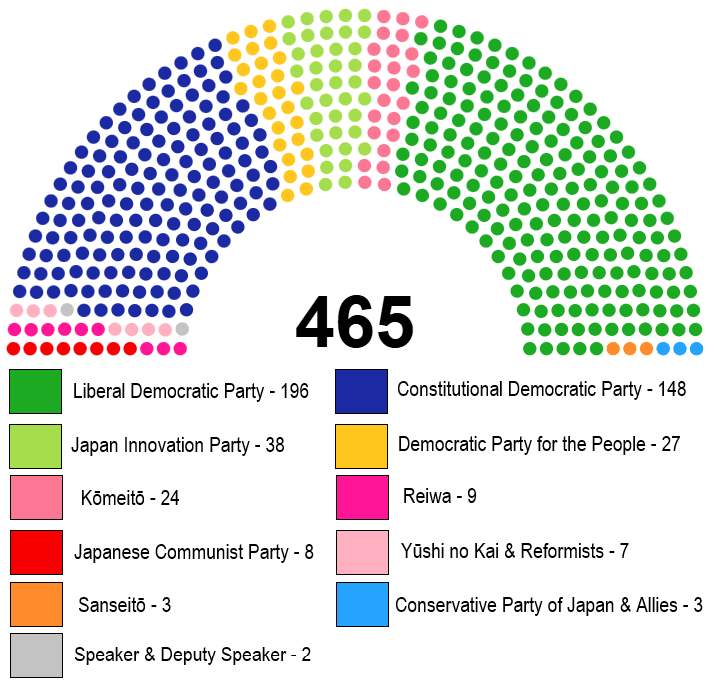

- KOMEITO WITHDRAWAL FROM GOVERNMENT PUTS LDP'S TAKAICHI IN PERILOUS POSITION

- ISRAELI CABINET BACKS GAZA DEAL, PAVING WAY FOR HOSTAGES RELEASE

- SENATE PASSES AI CHIP EXPORT LIMITS ON NVIDIA, AMD TO CHINA

- WHITE HOUSE DECLINES TO ENGAGE DEMOCRATS AS SHUTDOWN DRAGS INTO SECOND WEEK

Figure 1: Japan's House of Representatives, Seats

Source: MNI, shugiin.go.jp

NEWS

JAPAN (MNI): Komeito Withdrawal From Government Puts LDP's Takaichi in Perilous Position

Leader of the centrist social conservative Komeito party, Tetsuo Saito, announced that his party wishes to 'reset' the governing coalition with the conservative Liberal Democratic Party (LDP) and that its lawmakers would not vote for the new LDP president, Sanae Takaichi, to become PM in a confirmatory vote expected in the National Diet on 20 October. The PM is confirmed in a two-round system. If no single nominee receives an overall majority, then the top two candidates hold a run-off . If the two chambers elect different candidates, a joint committee is formed to try to reach agreement. If there is no agreement, or the upper House of Councillors does not submit a nomination within 10 days, the lower House of Representatives' candidate is elected as PM.

JAPAN (MNI): Opposition Leaders Talk Up Komeito Cooperation After Split w/LDP

Leader of the conservative populist Democratic Party for the People (DPFP), Yuichiro Tamaki, has posted on X regarding the centrist social conservative Komeito's withdrawal from the governing coalition with the conservative Liberal Democratic Party (LDP). Says "I view this as a manifestation of Komeito's extremely strong determination that the issue of money in politics must be brought to an end", referring to the LDP slush fund scandal that brought down the party's powerful faction system

and PM Fumio Kishida in 2024.

ISRAEL/MIDEAST (BBG): Israeli Cabinet Backs Gaza Deal, Paving Way for Hostages Release

Israel’s cabinet approved a deal that will see Hamas free all remaining hostages held in Gaza in exchange for around 2,000 prisoners, a major step toward ending a two-year war that’s killed tens of thousands of people and destabilized the wider Middle East. Israeli Prime Minister Benjamin Netanyahu’s coalition gave its approval overnight, around a day after negotiators for the warring sides reached an agreement in the Egyptian resort of Sharm El-Sheikh.

US/CHINA (BBG): China to Impose Special Port Fees on US Vessels From Oct. 14

China will impose special port service fees on US vessels starting Oct. 14, according to a statement from the Chinese Ministry of Transport. The move follows US’s decision to impose port service fees on Chinese vessels starting Oct. 14. China says US action severely disrupts bilateral shipping trade.

US/CHINA (BBG): Senate Passes AI Chip Export Limits on Nvidia, AMD to China

Advanced artificial intelligence chipmakers Nvidia Corp. and Advanced Micro Devices Inc. would have to ensure US companies get priority access to their products before China under legislation the Senate passed, a setback for the industry’s efforts to block the measure. The bipartisan legislation was easily approved in a vote late Thursday. It’s designed to bolster US competitiveness in cutting-edge industries and curb exports to China and other foreign adversaries, according to lead co-sponsor Senator Jim Banks, an Indiana Republican.

US/JAPAN (BBG): US, Japan to Press On With Trade Deal While New Leader Awaited

The US and Japan confirmed they will keep up efforts to implement their trade deal, as the Asian nation transitions to a new leader ahead of an expected visit to Tokyo by President Donald Trump. US Commerce Secretary Howard Lutnick and his negotiation counterpart Ryosei Akazawa talked by phone for about an hour and pledged that the two sides will continue to carry out the July deal, Japan’s Cabinet Secretariat said Friday.

US (WaPo): White House Declines to Engage Democrats as Shutdown Drags Into Second Week

In the eight days since the government shut down, President Donald Trump and his allies have engaged in a furious public campaign against Democrats, blaming them for the closure, trolling political opponents online and urging party leaders to accede to their demands. Behind the scenes, Trump and his aides have still not engaged with Democrats at all. The stance comes despite the potential political ramifications of the closure, which polling has shown the public blames more so on Republicans than Democrats.

US (WaPo): Senate Passes $925 Billion Defense Bill, Setting Up House Talks

The Senate on Thursday night approved its $925 billion version of the National Defense Authorization Act, the annual must-pass Pentagon policy blueprint, setting up what is expected to be a lengthy negotiation with the House to finalize the bill.

FRANCE (BBG): France Deficit Should Be Within 4.8% GDP in 2026, Villeroy Says

Bank of France Governor Francois Villeroy de Galhau said the next government must overcome political infighting and continue to target a significant reduction in the budget deficit next year. Outgoing Prime Minister Sebastien Lecornu opened the door to smaller cuts in 2026 as part of a deal on economic policy that he says will allow President Emmanuel Macron to appoint a new premier by Friday evening.

PERU (MNI): Limited Market Reaction Expected After President Boluarte Removed From Office

In a sudden move overnight, President Boluarte was ousted from office after Congress voted unanimously to approve an impeachment to remove her. The vote was triggered as parties that had previously aligned with her switched sides amid criticism over her failure to rein in soaring crime, culminating in a shooting at a concert in Lima this week. She has been replaced by the leader of Congress, José Jerí, who was sworn in as interim president earlier today to complete the rest of the current term that ends in July 2026. Jeri has said he will uphold the election timetable, which will see general elections held in April next year.

MALAYSIA (BBG): Anwar Aims to Cut Malaysia Deficit as Taxes Replace Oil Revenue

Malaysian Prime Minister Anwar Ibrahim plans to cut more subsidies and improve tax collection to narrow the budget deficit next year, as he grapples with lower petroleum-related revenue and dimming economic prospects. The government proposes 419.2 billion ringgit ($99.3 billion) of spending next year, according to a Finance Ministry report published just as Anwar begins to present the budget in parliament. That’s 1.7% higher than estimated state spending for 2025, which has been revised lower than last year’s official forecast.

THAILAND (BBG): Bank of Thailand Chief Sees Room to Ease After Surprise Hold

Governor Vitai Ratanakorn said the Bank of Thailand still has policy space to cut a benchmark interest rate that is already among the world’s lowest. “We’re ready to ease monetary policy further if needed to support economic growth and inflation,” Vitai said Friday, ten days into his job as central bank chief. The Bank of Thailand on Wednesday unexpectedly kept borrowing costs unchanged at 1.5%, partly to preserve limited policy space.

GLOBAL (BBG): Nobel Peace Prize Awarded to Venezuela’s Maria Corina Machado

Maria Corina Machado of Venezuela was awarded the Nobel Peace Prize for 2025. She receives the prize worth 11 million Swedish kronor ($1.2 million) “for her tireless work promoting democratic rights for the people of Venezuela and for her struggle to achieve a just and peaceful transition from dictatorship to democracy,” the Oslo-based Norwegian Nobel Committee said in a statement Friday.

DATA

UK DATA (MNI): KPMG-REC Report On Jobs Has Something for Everyone

The KPMG-REC Report on Jobs for September continued to show building slack in the labour market, albeit the pace of change is mixed across sub of the subcomponents. Starting salaries only rose "negligbly" in September "with the rate of growth the weakest seen since the current run of pay inflation began just over four-and-a-half years ago." Vacancies fell at a marginally slower pace than in August - but were still depressed. Permanent placements continued to fall - but at the slowest pace in a year.

NORWAY DATA (MNI): Soft Services Inflation Offset by Strong Goods/Food

- NORWAY SEP CPI +0.4% M/M, +3.6% Y/Y

- NORWAY SEP UNDERLYING CPI +0.2% M/M, +3.0% Y/Y

Details of the September inflation report show a continued pullback in services inflation was offset by higher-than-expected food and goods inflation outcomes. While there are some areas of encouragement on the services side, underlying price pressures remain firm overall. This is the only inflation report before Norges Bank's November 6 decision. It's probably not enough to spark any material guidance changes, particularly as November is an interim (non-MPR) meeting.

SWEDEN DATA (MNI): Monthly GDP Tracking Well Above Riksbank Q3 Forecasts

Swedish GDP rose 1.1% M/M in August, according to Statistics Sweden's monthly indicator. This was well above the three forecasts submitted to Bloomberg (median 0.0% M/M). On a 3m/3m basis, GDP is up 1.5%, the highest rate in three and a half years. Current monthly data run rates are well above the Riksbank's September MPR projection of 0.5% Q/Q growth for Q3. The Riksbank is likely to remain at 1.75% for the foreseeable future, but we think the risk of a hike back to 2.00% currently outweighs the risk of another cut.

JAPAN DATA (MNI): Japan Sept CGPI Rises 2.7% Y/Y; Import Price Drops

- JAPAN SEPT CORP GOODS PRICE INDEX +2.7% Y/Y; AUG +2.7%

- JAPAN SEPT CORP GOODS PRICE INDEX +0.3% M/M; AUG -0.2%

Japan’s corporate goods price index (CGPI) rose 2.7% y/y in September, unchanged from August’s unrevised pace, while import prices declined for an eighth consecutive month, Bank of Japan data showed Friday. The index was supported by higher prices for nonferrous metals (+9.6% vs. +6.2% in August) but was weighed down by a smaller increase in agriculture, forestry and fishery products (+30.5% vs. +41.0%).

JAPAN DATA (MNI): Households’ 5-Yr Inflation Stays at 5%

The Bank of Japan's quarterly consumer survey released Friday showed the median inflation forecast five years ahead stood at 5%, unchanged from June, while the share of households expecting prices to rise increased to 84.8% from 83.1%. The median one-year-ahead forecast rose slightly to 10% from 9.9%, reflecting continued concern over high living costs, particularly for food, the survey showed. BOJ officials are heartened by the results as households' inflation view didn't fall despite the slowing year-on-year increase in consumer price index. The results were the similar to the Tankan survey that corporate inflation view didn't fall despite the falling prices.

RATINGS: Belgian & Italian Updates Set to Headline Today

Potential rating reviews of note scheduled for after hours on Friday include:

- Fitch on Switzerland (current rating: AAA; Outlook Stable)

- Moody’s on Belgium (current rating: Aa3; Outlook Negative), Lithuania (current rating: A2; Outlook Stable) & Slovenia (current rating: A3; Outlook Positive)

- S&P on Hungary (current rating: BBB-; Outlook Negative), Italy (current rating: BBB+; Outlook Stable) & the United Kingdom (current rating: AA; Outlook Stable)

- Morningstar DBRS on Lithuania (current rating: A (high), Stable Trend) & Malta (current rating: A (high), Stable Trend)

- Scope Ratings on Cyprus (current rating: A-; Outlook Stable), the European Union (current rating: AAA; Outlook Stable), Hungary (current rating: BBB; Outlook Stable) & Luxembourg (current rating: AAA; Outlook Stable)

FOREX: Two-Way JPY Vol as Japan's Komeito Want to 'Reset' Coalition

- The USD is lower headed into the Friday crossover for the first time this week, aiding a shallow recovery off lows for both EUR/USD and GBP/USD. The greenback fade means the USD Index has retraced ~10% of the month-to-date rally, exposing 99.067 as first major intraday support - the 23.6% retracement of the bounce.

- Japanese politics remains a key focus for markets. JPY (briefly) rallied following headlines that Japan's Komeito Party wish to 'reset' the governing coalition following talks with Takaichi, stating that they cannot support her premiership without alignment.

- The initial JPY strength came on an unwind of expectations on the Takaichi trade (pro-fiscal, monetary easing), who may now face an uphill struggle to be confirmed as PM in a 20 Oct parliamentary session, let alone enact her expansionary policy agenda. The situation is evolving, with higher political risk premia having the potential to work against the JPY as other coalition options are investigated.

- From a technical perspective, bullish trend conditions in USDJPY remain intact, and sights are on 154.39, a Fibonacci retracement point. Initial support to watch lies at 150.92, the Aug 1 high.

- NOK underperforms following this morning’s lower than expected Norwegian inflation data. While the release was dovish on net, Norges Bank may need to see more evidence of declining underlying price pressures before deviating from its cautious stance, particularly with mainland demand still relatively resilient. SEK meanwhile is the strongest in G10 as August Swedish GDP rose much more than expected, supporting analyst, Riksbank and Government expectations for a cyclical recovery in activity going forward. The Riksbank is likely to remain at 1.75% for the foreseeable future, with the risk of a hike back to 2.00% outweighing the risk of another cut - an outlook which today's release supports.

- The combination of these data led NOKSEK 0.45% lower on the day at 0.9430. The cross remains on a sideways trend, with support located at 0.9399, the October 6 low, and key resistance seen around 0.9500.

- Canadian jobs data and the prelim October UMich sentiment release are the market focus Friday. Consensus looks for Canada to have added 5k jobs over September, while seeing consumer sentiment fade in the US.

EGBS: German Curve Bull Flattens; Focus on French PM Announcement Later

Bund futures are +27 ticks at 128.93, with light spillover from JGB futures after the Komeito party withdrew from its coalition with the LDP. A pullback in commodity and European equity futures may also have generated some cross-asset support.

- Initial resistance in Bunds is 129.07, the 76.4% retracement of the Sep 10 - 25 bear leg.

- The German curve has bull flattened, with yields 0.5 to 2.5bps lower. 5s30s is down 1bp to 97.2bps, with focus on interactions with support at 93.4bps (Sep 12 low).

- The 10-year OAT/Bund spread is 0.5bps narrower at ~81.5bps, but analysts remain cautious around tightening prospects in the coming months. Markets are waiting to see if French President Macron will appoint a new prime minister today. While an appointment may reduce near-term political uncertainty, it will likely come at the cost of a worse fiscal trajectory in the 2026 budget.

- Broader EGB spreads to Bunds are mixed. There is some interest in today’s after hours ratings decisions on Belgium and Italy.

- ECB’s Escriva, Kazaks and Dolenc haven’t added much new to the policy debate.

- The US UMich survey and Canadian labour market data headline this afternoon’s macro data calendar.

GILTS: Still Bull Flattening on the Day, Futures Within Yesterday's Range

Gilts remain underpinned, with political news flow out of Japan supporting wider core global FI markets.

- Domestic support comes from the latest REC-KPMG report on jobs, which continued to point to increasing slack within the UK labour market.

- Futures last +28 at 90.74, holding within yesterday’s range after gapping higher at the open.

- Bears remain in technical control, initial support and resistance (90.26 & 91.08) untouched.

- Yields 1.5-4bp lower, curve flatter.

- 10-Year yields around the middle of their multi-week 4.60-4.80% closing range, ~4.71% last.

- NIESR has suggested that Chancellor Reeves should break her promise not to raise taxes on working people in next month's budget, pointing to an increase in income tax.

- We have previously outlined methods that the government could deploy if it chooses to break its manifesto promises:

- SONIA futures flat to +2.5 given the bid further out the curve. BoE-dated OS continues price less than 5bp of BoE easing through year-end, which we think underestimates the odds of a Q4 rate cut.

- Little of note on the UK calendar ahead of the weekend, which will leave cross-market cues & U.S. UoM survey data at the fore.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.960 | -0.7 |

Dec-25 | 3.924 | -4.4 |

Feb-26 | 3.822 | -14.5 |

Mar-26 | 3.787 | -18.0 |

Apr-26 | 3.709 | -25.9 |

Jun-26 | 3.687 | -28.1 |

Jul-26 | 3.639 | -32.8 |

Sep-26 | 3.628 | -33.9 |

EQUITIES: Eurostoxx 50 Futures Consolidate Close to Recent Highs

The trend condition in Eurostoxx 50 futures is unchanged, the direction remains up and the recent consolidation appears to be a flag formation - a bullish continuation pattern. The recent breach of key resistance at 5525.00, the Aug 22 high, confirmed a resumption of the uptrend. Sights are on the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Initial firm support lies at 5550.36, the 20-day EMA. The trend condition in S&P E-Minis is unchanged and the direction remains up. Fresh cycle highs this week confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. The contract is holding on to its latest gains and sights are on 6812.29 and 6819.25, Fibonacci projection points. Initial support to watch is at the 20-day EMA, at 6716.75. A clear break of it would signal scope for a pullback.

- Japan's NIKKEI closed lower by 491.64 pts or -1.01% at 48088.8 and the TOPIX ended 60.18 pts lower or -1.85% at 3197.59.

- Elsewhere, in China the SHANGHAI closed lower by 36.944 pts or -0.94% at 3897.028 and the HANG SENG ended 462.27 pts lower or -1.73% at 26290.32.

- Across Europe, Germany's DAX trades higher by 18.58 pts or +0.08% at 24624.52, FTSE 100 lower by 11.84 pts or -0.12% at 9496.08, CAC 40 up 20.13 pts or +0.25% at 8061.49 and Euro Stoxx 50 up 6.2 pts or +0.11% at 5631.76.

- Dow Jones mini up 53 pts or +0.11% at 46646, S&P 500 mini up 9.5 pts or +0.14% at 6789.25, NASDAQ mini up 49.5 pts or +0.2% at 25339.25.

Time: 10:05 BST

COMMODITIES: Next Target for Gold at $4074.54, a Fibonacci Projection

A bearish theme in WTI futures remains intact and short-term gains are considered corrective. Recent weakness resulted in a move through key support and a bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens the bear threat and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance is at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal. A bull cycle in Gold remains in play and this week’s breach of the $4000 handle reinforces the uptrend. The move higher maintains the price sequence of higher highs and higher lows. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. For now, sights are on $4074.54, a Fibonacci projection. Support to watch is $3817.5, 20-day EMA.

- WTI Crude down $0.18 or -0.29% at $61.28

- Natural Gas down $0.05 or -1.59% at $3.219

- Gold spot up $14.73 or +0.37% at $3992.54

- Copper up $1.9 or +0.37% at $514.1

- Silver up $1.66 or +3.36% at $50.957

- Platinum down $0.77 or -0.05% at $1626.02

Time: 10:05 BST

| Date | GMT/Local | Impact | Country | Event |

| 10/10/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 10/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | St Louis Fed's Alberto Musalem | ||

| 10/10/2025 | 1800/1400 | ** | Treasury Budget |

Note: Due to U.S. government shutdown, some data may be unavailable.