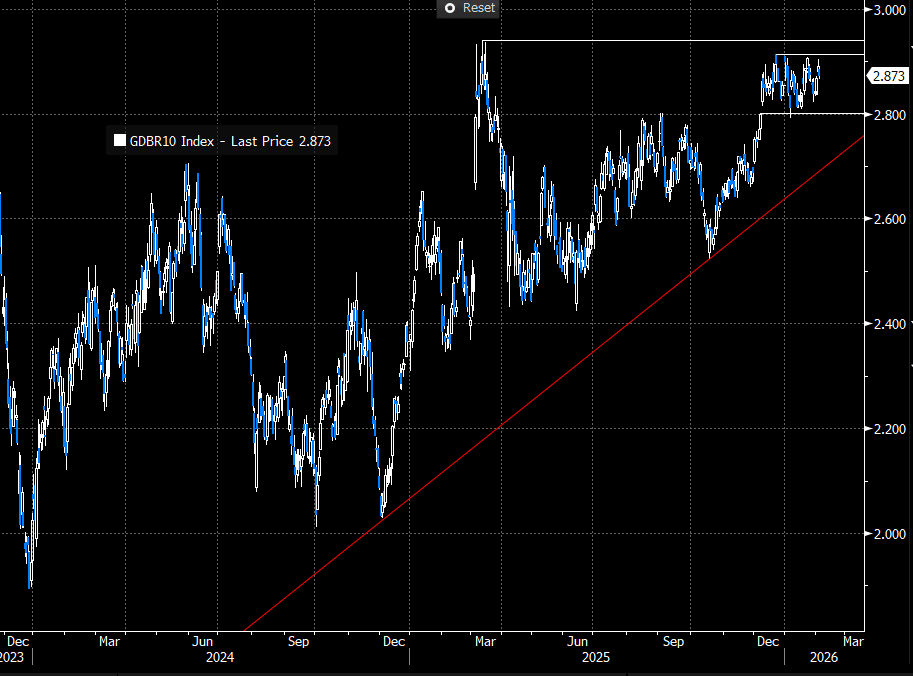

EGBS: 2.90% Again Contained Upside In 10-year Bund Yields Yesterday

10-year Bund yields were once again unable to sustain a move above 2.90% yesterday. Yields are back at 2.875% at typing. The key topside levels to watch remain 2.914% (Dec 22 high) and the more important 2.94% (March 2025 high). Although the medium-term risk to Bund yields is likely still to the upside (owing to well-documented fiscal/issuance dynamics), lingering geopolitical uncertainty, shifting investor demand patterns (e.g. away from 30-year maturities and towards the 10-15-year segment) and the absence of a near-term hawkish ECB pivot may promote rangebound trading for now.

- Across the curve, German yields are down 1-2bps, with 2s10s flattening 0.5bps.

- Bund futures are +16 ticks at 127.85. Initial resistance is 128.03, followed by the more important 128.40 level (Jan 29 high).

- Germany sold E4bln of the 7-year 2.50% Nov-32 Bund this morning, while Belgium is holding a 30-year OLO syndication.

- 10-year EGB spreads to Bunds are mixed, with BTPs 1bp narrower at 60bps and OATs and RAGBs marginally wider.

- Eurozone flash January headline HICP was in line with consensus and MNI tracking at 1.69% Y/Y (vs 1.97% prior), while core softened to 2.19% Y/Y (vs 2.2% MNI consensus, 2.3% BBG consensus and 2.32% prior). Overall, it argues in favour of Chief Economist Lane’s expectation for a more sustainable composition of inflation in 2026 – it’s not likely to promote a meaningful ECB pivot at this stage.

- The Eurozone January composite PMI was revised down to 51.3 (vs 51.5 flash).

Figure 1: 10-year Bund Yields Since 2024 (Source: Bloomberg Finance L.P)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Srangle seller

0RH6 97.56/98.06^^, sold at 3 in 5.5k.

EQUITY OPTIONS: Estoxx Call Spread

SX5E (16th Jan) 5850/5950cs, trades for 52.5 in 10k (suggest seller).

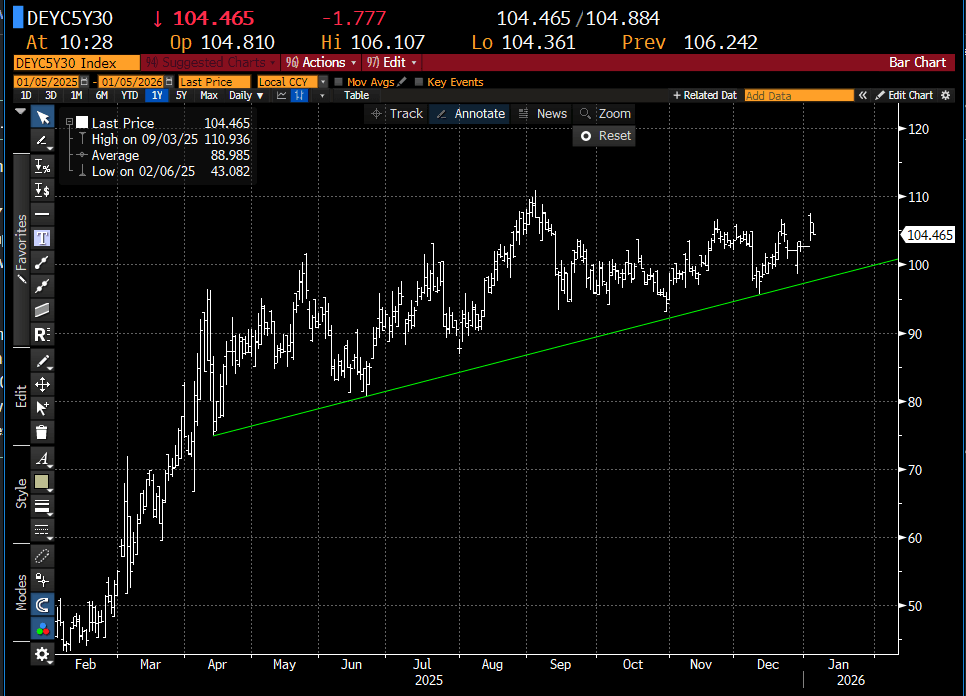

EGBS: Bunds Pare Early Gains, Trend Condition Bearish

- The trend condition in Bunds remains bearish, with futures having pared early morning gains. Currently +5 ticks at 127.16, support and the bear trigger in Bunds is located at 126.75.

- The move away from today’s 127.31 high may have been a function of solid corporate supply and an uptick in European equities. Crude oil futures have been volatile, with markets still digesting the implications of the US’ special operation in Venezuela over the weekend.

- The German curve is bull flatter, with 30-year yields down 2bps. That leaves 5s30s down almost 2bps to 104.5bps. However, trendline support drawn from the April 2025 low remains intact.

- Long-end swap spreads are little changed. One focus for EUR rates markets in H1 is the impact of Dutch pension fund flows, with several funds having transitioned to a defined contribution scheme from January 1.

- 10-year EGB spreads to Bunds have unwound earlier narrowing, now up to +1bp wider on the session.

- In supply, Slovenia is holding a 10-year syndication today, and we remain on the lookout for start-of-year mandates from several Eurozone countries. Conventional auction supply kicks off tomorrow with Germany.

- This afternoon’s calendar includes the US ISM manufacturing report, with regional focus on tomorrow’s December flash inflation data from France and Germany.

Figure 1: German 5s30s Curve (Source: Bloomberg Finance L.P)