MNI US OPEN - Iran Seeks to Limit US Talks to Nuclear Activity

EXECUTIVE SUMMARY

- IRAN WANTS US TALKS CHANGED TO OMAN AND LIMITED TO NUCLEAR FILE: BBG

- NVIDIA AI CHIP SALES TO CHINA STALLED BY US SECURITY REVIEW: FT

- TRUMP’S VIEW OF COLOMBIA LEADER SWINGS FROM ‘SICK’ TO ‘TERRIFIC’

- MNI BOE PREVIEW: AGENTS PAY, INDIVIDUAL PARAS

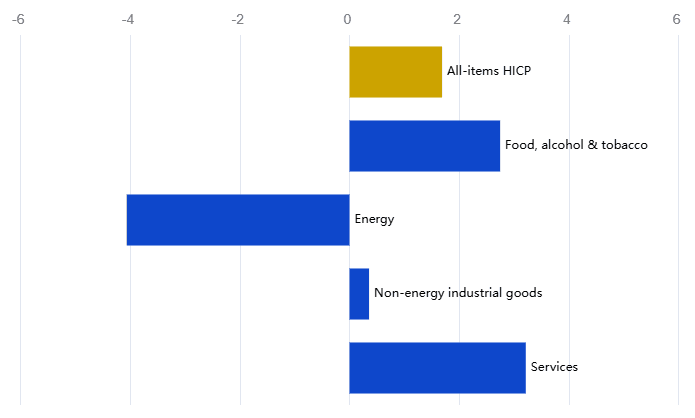

Figure 1: Euro area annual inflation eases to 1.7% in January, in line with estimates

Source: Eurostat

NEWS

US/IRAN (BBG): Iran Wants US Talks Changed to Oman and Limited to Nuclear File

Iran has asked the US to move diplomatic talks originally planned for Turkey to Oman and to limit the agenda to the Islamic Republic’s nuclear program, according to people familiar with the matter. Tehran wants the talks, originally planned for Friday in Istanbul, to focus only on Iran’s nuclear activities and not its support for proxy militias in the Middle East and its ballistic missiles, said the people, who asked not to be named discussing private matters. They added that Tehran also opposed the participation of regional countries, aside from Turkey, in the negotiations.

US/RUSSIA/UKRAINE (NYT): Ukraine Talks Set to Resume, Following a Huge Attack by Moscow

The second round of peace talks among Russian, Ukrainian and American officials was set to begin Wednesday in the United Arab Emirates, following another huge Russian attack on Ukraine’s power grid early Tuesday. Negotiators were expected to discuss the two main sticking points in reaching a peace deal: the fate of Ukrainian-controlled territory in the east that Russia wants, and how Ukraine’s security would be guaranteed if Russia again attacks.

US/CHINA (FT): Nvidia AI Chip Sales to China Stalled by US Security Review

Nvidia’s sales of H200 AI chips to China are still awaiting final approval from Washington nearly two months after Donald Trump greenlit exports, as the US government conducts a national security review before granting licences to Chinese customers. Chinese customers are not placing H200 chip orders with Nvidia until it becomes clear whether they will be able to secure the licences or what conditions will be attached, people familiar with the discussions told the FT.

US/COLOMBIA (BBG): Trump’s View of Colombia Leader Swings From ‘Sick’ to ‘Terrific’

President Donald Trump’s opinion of Colombia’s leader swung from “sick” to “terrific” as a face-to-face White House meeting eased tensions between the ideological foes. Trump and President Gustavo Petro discussed the war on drugs, energy and security in their two-hour sit-down at the Oval Office. “He and I weren’t exactly the best of friends, but I would have felt it because I never met him,” Trump told reporters in Washington. As recently as last month, Trump had accused Petro of being involved in the cocaine trade, and even threatened military strikes on Colombia.

US (Semafor): Bessent Testifies Before Congress Amid Fed Drama

Treasury Secretary Scott Bessent is set to testify before the House Financial Services Committee Wednesday and the Senate Banking Committee on Thursday. It’ll be lawmakers’ first chance to grill him after the Justice Department opened an investigation into Federal Reserve Chair Jerome Powell — but don’t expect Republicans to partake. Financial Services Chair French Hill, R-Ark., told Semafor he wants Bessent to “illustrate how much better the American economy is doing than [was] forecast” a year ago, as well as to weigh in on why Republicans’ proposal to roll back regulations on smaller banks “is helpful to boosting economic growth.”

US (FT): Senators Push $70bn Funding Deal to Support Donald Trump’s Critical Minerals Agenda

Senators will introduce legislation on Wednesday to reauthorise funding for the US Export-Import Bank for the next decade, as lawmakers try to inject an extra $70bn into an agency that plays an increasingly central role in shoring up energy and minerals projects. Kevin Cramer, the Republican senator from North Dakota who is co-sponsoring the reauthorisation legislation with Democrat Mark Warner, told the FT that Donald Trump was “all in” on funding the Ex-Im Bank, adding the US president “sees the value” of the institution. Cramer said he would advocate for Ex-Im’s lending cap to be lifted from $135bn to $205bn as part of the reauthorisation package.

US (BBG): Nvidia Nears Deal to Invest $20 Billion in OpenAI Round

Nvidia Corp. is nearing a deal to invest $20 billion in OpenAI as part of its latest funding round, according to people familiar with the matter, marking the chipmaker’s single biggest investment in the ChatGPT developer. Nvidia’s contribution is close to being completed, according to the people, who spoke on condition of anonymity because the information is not public. The deal is not final and the terms could change. OpenAI declined to comment. Nvidia declined to comment. OpenAI is looking to raise up to $100 billion in funding for a new round, with much of that coming from large tech firms, Bloomberg News has reported.

US (MNI): Fed Governor Miran Resigns White House Post

Federal Reserve Governor Stephen Miran has stepped down from his position as chair of the White House Council of Economic Advisers, MNI confirmed. Miran joined the Trump administration’s Council of Economic Advisers in January 2025. He had been on leave from this post since September 2025, when he became a member of the Federal Reserve Board of Governors. The Fed governor took the seat vacated by Joe Biden appointee Adriana Kugler. Miran's term as a Fed governor has expired but will remain on the seat until there is a replacement.

US (NYT): Trump Repeats Call to ‘Nationalize’ Elections, as White House Walks It Back

President Trump’s extraordinary comments were the latest iteration of his unsubstantiated claims that U.S. elections are rigged as Republicans face potentially big losses next year. President Trump doubled down on his extraordinary call for the Republican Party to “nationalize” voting in the United States, even as the White House tried to walk it back and members of his own party criticized the idea. Mr. Trump said on Tuesday that he believed the federal government should “get involved” in elections that are riddled with “corruption,” reiterating his position that the federal government should usurp state laws by exerting control over local elections.

US/S.KOREA (BBG): South Korea’s Top Envoy Meets Rubio as Trump’s New Tariff Looms

South Korea’s top diplomat met with Secretary of State Marco Rubio as the country scrambles to avoid a threatened US tariff hike to 25% while lawmakers in Seoul prepare to review a special bill required to implement funding pledged as part of last year’s trade agreement. Cho Hyun held talks with Rubio in Washington on Tuesday on the sidelines of a ministerial meeting on critical minerals, South Korea’s Foreign Ministry said.

MNI BOE PREVIEW: Agents Pay, Individual Paras

The upcoming Bank of England meeting is probably the least anticipated quarterly meeting for some time with the MPC expected to leave Bank Rate on hold and leave guidance unchanged, but there are still aspects worth watching. Most in focus will be the vote split (we expect to be 7-2, in line with consensus), the Agents’ Pay Survey (which will be published alongside the decision) and the individual member paragraphs. We look at all of these in detail. We also summarise over 20 sellside previews - a 7-2 vote split is expected by around 2/3 of analysts with risks of 6-3 seen.

UK (MNI): UK Unemployment Will Peak at 5.4% - NIESR

UK unemployment will peak at 5.4%, the National Institute of Economic and Social Research said in its quarterly forecast on Wednesday, as it expects 50 basis points of further cuts to Bank Rate this year. "We expect that continued cooling in labour market activity will dampen pay growth" and inflation, it said, and inflation is expected to return to 2% "on a lasting basis from the second quarter of this year. "The UK economy is "closer to normal than at any point in the last decade," Director David Aikman said on Tuesday at a press conference, in spite of the difficult fiscal picture.

RIKSBANK (MNI): Riksbank Minutes Show Jansson Saw Case for Cut

Riksbank Deputy Governor Per Jansson saw the case for a rate cut at the January meeting the minutes showed. Jansson, one of the four voting members of the Riksbank's Executive Board, said underlying measures showed a consistent picture of below target inflationary pressures and the appreciation of the krona, which started in early 2025, appeared to be a key factor driving inflation down, although he voted for unchanged policy.

CHINA (BBG): Top China Official Vows to Boost Consumption to Overhaul Economy

China will press ahead with building a unified market to unleash domestic consumption as countries around Asia face a “pivotal juncture” in the transformation of the global economy, a top economic official said. As the country opens its economy further, it will create more business opportunities for the region, Vice Finance Minister Liao Min said in a speech delivered on Wednesday at a meeting of finance and central bank deputies from Asia‑Pacific Economic Cooperation (APEC) member economies in Shanghai.

RBNZ (MNI INTERVIEW): RBNZ to Keep OCR Steady - McDermott

A former RBNZ assistant governor shares his OCR outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

MNI BANXICO PREVIEW: Risk of Extended Pause

Banxico is widely expected to remain on hold at 7.00% on Thursday, as it takes its time to assess incoming data amid concerns about persistent core CPI inflation pressures. The recent shift in the committee’s guidance, plus confirmation from an MNI interview with Deputy Governor Cuadra, has all but cemented an easing cycle pause. Further ahead, however, the weak growth backdrop keeps the door open to renewed rate cuts later this year.

DATA

EUROZONE DATA (MNI): HICP in Line, but Variation on Subcomponents

- Headline 1.69% (1.7% MNI tracking and consensus, 1.97% prior)

- Core 2.19% (2.2% MNI median, 2.37% prior)

- Services 3.21% (3.3% MNI median, 3.42% prior)

- NEIG 0.36% (0.5% MNI median, 0.34% prior)

- FAT 2.74% (2.5% MNI median, 2.51% prior)

- Energy -4.06% (-4.5% MNI median, -1.94% prior)

Note all priors using ECOICOP2 rather than the values published at the time. Services around a tenth softer than expected (0.09ppt), NEIG 0.14ppt softer. But overall core is broadly in line - so suggests the core expectation wasn't fully consistent with services / core goods. FAT and energy are both higher than expected. Overall this leaves headline 1.69% Y/Y - in line with the 1.7% MNI tracking and consensus.

EUROZONE JAN FINAL SERVICES PMI 51.6 (51.9 FLASH, 52.4 DEC) (MNI)

GERMANY JAN FINAL SERVICES PMI 52.4 (53.3 FLASH, 52.7 DEC) (MNI)

FRANCE JAN FINAL SERVICES PMI 48.4 (47.9 FLASH, 50.1 DEC) (MNI)

SPAIN DATA (MNI): PMI Details Still Solid Despite Weaker-Than-Expected Print

- SPAIN JAN SERVICES PMI 53.5 (56.8 EXP, 57.1 DEC)

- SPAIN JAN COMPOSITE PMI 52.9 (55.4 EXP, 55.6 DEC)

Although weaker than expected, the details of the Spanish services PMI aren't too worrying - employment growth in particular remains "highly positive". The services and composite PMIs have been in expansionary territory for over two years now. Key notes from the release: "The downshift in sector expansion was closely correlated with an easing of new business growth in January to its slowest since last June. Whilst market demand was reported to have remained positive, panellists detected a weakening of demand growth, especially when compared to levels seen in the second half of 2025."

ITALY DATA (MNI): Services PMI Stronger Than Expected Despite Export Weakness

- ITALY JAN SERVICES PMI 52.9 (51.3 EXP, 51.5 DEC)

- ITALY JAN COMPOSITE PMI 51.4 (50.1 EXP, 50.3 DEC)

The Italian January services PMI was stronger than expected, helping the composite retrace around half of December's fall. Sales volumes and new orders grew relative to December, the latter despite weakness in export markets. Like Spain, there was another increase in employment in January. Key notes from the release: "In January, total sales volumes rose again across the sector, but at the slowest pace since August last year"

UK DATA (MNI): Services PMI Revised Down; Wage Increases and Passthrough Still Concern

- UK JAN FINAL SERVICES PMI 54.0 (54.3 FLASH, 51.4 DEC)

A downward revision to the services PMI by 0.3 points, but the areas of concern for the doves are still there in the forms of payroll costs pushing up output prices by the most since August. And improving sentiment also flagged. From the press release: "Higher payroll costs were by far the most commonly cited factor pushing up input prices in January. Latest data signalled a sharp rate of overall cost inflation, albeit slightly lower than December's seven-month high. Greater technology costs and raw material prices (especially food and metals) were also noted at the start of the year."

SWEDEN DATA (MNI): Surveys Suggest Economy Started The Year On Solid Footing

The Swedish January services PMI was below the three analyst forecasts submitted to Bloomberg (range 56.5-57.0), but at 54.3 (vs 56.3 prior) was still the sixth consecutive month in expansionary territory. That left the composite PMI at 54.8 (vs 56.0 prior). Overall, the January PMI and Economic Tendency Indicator surveys suggest the Swedish economic started the year on a solid footing, consistent with Riksbank and analyst expectations. In January, services production and new orders remained above the neutral 50 level, at 56.1 and 55.2 respectively.

NEW ZEALAND DATA (MNI): NZ Q4 Unemployment Rises to 5.4%

New Zealand’s unemployment rate rose 10 basis points to 5.4% in the fourth quarter, up from 5.3% in Q3, data released by Stats NZ on Wednesday showed. The underutilisation rate was unchanged at 13.0%, while the employment rate edged up to 66.7% from 66.6% in the previous quarter. In the year ended December 2025, all salary and wage rates, including overtime, increased 2.0%. Average weekly earnings for full-time equivalent employees rose to NZ$1,712 from NZ$1,651, while average ordinary time hourly earnings increased to NZ$43.99 from NZ$42.57.

FOREX: USDJPY Recovery Extends, Dovish Riksbank Minutes Weigh on SEK

- USDJPY continues to grind higher on Wednesday, extending the recovery from last week’s lows to 3%. The move back above the 50-day EMA, intersecting at 155.75, undermines the recent bear theme and highlights a stronger short-term bull cycle. Price action this morning has bridged the gap to initial resistance at 156.64, the 61.8% retracement of the Jan 14 - 27 bear leg, with 157.72 the next topside level of note.

- The swift recovery has been primarily driven by a more stable backdrop for the dollar following Kevin Warsh’s nomination, while expectations for the LDP securing a majority bring concerns surrounding Japan’s fiscal trajectory back to the fore. The firmer dollar has weighed on NZD (-0.45%) after mixed Q4 unemployment has failed to reignite bullish Kiwi momentum.

- USDCNY and USDCNH saw some buying interest in European trade, with both pairs edging to new session highs of 6.9425 and 6.9404 respectively - but we note no specific headlines behind the move. News that Putin is holding a videocall with Xi Jinping unlikely to be the driver here, but moves do follow the further strength in the CNY fix Wednesday: the 6.9533 fix was again the lowest since mid-2023 but still well above expectations (survey saw today's fix at 6.9363).

- Riksbank minutes are driving SEK underperformance. The debate amongst the Board over the next few months is clearly between holding the policy rate steady (the most likely scenario) and delivering another cut (only likely if both inflation and economic activity are weaker than expected). EURSEK has advanced 0.5% to 10.58, extending a moderate bounce from yesterday’s 10.50 cycle lows. The 20-day EMA intersects at 10.6336.

- Fed's cook is scheduled to speak on monetary policy and the economy later today, and ISM services highlights the data calendar today. Focus then turns to tomorrow's ECB and BoE decisions.

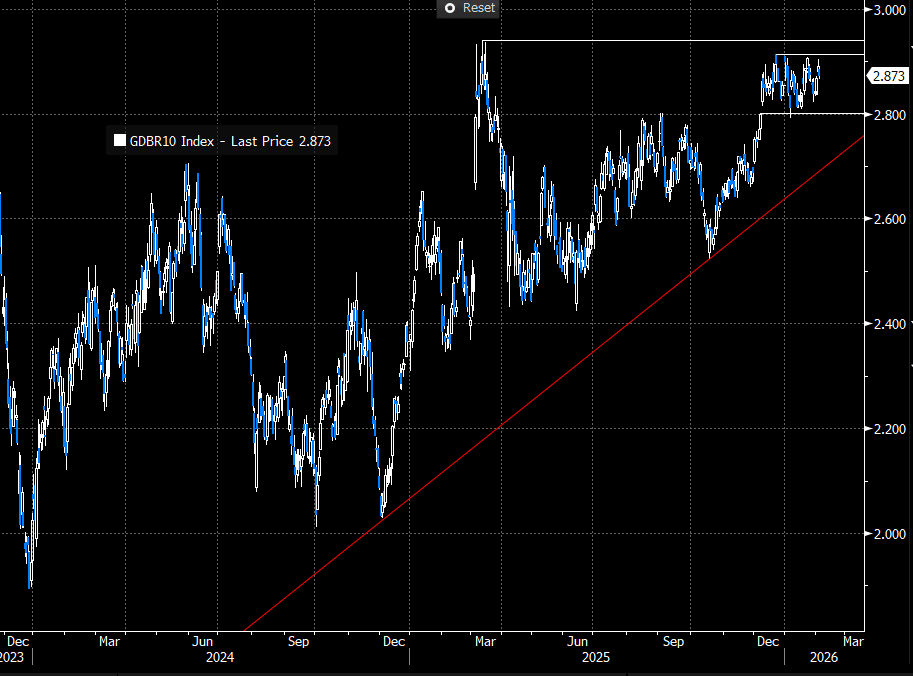

EGBS: 2.90% Again Contained Upside in 10-year Bund Yields Yesterday

10-year Bund yields were once again unable to sustain a move above 2.90% yesterday. Yields are back at 2.875% at typing. The key topside levels to watch remain 2.914% (Dec 22 high) and the more important 2.94% (March 2025 high). Although the medium-term risk to Bund yields is likely still to the upside (owing to well-documented fiscal/issuance dynamics), lingering geopolitical uncertainty, shifting investor demand patterns (e.g. away from 30-year maturities and towards the 10-15-year segment) and the absence of a near-term hawkish ECB pivot may promote rangebound trading for now.

- Across the curve, German yields are down 1-2bps, with 2s10s flattening 0.5bps.

- Bund futures are +16 ticks at 127.85. Initial resistance is 128.03, followed by the more important 128.40 level (Jan 29 high).

- Germany sold E4bln of the 7-year 2.50% Nov-32 Bund this morning, while Belgium is holding a 30-year OLO syndication.

- 10-year EGB spreads to Bunds are mixed, with BTPs 1bp narrower at 60bps and OATs and RAGBs marginally wider.

- Eurozone flash January headline HICP was in line with consensus and MNI tracking at 1.69% Y/Y (vs 1.97% prior), while core softened to 2.19% Y/Y (vs 2.2% MNI consensus, 2.3% BBG consensus and 2.32% prior). Overall, it argues in favour of Chief Economist Lane’s expectation for a more sustainable composition of inflation in 2026 – it’s not likely to promote a meaningful ECB pivot at this stage.

- The Eurozone January composite PMI was revised down to 51.3 (vs 51.5 flash).

Figure 2: 10-year Bund Yields Since 2024

Source: Bloomberg Finance L.P

GILTS: Off Early Highs to Trade Little Changed, Bears in Technical Control

Gilts soften in recent trade, with Bunds away from highs ahead of German supply, countering the rally seen around the soft Spanish services PMI release.

- A modest downward revision to the final UK services PMI data had no tangible impact.

- Futures last -9 at 90.84 after filling yesterday’s gap lower during the early uptick.

- The bearish technical theme in the contract remains intact. Initial support and resistance of note located at last week’s low (90.48) and the 20-day EMA (91.35), respectively.

- Yields essentially flat on the day across the curve. 10s remain tethered to 4.50%.

- The ’25 closing high in 2s10s remains intact (81.63bp). The curve is less than 0.5bp off that level, a clean break above would expose the ’25 intraday high (84.58bp).

- Gilts ~2bp wider vs. Bunds this morning. A reminder that solid demand at yesterday’s gilt auction factored into outperformance for UK paper vs. Bunds on Tuesday.

- STIRs essentially flat, continuing to price around 1.5x BoE rate cuts for the remainder of the current cycle

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Feb-26 | 3.727 | +0.1 |

Mar-26 | 3.681 | -4.5 |

Apr-26 | 3.547 | -17.9 |

Jun-26 | 3.495 | -23.1 |

Jul-26 | 3.422 | -30.4 |

Sep-26 | 3.396 | -33.0 |

Nov-26 | 3.362 | -36.4 |

Dec-26 | 3.367 | -35.9 |

EQUITIES: This Week's Gain Reinforces Bullish EuroStoxx Theme

A bull cycle in Eurostoxx 50 futures remains intact and this week’s gains reinforce this theme. Key support lies at the 50-day EMA at 5863.24. A clear breach of this average would signal scope for a deeper retracement. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger at 6072.00, the Jan 14 / 15 high, has been pierced. A clear break would resume the primary uptrend. The trend in S&P E-Minis remains bullish. The recovery from Monday’s low suggests that a recent bear threat merely resulted in a short lived correction. Attention is on key resistance and the bull trigger at 7043.00, the Jan 28 high. A break of this level would confirm a resumption of the primary uptrend and open 7080.92, a Fibonacci projection. Key support and a bear trigger has been defined at 6814.50, the Jan 21 low.

- Japan's NIKKEI closed lower by 427.3 pts or -0.78% at 54293.36 and the TOPIX ended 9.74 pts higher or +0.27% at 3655.58.

- Elsewhere, in China the SHANGHAI closed higher by 34.465 pts or +0.85% at 4102.202 and the HANG SENG ended 12.55 pts higher or +0.05% at 26847.32.

- Across Europe, Germany's DAX trades lower by 38.11 pts or -0.15% at 24740.77, FTSE 100 higher by 95.62 pts or +0.93% at 10410.04, CAC 40 up 56.81 pts or +0.69% at 8236.31 and Euro Stoxx 50 up 0.88 pts or +0.01% at 5996.23.

- Dow Jones mini up 129 pts or +0.26% at 49481, S&P 500 mini up 6.25 pts or +0.09% at 6948.5, NASDAQ mini down 13 pts or -0.05% at 25440.75.

Time: 10:30 GMT (05:30 ET)

COMMODITIES: Gold Continues to Retrace Jan 29 - Feb 2 Sell Off

A bull cycle in WTI futures remains intact. However, Monday’s impulsive sell-off continues to highlight the beginning of a corrective phase. Attention is on support at the 20-day EMA, at $61.22. The 50-day EMA lies at $59.88. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. Gold has recovered from Monday’s low and is retracing the Jan 29 - Feb 2 sharp sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from last week’s high still highlights a potential top in the L/T trend and from a S/T perspective, marks an unwinding of the recent extreme overbought condition. A reversal lower would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude up $0.46 or +0.73% at $63.69

- Natural Gas down $0.01 or -0.21% at $3.304

- Gold spot up $109.7 or +2.22% at $5056.7

- Copper down $5.45 or -0.9% at $603.2

- Silver up $4.47 or +5.25% at $89.7014

- Platinum up $68.52 or +3.09% at $2285.41

Time: 10:30 GMT (05:30 ET)

US data appearing below is as originally scheduled. Due to the partial federal government shutdown, releases from agencies including the BLS and Department of Labor are subject to change.

| Date | GMT/Local | Impact | Country | Event |

| 04/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/02/2026 | 1315/0815 | *** | ADP Employment Report | |

| 04/02/2026 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 04/02/2026 | 1445/0945 | *** | S&P Global Composite & Services Index (f) | |

| 04/02/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 04/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 04/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 04/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/02/2026 | 1700/1200 | Richmond Fed's Tom Barkin | ||

| 04/02/2026 | 2330/1830 | Fed Governor Lisa Cook | ||

| 05/02/2026 | 0030/1130 | ** | Trade Balance | |

| 05/02/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 05/02/2026 | 0745/0845 | * | Industrial Production | |

| 05/02/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/02/2026 | 0900/1000 | * | Retail Sales | |

| 05/02/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/02/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 05/02/2026 | 1200/1200 | *** | Bank of England Interest Rate | |

| 05/02/2026 | 1230/1230 | BOE Press Conference | ||

| 05/02/2026 | 1315/1415 | *** | ECB Deposit Rate | |

| 05/02/2026 | 1315/1415 | *** | ECB Main Refi Rate | |

| 05/02/2026 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 05/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/02/2026 | 1345/1445 | ECB Press Conference | ||

| 05/02/2026 | 1400/1400 | *** | BOE Decision Making Panel | |

| 05/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 05/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/02/2026 | 1550/1050 | Atlanta Fed's Raphael Bostic | ||

| 05/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/02/2026 | 1725/1225 | BOC Governor Macklem Speech in Toronto, Release Time TBC | ||

| 05/02/2026 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/02/2026 | 2330/0830 | ** | Household spending |