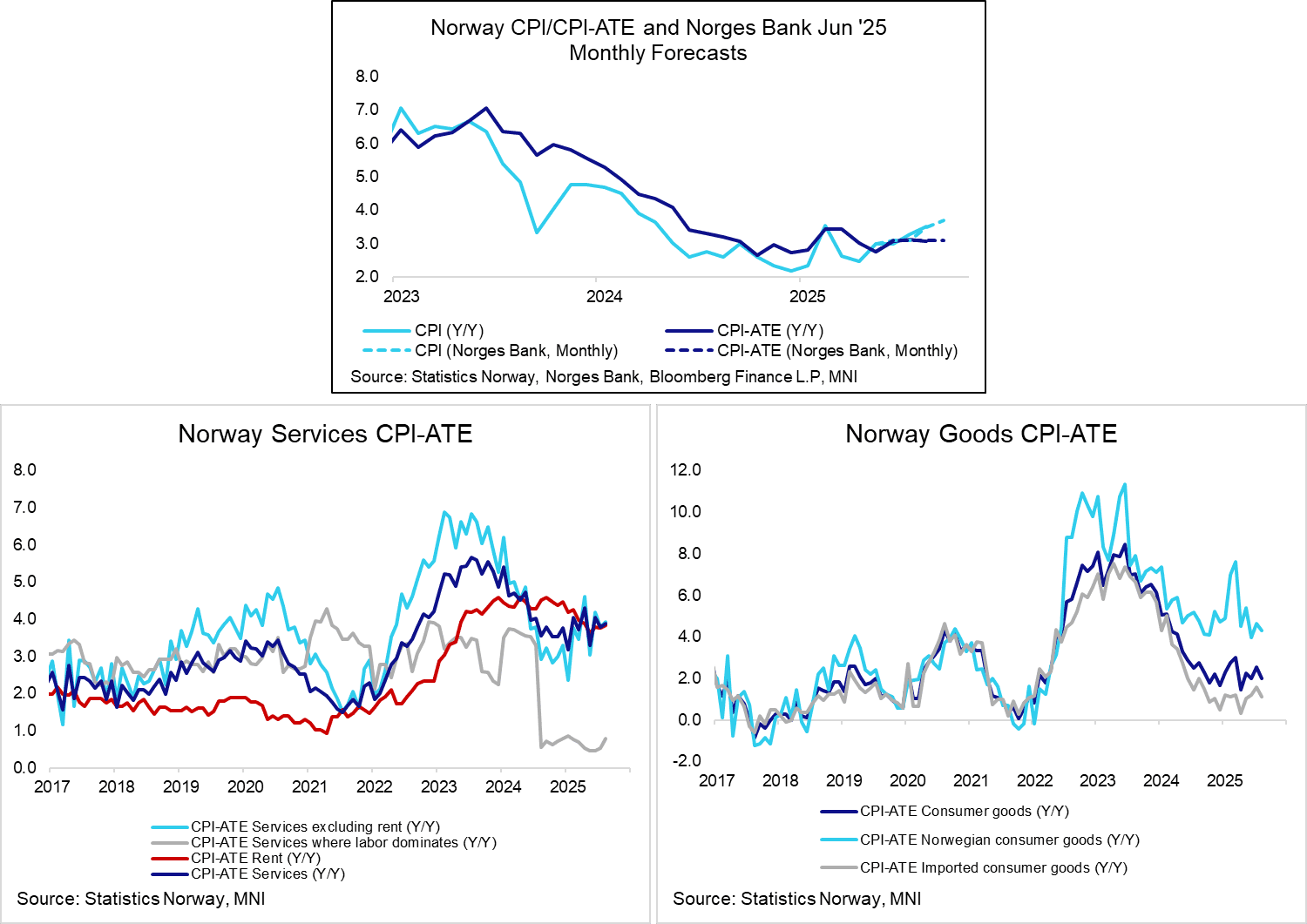

NORWAY: Sep Inflation: Soft Services Offset By Strong Goods/Food

Details of the September inflation report show a continued pullback in services inflation was offset by higher-than-expected food and goods inflation outcomes. While there are some areas of encouragement on the services side, underlying price pressures remain firm overall. This is the only inflation report before Norges Bank’s November 6 decision. It’s probably not enough to spark any material guidance changes, particularly as November is an interim (non-MPR) meeting.

- On a seasonally adjusted basis using Statistics Norway data, CPI-ATE prices rose 0.22% M/M in September - still above 2% on an annualised basis. Various measures of inflation momentum ticked up modestly, with 3m/3m annualised inflation up to 2.62% from 2.52% in August, the highest since May.

- Services excluding rent eased to 3.55% Y/Y (vs 3.93% prior), the lowest since March. There was a notable pullback in recreation and culture services (3.88% Y/Y vs 4.38% prior), restaurants (2.99% Y/Y vs 3.20% prior) and the more volatile accommodation services (4.73% Y/Y vs 7.12% prior).

- Rents inflation continued its gradual deceleration, falling to 3.57% Y/Y from 3.83% in August and 4.18% in January. Rents have been a key driver of elevated CPI-ATE inflation for some time now, so recent disinflation is encouraging.

- Norwegian consumer goods accelerated to 5.36% Y/Y (vs 4.33% prior), driven by both agricultural and non-agri components. There was some uncertainty amongst analysts around food inflation in September. Food prices rose 5.76% Y/Y (vs 4.70% prior), which seems quite a bit higher than expected. Clothing, household textiles and household appliances were also less deflationary in September than in August.

- Imported consumer goods were steady at 1.10% Y/Y (vs 1.11% prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 4: 6617.73 2.0% 10-dma envelope

- RES 3: 6600.00 Round number resistance

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6541.75 High Sep 5

- PRICE: 6538.75 @ 07:23 BST Sep 10

- SUP 1: 6462.58/6371.75 20-day EMA / Low Sep 2

- SUP 2: 6365.35 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirmed a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6456.35, the 20-day EMA.

WTI TECHS: (V5) Trend Needle Points South

- RES 4: $77.85 - 2.794 proj of the Apr 9 - 23 - May 5 price swing

- RES 3: $75.65 - 2.500 proj of the Apr 9 - 23 - May 5 price swing

- RES 2: $74.25 - High Jun 23 and a bull trigger

- RES 1: $66.03/69.36 - High Sep2 / High Jul 30 and key resistance

- PRICE: $63.21 @ 07:19 BST Sep 10

- SUP 1: $61.29 - Low Aug 13 and the bear trigger

- SUP 2: $57.71 - Low May 30

- SUP 3: $54.80 - Low May 5

- SUP 4: $54.03 - Low Apr 9 and a key support

The trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

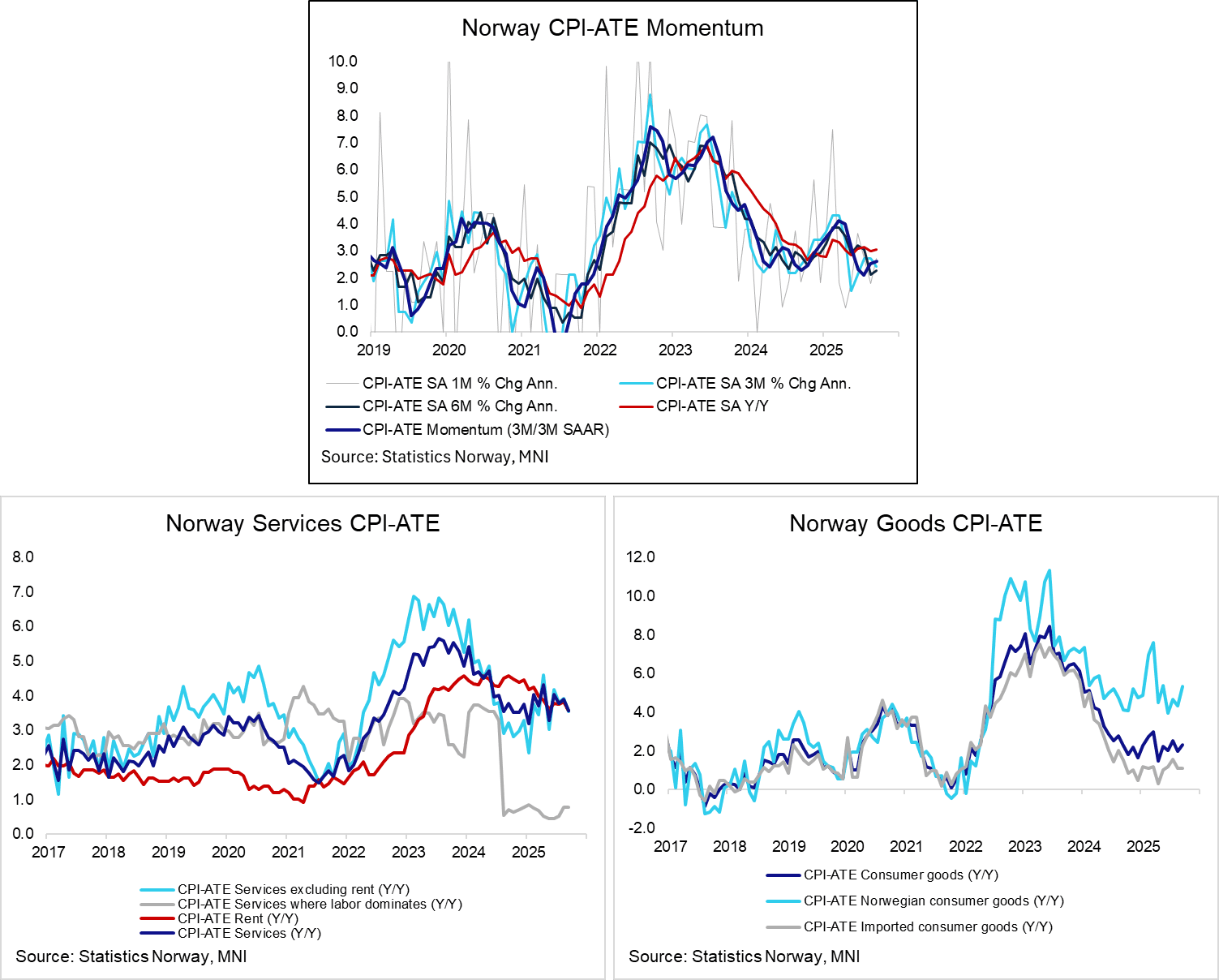

NORWAY: Stronger-than-expected Underlying Inflation, But Not Alarmingly So

CPI-ATE inflation was 3.07% Y/Y in August, after 3.12% in July and 3.07% in June. Overall, we judge it to be a little stronger than expected by analysts and Norges Bank, but not alarmingly so. A portion of CPI-ATE strength came from the volatile airfares category.

- Despite Norges Bank noting at the August decision that “Child daycare prices were reduced from 1 August 2025 and will thus be lower than assumed in the June Report”, Statistics Norway suggests the policy did not have much impact on annual CPI-ATE inflation in August. From the press release: “Despite a large reduction in the maximum price for kindergartens from July to August, this does not significantly reduce the twelve-month growth in the CPI. This is because the maximum price was reduced by about the same amount this year as last year”.

- Excluding these prices from CPI-ATE, Stats Norway notes that inflation would have been 3.9% Y/Y. This underscores why Norges Bank remains cautious in its approach to easing monetary policy – underlying inflation is still quite strong.

- Overall, services excluding rent accelerated to 3.93% Y/Y (vs 3.80% prior). An uptick in airfares (8.34% Y/Y vs -0.18% prior) was an important contributor here. Other services components generally eased a little.

- Rents, which some analysts had expected to decelerate in August, ticked up to 3.83% Y/Y (vs 3.77% prior).

- Elsewhere, food inflation fell to 4.70% Y/Y (vs 5.57% prior), a dynamic that was in line with analyst expectations. This was offset a little by accelerations in non-alcoholic and alcoholic beverage inflation.

- Domestic goods inflation eased to 4.33% Y/Y (vs 4.65% prior), while imported goods fell to 1.11% Y/Y (vs 1.58% prior).

- Headline CPI was 3.53% Y/Y, in line with expectations (vs 3.27% prior). As expected, electricity inflation accelerated in August on a base effect (29.41% Y/Y vs 12.98% prior).