UK DATA: KPMG-REC Report On Jobs Has Something for Everyone

- The KPMG-REC Report on Jobs for September continued to show building slack in the labour market, albeit the pace of change is mixed across sub of the subcomponents.

- Starting salaries only rose "negligbly" in September "with the rate of growth the weakest seen since the current run of pay inflation began just over four-and-a-half years ago."

- Vacancies fell at a marginally slower pace than in August - but were still depressed.

- Permanent placements continued to fall - but at the slowest pace in a year.

- There is something for everyone in this report. The dovish MPC members are more focused on wage slowing wage growth while the more hawkish MPC members are focused on labour market deterioration not happening as fast as earlier in the year (leaving them more focused on inflation persistence). Both of these views can be reinforced from this data. So overall, it doesn't really change the picture too much - and we still think that it is Governor Bailey who will be the swing voter in Q4. This data doesn't rule out him voting for a cut, nor does it lower the bar.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: 10bp Of BoE Cuts Priced Through Dec

A pretty flat start for GBP STIRs, with ongoing domestic focus on the run into the late November Budget as PM Starmer reportedly assembles a “Budget Board” focused on pro-growth policies, while Chancellor Reeves has reportedly limited Cabinet colleague access to the Treasury’s emergency funds ahead of the Budget.

- BoE-dated OIS shows ~10bp of easing through year-end after printing below 8bp in recent sessions.

- SONIA futures -0.5 to +0.5.

- Little of note on the UK calendar until Friday’s monthly economic activity data.

- That will leave wider macro and developments at the fore today, with U.S. PPI data providing the key scheduled risk event.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.976 | +0.9 |

Nov-25 | 3.919 | -4.8 |

Dec-25 | 3.868 | -9.9 |

Feb-26 | 3.756 | -21.1 |

Mar-26 | 3.712 | -25.5 |

Apr-26 | 3.636 | -33.1 |

FOREX: DXY Ticks Lower, Antipodeans Outperform

The broader USD trades on the backfoot early on Wednesday, with headlines noting that President Trump cannot fire Fed Governor Cook for cause at this stage doing little to support the USD (potential for ongoing Trump-related headline risk on that front may be lifting uncertainty and adding weight to the greenback).

- Upticks in global equity markets will also be weighing on the USD, while also helping explain the outperformance for the AUD & NZD amongst G10 FX.

- Zooming out, JPY, EUR & GBP are little changed vs. the USD on the day after recovering from Asia lows.

- EUR/USD based at 1.1690 before a recovery to 1.1710. Initial support at the 20-day EMA (1.1674) went untouched, leaving the bullish technical theme in the pair intact.

- USD/CNH threatened to test yesterday’s lows in recent trade, before a recovery to 7.1180. China’s Finance Minister stressed China’s commitment to using all its proactive fiscal policy space, along with vowing to stabilise international trade and domestic employment conditions. There wasn’t much new in the headlines given by Xinhua.

- Contained reaction in Scandi FX following this morning’s Norwegian CPI & Swedish consumption & production data (see recent bullets for more details).

- U.S. PPI data headlines today’s macro calendar, ahead of CPI data due Thursday.

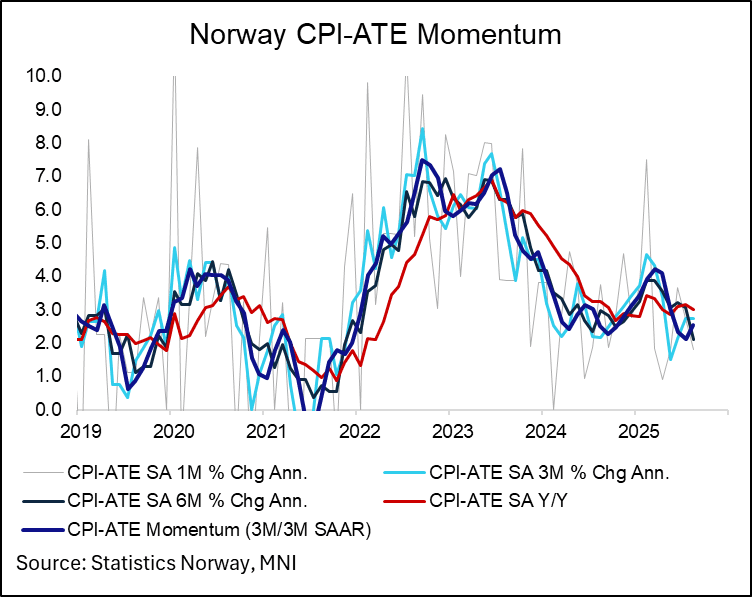

NORWAY: SA CPI-ATE Inflation Consistent With 2% Annualised In August

On a seasonally adjusted basis using Statistics Norway data, CPI-ATE inflation rose 0.15% M/M, after 0.22% in July and 0.30% in June. When annualised, this is a rate slightly below 2%. As such, we think it is consistent with the view that while August inflation was stronger-than-expected, it isn’t enough to stand in the way of a September rate cut in isolation. Tomorrow’s Regional Network Survey remains very import.

- 3m/3m annualised inflation momentum rose to 2.52% in August (vs 2.12% prior) because the March – May period was characterised by soft M/M SA inflation rates averaging 0.13%.

- These rates remain below the 3-4% range seen at the start of this year (which caused Norges Bank to delay its plans for a March rate cut).