MNI US OPEN - EU-US Talks Paused Pending Tariff Letter

EXECUTIVE SUMMARY:

- EU TARIFF LETTER COULD BE DELIVERED AS SOON AS TODAY

- TRUMP TO MAKE MAJOR RUSSIA STATEMENT ON MONDAY

- UK ECONOMY CONTRACTS FOR SECOND CONSECUTIVE MONTH

- CANADIAN UNEMPLOYMENT RATE EXPECTED TO TICK HIGHER TO 7.1%, COULD FACE 35% TARIFF

Figure 1: Energy Drives Upward Revision To French June Inflation

NEWS

EU-U.S. trade talks have ended for the moment pending an expected announcement by President Donald Trump later on Friday, EU sources said. One EU source said that Trade Commissioner Maros Sefcovic spoke with USTR Jamieson Greer Thursday afternoon Brussels time, only to be informed that "now all is in the hands of Trump." Trump subsequently publicly promised to "send a letter in a couple of hours", sources said, though whether this will be a definite deal or a temporary one remains unclear.

The U.S. will put a 35% tariff on imports from Canada effective Aug. 1, President Trump announced on Thursday evening. But an exemption for goods that comply with the nations’ free-trade agreement, the U.S.-Mexico-Canada Agreement, would still apply, a White House official said, stressing that could change.

US-RUSSIA (BBG): Trump Plans ‘Major’ Russia Statement Monday, Mulls Sanctions

President Donald Trump said he plans to make a “major statement” on Russia, as the US prepares to send more American weapons to Ukraine via purchases from NATO allies. “I think I’ll have a major statement to make on Russia on Monday,” Trump told NBC News in a telephone interview. He also said he expects the Senate to pass a tougher Russia sanctions bill sponsored by a close ally, Senator Lindsey Graham of South Carolina.

The Trump administration's immigration curbs are not having much aggregate impact in the U.S. job market, which continues to be solid, San Francisco Fed President Mary Daly told MNI on Thursday. "I don't see this right now as being a large threat to either the balance in the labor market or the potential run-up in wage inflation," she told a MNI Livestreamed Connect event.

ECB (BBG): ECB’s Schnabel Sees High Bar for Rate Cut With Economy Resilient

European Central Bank Executive Board member Isabel Schnabel said there’d have to be a major downward shift in inflation to justify another reduction in borrowing costs, dismissing concern that the economy is struggling. In remarks that represent some of the strongest opposition to extending the year-long easing campaign, Schnabel said interest rates are “in a good place,” with disinflation proceeding broadly as expected and the economy proving resilient to uncertainty.

ECB (BBG): ECB Must Cut More If Weak Growth Weighs on Prices, Panetta Says

The European Central Bank should lower interest rates further if economic expansion falls short of forecasts and drags down inflation excessively, according to Governing Council member Fabio Panetta. “If downside risks to growth were to strengthen disinflationary trends, it would be appropriate to continue with monetary easing,” the Italian central-bank chief said Friday in a speech.

The Reserve Bank of Australia needs to overhaul its communications, providing clearer estimates of the neutral rate and more transparent labour market models, to allow markets to better anticipate rate decisions by its new monetary policy board, a former senior official told MNI.

China’s steel rebar futures are likely to face further downward pressure in the second half of the year, as consumption remains weak amid insufficient stimulus and soft export demand, while planned production cuts may fall short of market expectations, local analysts told MNI. The October contract on the Shanghai Futures Exchange may fluctuate between CNY2,900-CNY3,150 per tonne in H2, likely rising initially on improved sentiment following authorities’ latest call for the withdrawal of obsolete production capacity and a seasonal rebound in coal prices, before softening on limited output reductions and a lack of demand support, said Zhuo Guiqiu, senior researcher at Jinrui Futures.

OIL (BBG): Saudis Surged Oil Output Far Above OPEC+ Quota in June, IEA Says

Saudi Arabia raised crude output far above its OPEC+ quota last month, joining other producers in a rush to export oil out of the Persian Gulf as Israel went to war with Iran, according to the International Energy Agency. The kingdom raised crude production by roughly 700,000 barrels a day to 9.8 million barrels a day, with about 70% of the additional supply exported, the IEA said in its monthly report. It was a rare breach of agreed OPEC+ limits by Riyadh, which has repeatedly scolded other members for over-production.

HONG KONG (BBG): Hong Kong Defends FX Peg for Fourth Time in Two Weeks

Hong Kong authorities intervened for the fourth time in two weeks to prevent the city’s currency from weakening beyond its official trading band, after previous efforts failed to drain enough liquidity to push up funding costs. The Hong Kong Monetary Authority, the Chinese financial hub’s de-facto central bank, purchased HK$13.3 billion ($1.7 billion) of the local dollar, according to its Bloomberg page on Friday. The HKMA’s three previous rounds of currency defense had cost it a total of HK$59 billion, according to Bloomberg’s calculations of official data.

The UK economy contracted for a second consecutive month in May, preliminary data published by the Office For National Statistics showed Friday, although officials highlighted an upward revision to growth in March. GDP is estimated to have fallen by 0.1% in May 2025, following an unrevised fall of 0.3% in April and upwardly revised growth of 0.4% in March. Real GDP is estimated to have grown by 0.5% in the three months to May, compared with the three months to February, largely driven by growth in the services sector in this period.

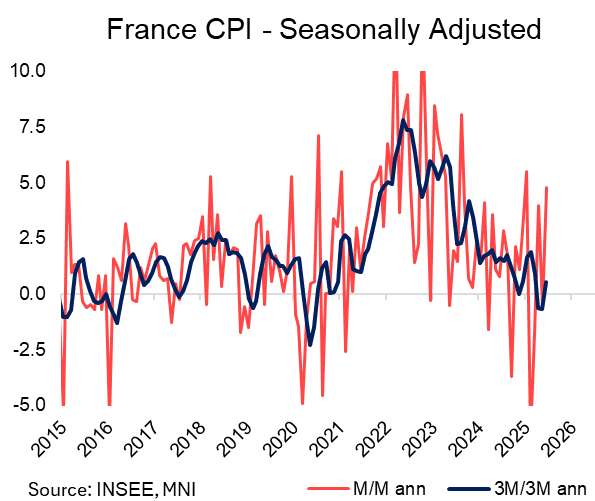

EUROPEAN INFLATION: Energy Drives Upward Revision To French June Inflation

French final June HICP was a tenth above the flash release on a rounded basis, but actually was only revised 4 hundredths higher to 0.86% Y/Y (vs 0.82% flash, 0.59% prior). Still, it’s worth remembering that the initial consensus ahead of the flash release was 0.7% Y/Y, so it’s a decent upward surprise all told. Energy drove the upward revision versus the flash release.

- Headline CPI was also revised a touch higher to 0.97% Y/Y (vs 0.93% flash, 0.66% prior).

- On a seasonally adjusted basis using INSEE data, CPI rose 0.39% M/M, above May’s -0.05% and April’s 0.32%. 3m/3m SA CPI growth rose 0.55% (VS -0.66% prior), though it’s too early to suggest the broader downtrend that began in late 2022 has ended.

- Core inflation (excluding energy and unprocessed foods) ticked up to 1.2% Y/Y (vs 1.1% prior).

FOREX: CAD Volatility in Focus Ahead of Canadian Jobs Report

- European ranges for G10 FX have been relatively contained in comparison to the punchy moves during the APAC session. The USD index is rising once again, extending its cautious recovery from last week’s cycle lows to ~1.5%. The DXY is again testing above initial 20-day EMA resistance, of which a weekly close above would mark a bullish development.

- One of the key moves overnight was for the Canadian dollar following President Trump’s latest letter to Prime Minister Mark Carney. The announcement that Canada will face a 35% tariff on exports to the United States starting August 1 prompted a rapid spike for USDCAD, from levels around 1.3655 to an intra-day peak of 1.3731. Spot has since settled around the 1.37 mark, but the volatility provides an interesting dynamic ahead of today’s release of Canadian employment data for June, the highlight on the global calendar..

- Elsewhere, USDJPY is outperforming Friday following a consistent 100 pip grind higher overnight to match the weekly highs at 147.18 underpinning a short-term bull cycle that remains in play. The latest recovery has resulted in a breach of the 50-day EMA, highlighting a stronger reversal which will target a move back towards 148.03, the Jun 23 high. Higher US yields have been supportive of the move.

- In similar vein, GBP and NZD are notable underperformers on the session, both declining ~0.4%. For GBPUSD, spot is approaching the lowest levels of the week at 1.3526 following a soft May GDP print and weaker-than-expected industrial production figures. The market will concentrate on key 50-day EMA support which intersects today at 1.3481 and below here, a key trendline drawn from the January lows comes in just above the 1.34 mark.

- AUDNZD (+0.15%) continues its upswing above the May peak to trade at fresh 3-month highs. A sustained break would signal scope for a move back to the early April highs just above the 1.10 mark, being assisted by the Aussie outperformance in the aftermath of the hawkish RBA surprise this week.

EGBS: Bund Futures Narrowing Gap To Key Support

Bund futures are narrowing the gap to key support at 128.97 (May 14 low), currently down 30 ticks today at 129.15 on decent volumes. There hasn’t been a discernible headline trigger for today’s selloff in Bunds, but this week’s bias has clearly been tilted to the downside.

- In yield terms, desks will look to target the 2.75% level in the 10-year Bund (currently +2.6bps at 2.73%).

- The light data calendar has allowed markets to focus on medium-term German/EU fiscal impulses, with the German curve bear steepening. 10s30s is up 0.4bps today at 50bps, extending this week’s steepening to 4bps.

- Characteristically hawkish comments from ECB’s Schnabel will have kept the pressure on the EGB complex, but intraday curve steepening suggests this has not been the primary driver.

- 10-year EGB spreads to Bunds are biased slightly tighter, but still within 1bp of yesterday’s close. 3/7/15-year BTP supply was digested smoothly.

- French June final HICP inflation was revised a tenth higher on a rounded basis, but this was driven by energy and not a market mover.

- Overnight, US President Trump surprised markets with a 35% tariff on Canada and signalled that a letter to the EU will be coming today. With the President now seemingly eyeing blanket tariffs of 15-20%, it seems the previous 10% reciprocal levy will be a best-case scenario for the EU.

Gilts are lower but within this week’s ranges, with a modest mark higher in final French CPI data, a reaffirmation of ECB Executive Board member Schnabel’s hawkish stance and ongoing discussions surrounding the UK’s fiscal fragility applying some weight.

- No real insulation from the softer-than-expected domestic GDP M/M data, 10s vs. Bunds essentially flat at ~189bp.

- A reminder that upward revisions to March data left the 3m/3m GDP measure above consensus, limiting any dovish move.

- Our macro team noted that overall, there's not a lot in the data to drive market reaction.

- Gilt futures trade as low as 91.67.

- Bears remain in technical control, initial support and resistance at 91.42/92.19, respectively.

- Yields 2.0-3.5bp higher, curve steeper.

- 2s10s and 5s30s remain below multi-week highs registered earlier in the week.

- GBP STIRs flat to a little more hawkish on the day.

- ~51.5bp of BoE cuts priced through Dec, with over 80% odds of the next 25bp cut priced through August and such a move more than fully discounted through September.

- SONIA futures +0.5 to -2.0, strip twist steepens.

- Little of note on the UK calendar for the remainder of the day, leaving focus on macro/cross-market cues.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.004 | -21.3 |

Sep-25 | 3.945 | -27.2 |

Nov-25 | 3.780 | -43.7 |

Dec-25 | 3.702 | -51.5 |

Feb-26 | 3.575 | -64.2 |

Mar-26 | 3.544 | -67.3 |

EQUITIES: US Futures Pressure Alltime Highs Despite Incoming Trade Letters

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract is trading at its recent highs. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. Eurostoxx 50 futures have traded higher this week as the contract extends the recovery that started Jun 23. This exposed key resistance and the bull trigger at 5486.00, the May 20 high.

- Japan's NIKKEI closed lower by 76.68 pts or -0.19% at 39569.68 and the TOPIX ended 10.9 pts higher or +0.39% at 2823.24.

- Elsewhere, in China the SHANGHAI closed higher by 0.495 pts or +0.01% at 3510.177 and the HANG SENG ended 111.2 pts higher or +0.46% at 24139.57.

- Across Europe, Germany's DAX trades lower by 186.25 pts or -0.76% at 24267.15, FTSE 100 lower by 17.31 pts or -0.19% at 8958.1, CAC 40 down 51.24 pts or -0.65% at 7851.83 and EuroStoxx 50 down 44.27 pts or -0.81% at 5394.

- Dow Jones mini down 250 pts or -0.56% at 44651, S&P 500 mini down 33.25 pts or -0.53% at 6290.5, NASDAQ mini down 116.25 pts or -0.51% at 22895.

COMMODITIES: WTI Crude Futures Steady After Thursday Drift

Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5. WTI futures maintain a bearish tone following the reversal from the Jun 23 high, and recent gains appear corrective. Support to watch is the 50-day EMA, at $65.27. The average has been pierced, a clear break of it would signal scope for a deeper retracement.

- WTI Crude up $0.29 or +0.44% at $66.84

- Natural Gas up $0.01 or +0.15% at $3.339

- Gold spot up $16.02 or +0.48% at $3341.61

- Copper down $5.45 or -0.97% at $552.85

- Silver up $0.47 or +1.27% at $37.4755

- Platinum down $1.61 or -0.12% at $1362.78

| Date | GMT/Local | Impact | Country | Event |

| 11/07/2025 | 1130/1330 | ECB Cipollone At Ukraine Recovery Conference | ||

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1230/0830 | * | Building Permits | |

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1800/1400 | ** | Treasury Budget |