MNI US OPEN - Japan Finance Minister Strengthens FX Warning

EXECUTIVE SUMMARY

- US JOBLESS CLAIMS DATA FOR W/E OCT 18 SLIGHTLY ABOVE MNI'S ESTIMATES

- CHINA RAMPS UP BUYING OF US SOYBEANS AFTER BRIEF PAUSE IN TRADE

- CANADA GOV'T SECURES BUDGET PASSAGE W/LITTLE APPETITE FOR SNAP ELECTION

- JAPAN’S KATAYAMA STRENGTHENS FX WARNING AS YEN SLIDES PAST 155

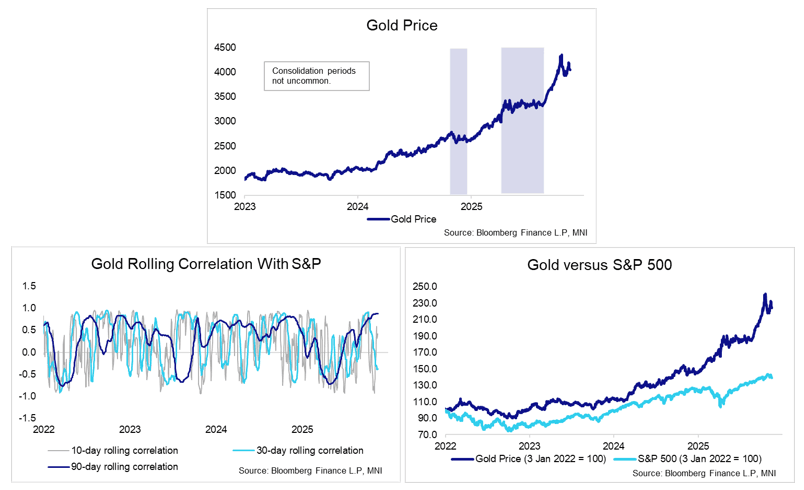

Figure 1: Consolidation period for gold may be healthy, key 50-day EMA support still intact

NEWS

US/CHINA (BBG): China Ramps Up Buying of US Soybeans After Brief Pause in Trade

China has bought nearly a million tons of US soybeans, a move that ends a temporary pause and appears to signal commitment to a trade truce agreed late last month. State-owned agriculture trader Cofco Group booked nearly 20 cargoes of the American oilseed on Monday for delivery in December and January, according to people familiar with the matter who asked not to be identified because they’re not authorized to speak to media. The shipments were from Pacific northwest ports and Gulf coast terminals in the US, they said.

US (NYT): Trump Says U.S. Will Sell F-35s to Saudis, Despite Pentagon Concerns

The president told reporters in the Oval Office on Monday that he planned to sell the advanced fighter jets to Riyadh. President Trump said on Monday that he planned to sell F-35 fighter jets to Saudi Arabia, despite concerns from national security officials in his administration that a sale could create an opportunity for China to steal the planes’ advanced technology. “We will be doing that, we’ll be selling F-35s,” Mr. Trump told reporters gathered in the Oval Office, explaining that the Saudis “want to buy them, they’ve been a great ally.”

CANADA (MNI): Gov't Secures Budget Passage w/Little Appetite for Snap Election

PM Mark Carney secured passage of the first federal budget of his tenure on 17 Nov. This was by a two-vote margin, and only thanks to the backing/abstention of opposition MPs. The budget passed with 170 votes in favour to 168 against, with Carney's centre-left Liberal Party of Canada (LPC) being joined by the sole environmentalist Green MP, Elizabeth May, in supporting the package. Even with May's support, if all other opposition MPs had voted against the budget, it would have been enough to defeat it. Given that federal budget votes are deemed confidence motions, this would have sparked a snap federal election. Instead, two MPs from the main opposition centre-right Conservatives (CPC) and two from the left-wing New Democratic Party (NDP) abstained on the vote.

EU (BBG): EU Bankers Prepare for Capital Buffer Overhaul to Disappoint

Banking executives in the European Union are bracing to be disappointed when officials lay out proposals to cut red tape in the coming weeks, as they predict that the measures will be far behind the deregulation taking place in the US. A task force of top euro area officials is set to deliver proposals on bank capital buffers and other efficiency measures to the European Central Bank before the end of the year. The findings are likely to be key input for the European Commission as it prepares a major report on the EU banking sector to be published in 2026.

UK (The Telegraph): Labour Backlash Growing Over Asylum Crackdown

Shabana Mahmood is facing a growing Labour backlash over her plan for the biggest overhaul of the asylum system since the Second World War. The Home Secretary is proposing fundamental reforms to increase deportations and reduce the pull factors making Britain Europe’s destination for “asylum shoppers”. However, Labour MPs accused the government of promoting rhetoric that risked “divisiveness” and fueled racism and abuse, with one claiming the plans were “performatively cruel” and “economically misjudged”.

JAPAN (BBG): Japan’s Katayama Strengthens FX Warning as Yen Slides Past 155

Japan’s Finance Minister strengthened her warning over the yen’s slide as the currency fell past the 155-per-dollar level, as reports of a larger-than-expected economic package fuels the view that Prime Minister Sanae Takaichi’s pro-stimulus stance may slow Bank of Japan rate hikes. “I’m seeing extremely one-sided and rapid movements in the currency market,” Finance Minister Satsuki Katayama told reporters on Tuesday. “I’m deeply concerned about the situation.”

JAPAN (MNI): Ueda & Takaichi Reaffirm Prior Comments

Nothing to really alter the picture in markets in the comments that follow the meeting between Japanese PM Takaichi and BoJ Governor Ueda. Ueda noted that he told Takaichi that the Bank is operating a process of gradually adjusting its monetary easing, which the PM "seemed to acknowledge". The Governor stressed the focus on a smooth landing towards the Bank's inflation target. Ueda also noted that the two discussed FX but wouldn't comment on specifics, instead reaffirming that it is desirable for FX to move in a stable manner, reflecting fundamentals.

JAPAN (BBG): Japan Ruling Party Bloc Pushes for Big Jump in Extra Budget

A group of lawmakers in Japan’s ruling Liberal Democratic Party urged Prime Minister Sanae Takaichi to craft an extra budget much larger than what’s been indicated thus far as she puts the finishing touches on her economic package. The Responsible and Expansionary Fiscal Policy Caucus called for an extra budget worth about ¥25 trillion ($161 billion) to fund the forthcoming stimulus, according to the proposal the group submitted to Takaichi on Tuesday. The amount far exceeds the roughly ¥14 trillion reported by local media to be under consideration. A year ago, former Prime Minister Shigeru Ishiba rolled out a ¥13.9 trillion spending plan.

RBA (MNI): RBA Outlines Factors That Will Drive Pause - Minutes

Stronger demand, reduced supply capacity and signs that the 3.6% cash rate may not be as restrictive as previously thought could lead the Reserve Bank of Australia to hold rates at coming meetings, minutes of the Board’s November session showed Tuesday. Members noted that any of these scenarios would limit the scope for further monetary easing, particularly with inflation having been above target for several years. The board held the cash rate steady at the November session, citing higher underlying inflation and concerns around supply capacity.

RUSSIA/UKRAINE (MNI): No Russian Participation in Zelenskyy-Witkoff Istanbul Talks - Kremlin

Kremlin spox Dmitry Peskov has said that Russia will not participate in the 19 November talks planned in Istanbul involving Ukrainian President Volodymyr Zelenskyy, US Middle East envoy Steve Witkoff and (presumably) Turkish officials. While saying Russia will not participate, Peskov claims that "Russia remains open to negotiations", and that its position is well known in Washington, Istanbul and Kyiv.

RUSSIA/CHINA (BBG): Fear of Sanctions Stymies Russia-to-China Oil Flows for Now

Expanding sanctions on Chinese ports and refiners are choking flows of Russian and Iranian oil to the world’s No. 1 importer, although emerging workarounds suggest the slowdown may be fleeting. The big state-owned processors have paused purchases of ESPO, the crude that makes up the bulk of China’s imports from Russia, following US sanctions on producers Rosneft PJSC and Lukoil PJSC. Washington’s targeting of the Rizhao oil terminal, which handled about a 10th of China’s crude imports, is also crimping Iranian flows.

CORPORATE (BBG): Amazon Raises $15 Billion in First US Bond Sale in Three Years

Amazon.com Inc. raised $15 billion in its first US dollar bond offering in three years, adding to a spree of jumbo debt sales by technology firms as they race to fund artificial-intelligence infrastructure. The proceeds of the deal — which topped initial estimates by $3 billion — will be used for everything from acquisitions and capital expenditures to share buybacks, according to people with knowledge of the matter.

MNI NBH PREVIEW: Hawkish Risks Bolster Case for Hold

The National Bank of Hungary is expected to keep the base rate on hold at 6.50% for the 14th consecutive month, sticking to its ‘cautious and patient’ approach to monetary policy as headline inflation continues to run above target. Pro-inflationary government measures and the possibility of sovereign ratings downgrades pose hawkish risks. All 20 analysts surveyed by Bloomberg expect the base rate to be left unchanged.

DATA

US DATA (MNI): Jobless Claims Data for W/E Oct 18 Slightly Above MNI's Estimates

- US JOBLESS CLAIMS AT 232K IN OCT. 18 WEEK: GOVT WEBSITE (BBG)

At the time using state-level data, MNI had estimated jobless claims in the week to Oct 18 to be a seasonally adjusted 227k - so 5k below the 232k figure being presented here. Data for the week-ending Sep 20 and Sep 13 are also available:

- Sep 20: 219k vs MNI estimate of 218k

- Sep 13: 232k vs MNI estimate of 231k

Note that data for the week ending Oct 18 is technically a payrolls reference period, as was the week ending Sep 13 (that's possibly why the Oct 18 is being published now). The DOL source we posted earlier suggests claims data for the week ending Sep 27, Oct 4 and Oct 11 are not yet available.

MNI UK DATA PREVIEW: October 2025 Inflation Release

Governor Bailey's vote at the December MPC meeting is still far from guaranteed despite last week's soft labour market data. We still think that assuming data comes in broadly in line with expectations and we don't have an inflationary Budget that Bailey will vote to support a cut at the December MPC meeting, which would hence see a 5-4 vote for a pre-Christmas 25bp cut. The BOE November MPR forecast looks for headline CPI to come in at 3.60%Y/Y - this forecast is 11 hundredths below the August MPR expectation following a 21 hundredth downside surprise in September.

CHINA DATA (MNI): China Oct Youth Unemployment Slight Improvement

MNI (Beijing) China’s youth unemployment rate for 16-to-24 year old urban workers was 17.3% in October, an improvement from 17.7% in September and August's year-high 18.9%, data from the National Bureau of Statistics showed on Tuesday. The rate for 30-to-59 year old urban workers was 7.2%, unchanged month-on-month. In October, the overall national urban survey unemployment rate was5.1%, down 0.1 percentage points from the previous month, data from the bureau released last week showed.

FOREX: USDJPY Uptrend Remains Intact as Takaichi - Ueda Meet Affirms Gradualism

- Ongoing weak risk sentiment underpins low yielding haven currencies JPY and CHF in a session seeing limited volatility so far. Markets await key official economic data reducing uncertainty about the macro picture - clearing up the Fed policy path for the rest of the year.

- CAD outperforms after PM Mark Carney secured passage of the first federal budget of his tenure, suggesting that despite external headwinds, the Canadian political environment will remain relatively stable in the short-to-medium term. Expectations for a further Bank of Canada cut in this cycle let alone December are pretty much eliminated by now, with the short-term outlook for USDCAD appearing bearish form a technical perspective. Firm core indicators in yesterday's CPI report, in conjunction with earlier stronger-than-expected labour market data have combined to pretty much eliminate expectations for a further Bank of Canada cut in this cycle.

- USDCAD is trading inside a bull channel drawn from the Jul 23 low. The top of the channel - currently at 1.4170 - provided a firm resistance on Nov 11. The subsequent move down highlights scope for a bear extension towards the base of the channel at 1.3893. Initial key support to watch is 1.3968, the 50-day EMA.

- USDJPY price action meanwhile confirmed the resumption of an uptrend and extension of recent gains, with sights on 155.53, a Fibonacci projection. Comments following the meeting between Japanese PM Takaichi and BoJ Governor Ueda did not move the needle, with Ueda noting that he told Takaichi that the Bank is operating a process of gradually adjusting its monetary easing, which the PM "seemed to acknowledge". Initial firm support in USDJPY would be 153.49, the 20-day EMA, a clear breach of which would signal scope for a corrective pullback.

- Fed's Barr and Barkin, the ECB's Pereira and Dolenc, as well as the BoE's Pill and Dhingra are scheduled to speak. Barkin is due to comment on the economic outlook having not commented directly on policy since the last Fed decision.

- The US data calendar is starting to pick up, with weekly ADP, November NY Fed services, weekly redbook retail sales, November NAHB housing index, August factory orders, and September TIC flows likely being released today ahead of tomorrow's UK CPI. A roughly inline UK inflation print with a non-inflationary budget may ensure key voter Bailey will support December cut, which could keep the pressure on GBP.

EGBS: German 5s30s Meets Resistance Again; 2026 Issuance Details Needed

The German 5s30 curve has once again met resistance around 103.7bps, a level which has contained upside on several occasions since mid-September. Although the 2026 German budget (passed last week) contained higher net debt than initial drafts, markets are still awaiting details on how the expected issuance ramp-up will be distributed across the curve. As such, details of DFA’s 2026 issuance plan (usually presented in mid-December) may be necessary before 5s30s can make a fresh challenge of year-to-date highs of 111bps.

- Renewed interest in long-end swap spread/ASW wideners on Dutch pension fund dynamics may have also played a role (even with spreads a touch off recent highs at typing). The EUR 5s30s swap curve (vs 3m Euribor) is currently at a fresh multi-year high of 70.5bps.

- Intraday, the curve is bull steeper, with 5-year yields down 2.5bps and 30-year yields little changed.

- Bund futures are +17 ticks at 128.82, seemingly finding support from a continued pullback in European equities (though we caveat that these correlations have not been too reliable in recent sessions). Initial resistance in Bunds is seen at the 50-day EMA of 129.10.

- 10-year EGB spreads to Bunds are up to 1.5bps wider. The OAT/Bund spread is back at 75bps, with political developments still in focus.

- The EU is holding a syndicated tap (E5bln WNG) of the 2.50% Oct-30 EU-bond today. Meanwhile, Slovakia sold SlovGBs and Finland will sell RFGBs at 1100GMT.

- There is no regional data scheduled today, while the only remaining ECBspeak comes from Bank of Slovenia’s Dolenc.

Figure 1: German 5s30s Curve

GILTS: Early Demand Stalls as Risk Sentiment Stabilises

Gilts initially drew support from a move lower in global equity markets, before stabilsation in wider risk sentiment and an uptick from session lows in crude oil limited demand.

- Gilt futures trade +8 at 92.47 vs. highs of 92.60.

- Initial support and resistance located at 91.94 & 92.85. Our technical analyst still deems the recent weakness to be corrective at this stage.

- Yields ~0.5bp lower across the curve.

- 2s10s and 5s30s got within 1bp of October closing highs.

- Gilt/Bunds 1.5bp wider at 183.5bp after failing to push above 185bp in recent sessions, still holding most of the recent recovery from sub-175bp.

- The GBP.125bln tender of the 4.75% Dec-30 line passed smoothly.

- BoE-dated OIS pricing 18.5bp of easing for December (~75% odds of a cut).

- SONIA futures little changed to +2.0, with SONIA-implied BoE terminal rate pricing little changed on the day, at 3.39%.

- Comments from BoE’s Pill (voted to leave rates unchanged earlier this month) & Dhingra (the most dovish MPC member) are due today.

- A reminder that we do not expect much market vol. to stem from any non-Bailey BoE comments in the lead up to the December decision, given the entrenched views of the other MPC members (Bailey is deemed the key swing voter).

- Immediate focus remains on tomorrow’s inflation data and next week’s Budget.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.785 | -18.4 |

Feb-26 | 3.697 | -27.3 |

Mar-26 | 3.619 | -35.0 |

Apr-26 | 3.519 | -45.0 |

Jun-26 | 3.476 | -49.3 |

Jul-26 | 3.427 | -54.2 |

Sep-26 | 3.404 | -56.5 |

EQUITIES: E-Mini S&P Maintains a Softer Short-Term Tone

A M/T bull trend in Eurostoxx 50 futures remains intact, however, the latest sell-off highlights a stronger corrective cycle. The move down this week has resulted in the breach of two key support points; 5606.50, the 50-day EMA, and 5604.50, the base of a bull channel drawn from the Aug 1 low. The breach signals scope for a deeper pullback and opens 5503.00, a Fibonacci retracement. Initial resistance to watch is 5675.90, the 20-day EMA. S&P E-Minis maintain a softer short-term tone. The below support at 6655.70, the Nov 7 low cancel recent bearish signals and signals scope for an extension of the current corrective cycle. Note that price has also breached support at the 50-day EMA. An extension would open 6540.25, the Oct 10 low and the next key support. Initial firm resistance to watch is 6793.65, the 20-day EMA.

- Japan's NIKKEI closed lower by 1620.93 pts or -3.22% at 48702.98 and the TOPIX ended 96.43 pts lower or -2.88% at 3251.1.

- Elsewhere, in China the SHANGHAI closed lower by 32.222 pts or -0.81% at 3939.813 and the HANG SENG ended 454.25 pts lower or -1.72% at 25930.03.

- Across Europe, Germany's DAX trades lower by 300.06 pts or -1.27% at 23292.55, FTSE 100 lower by 93.17 pts or -0.96% at 9582.31, CAC 40 down 107.64 pts or -1.33% at 8011.18 and Euro Stoxx 50 down 75.28 pts or -1.33% at 5566.43.

- Dow Jones mini down 132 pts or -0.28% at 46540, S&P 500 mini down 19 pts or -0.28% at 6674, NASDAQ mini down 84.25 pts or -0.34% at 24802.

Time: 10:00 GMT

COMMODITIES: Key Support to Watch for Gold at $3932.10, the 50-Day EMA

A sell-off in WTI futures on Nov 12 strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction. The downleg in Gold between Oct 20 and 28 appears to have been a correction and has allowed an overbought condition to unwind. Recent gains suggest that correction is over. With the metal retracing from last week’s high, the key support to watch lies at the 50-day EMA, at $3932.1. Clearance of this EMA would signal scope for a deeper retracement. The short-term bull trigger has been defined at $4245.23, the Nov 13 high.

- WTI Crude down $0.18 or -0.3% at $59.73

- Natural Gas down $0.01 or -0.18% at $4.354

- Gold spot down $3.87 or -0.1% at $4043.47

- Copper down $2.5 or -0.49% at $506.15

- Silver up $0.17 or +0.34% at $50.4359

- Platinum up $7.42 or +0.48% at $1545.57

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 1700/1700 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders | |

| 19/11/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 19/11/2025 | 0030/1130 | *** | Quarterly wage price index | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 19/11/2025 | 0700/0700 | *** | Producer Prices | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 19/11/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 19/11/2025 | 1330/0830 | ** | Trade Balance | |

| 19/11/2025 | 1500/1000 | Fed Governor Stephen Miran | ||

| 19/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 19/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 19/11/2025 | 1730/1230 | BOC Deputy Vincent speaks in Quebec City (Time TBC) | ||

| 19/11/2025 | 1745/1245 | Richmond Fed's Tom Barkin | ||

| 19/11/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 19/11/2025 | 1900/1400 | New York Fed's John Williams | ||

| 19/11/2025 | 1900/1400 | *** | FOMC Minutes |

Note: US Government data releases are still TBD pending an official release schedule.