MNI US OPEN - ECB Widely Expected to Leave Key Rates on Hold

EXECUTIVE SUMMARY

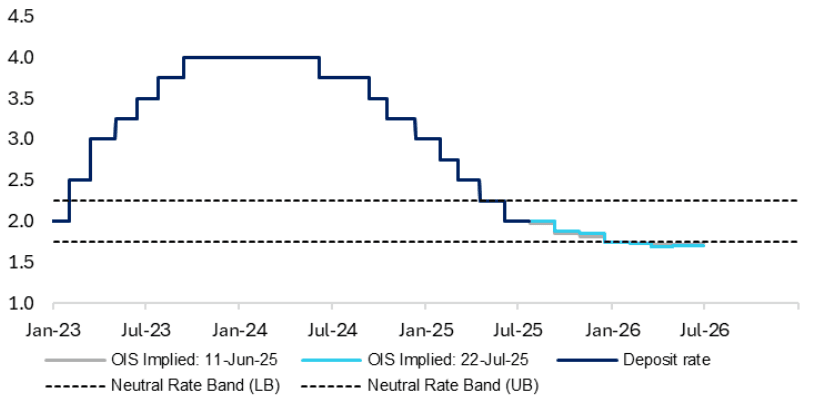

- MNI ECB PREVIEW - SEE YOU IN SEPTEMBER

- TRUMP SAYS COUNTRIES WILL FACE TARIFFS RANGING FROM 15% TO 50%

- UK-INDIA TRADE DEAL TO BE SIGNED BY KEIR STARMER AND NARENDRA MODI

- 36-MONTH HIGH FOR GERMAN MANUFACTURING PMI

Figure 1: ECB deposit rates and implied rates

Source: MNI/Bloomberg Finance L.P.

NEWS

MNI ECB PREVIEW - JULY 2025: See You in September

The ECB is fully expected to leave its three key rates on hold on Thursday, with its deposit rate at 2.00%. ECB President Lagarde last month signalled that policy was in a good place after a cut to the mid-point of neutral estimates of 1.75-2.25%. There haven’t been any significant data surprises in the intervening period and some Governing Council members have talked of a higher bar to cut rates.

US (BBG): Trump Says Countries Will Face Tariffs Ranging From 15% to 50%

US President Donald Trump suggested that he would not go below 15% as he sets so-called reciprocal tariff rates ahead of an Aug. 1 deadline, an indication that the floor for the increased levies was rising. “We’ll have a straight, simple tariff of anywhere between 15% and 50%,” Trump said Wednesday at an AI summit in Washington. “A couple of — we have 50 because we haven’t been getting along with those countries too well.”

US (FT): Donald Trump to Visit Federal Reserve After Attacking $2.5bn Renovation

Donald Trump will visit the US Federal Reserve on Thursday as the president looks to ratchet up pressure on its chair Jay Powell to cut interest rates more aggressively. The president will spend roughly an hour at the central bank, according to his schedule, which was released late on Wednesday. The unusual move is the latest salvo from the president as he looks to strong-arm Powell into lowering borrowing costs by 3 percentage points and intensifies an attack over the cost of building renovations. The Fed declined to comment on the visit. The White House did not respond to a request for comment.

US/S.KOREA (BBG): Bessent Set to Miss Key US-South Korea Trade Talks This Week

A high-level trade meeting between South Korea and the US this week has been postponed after Treasury Secretary Scott Bessent became unavailable due to a scheduling conflict, South Korea’s Finance Ministry said Thursday. The so-called “2+2” dialogue, originally scheduled for Friday, was expected to bring together top finance and trade officials from both nations, involving Bessent, US Trade Representative Jamieson Greer, South Korea’s Finance Minister Koo Yun-cheol and Trade Minister Yeo Han-koo.

US/AUSTRALIA (BBG): Australia to Lift Import Curbs on US Beef to Pacify Trump

Australia intends to remove restrictions on US beef imports in a bid to appease President Donald Trump, who had highlighted Canberra’s biosecurity measures as an unfair impediment to trade. Agriculture Minister Julie Collins said the Australian government will lift restrictions from next week on the import of red meat that originates in either Canada or Mexico and is later slaughtered in the US. Australia barred US beef imports in 2003 following an outbreak of mad cow disease, and only eased some restrictions in 2019.

UK/INDIA (FT): UK-India Trade Deal to Be Signed by Keir Starmer and Narendra Modi

UK Prime Minister Sir Keir Starmer and Narendra Modi, India’s prime minister, will on Thursday sign a trade deal between the two countries that London believes will boost British exports to India by 60 per cent by 2040. The agreement, first announced in May, means tariffs on more than 90 per cent of UK exports to India will be cut, with the largest reductions on cosmetics, clothes and food and drink — albeit phased in over a decade. Ministers said the deal was expected to eventually benefit the UK economy by £4.8bn a year.

EU/CHINA (MNI): China and EU Must Rebalance - von der Leyen

MNI (Beijing) The EU and China must rebalance bilateral relations to ensure mutual benefit, European Commission President von der Leyen told China’s President Xi during opening remarks at a meeting in Beijing on Thursday, the commission's press office announced. “As our cooperation has deepened, so have the imbalances. We have reached an inflection point,” von der Leyen added, noting that the EU is China's largest trading partner and China is the EU's third.

EU/CHINA (MNI): China Calls for Trade Cooperation With EU - Xinhua

MNI (Beijing) Chinese President Xi Jinping has called on the EU to keep its trade and investment markets open to Chinese enterprises and stressed the need for further cooperation in green and digital partnerships, Xinhua News Agency said on Thursday. Meeting with President António Costa of the European Council and President Ursula von der Leyen of the European Commission, Xi said the EU should restrain the use of restrictive economic and trade tools and provide a good business environment for Chinese firms, noting Beijing was willing to enhance coordination with the EU on climate change and the global green transition.

RBA (BBG): RBA’s Bullock Supports Measured, Gradual Approach to Easing

The Australian central bank’s interest rate-setting board judges that a “measured and gradual” approach to policy easing is appropriate, Governor Michele Bullock said, adding that labor demand remains strong while core inflation is easing gradually. The combination of “low” unemployment and recent strong jobs growth is “remarkable and very welcome,” Bullock said in a speech in Sydney on Thursday. Her comments came a week after data showed Australia’s jobless rate unexpectedly climbed to a four-year high of 4.3% in June as hiring all-but stalled.

RBNZ (MNI): Tariffs to Dampen Medium Term Inflation, RBNZ Ready to Act - Conway

RBNZ Chief Economist Pail Conway has delivered a speech earlier today in Wellington NZ. It focused on the impact of tariffs. Some key snippets from the speech are outlined below. The key take away from a monetary policy standpoint is that Conway reiterated the recent monetary policy stance: "As outlined in the July Monetary Policy Review, the Committee sees scope to lower the OCR further if medium-term inflation pressures continue to ease as projected, Mr Conway says."

MNI CBRT PREVIEW - JULY 2025: Restarting the Easing Cycle

Adjustments to the CBRT’s policy statement in June indicated that policy easing will resume from July onward – which is the prevailing view shared among sell-side analysts. The median surveyed estimate looks for a 250bp cut to the one-week repo rate to 43.50%, although there are some calls for an even bolder move. Softer-than-expected headline CPI in June is supportive of renewed easing, however, ongoing political uncertainty and recent tweaks to tax rates on TRY deposits should prompt the CBRT to approach its cutting cycle with caution.

THAILAND/CAMBODIA (NYT): Thailand Says 12 Killed in Border Clashes With Cambodia

A monthslong standoff between Cambodia and Thailand turned into a deadly exchange of fire along their contested border on Thursday that killed at least 11 civilians and a soldier, according to Thai officials. Both nations accused the other of striking first, in the worst hostilities between the Southeast Asian neighbors in more than a decade. The Thai army said that Cambodia had fired rockets into civilian areas in four Thai provinces, prompting Thailand to send F-16 fighter jets to strike targets in Cambodia and ordering the evacuation of border areas.

DATA

EUROZONE DATA (MNI): EZ Services PMI Strength Driven by ex-France/Germany

- EUROZONE JULY FLASH MANUF PMI 49.8 (49.8 FCAST, 49.5 PRIOR)

The Eurozone-wide July flash composite PMI reached its highest level in 11 months at 51.0, above the 50.7 consensus and 50.6 prior. The "rest of the Eurozone" (ex-France and Germany) appears to have driven the strength, particularly in the services sector. While not necessarily pushing back on expectations for one more 25bp ECB cut this cycle, signs of a continued gradual recovery in EZ activity suggests a deposit rate below 1.75% may not be warranted just yet.

GERMANY DATA (MNI): 36-Month High for Manufacturing PMI

- GERMANY FLASH JULY MANUF PMI 49.2 (49.5 FCAST, 49.0 PRIOR)

The German flash July composite PMI was slightly weaker-than-expected at 50.3 (vs 50.7 cons, 50.4 prior). This was due to the manufacturing component printing at 49.2 (vs 49.5 cons, 49.0 prior), with services broadly in line at 50.1 (vs 50.0 cons, 49.7 prior). Despite remaining below the neutral 50 handle, the manufacturing PMI still reached a 36-month high, with new orders consolidating June's notable rise. However, the excerpts on employment and prices will still screen as dovish for the ECB, at least with respect to the near-term outlook.

GERMANY DATA (MNI): August Consumer Confidence Soft Ahead of Next Week's Hard Data

- GERMANY GFK CONSUMER CLIMATE AUG -21.5 (JUL -20.3)

August GfK consumer confidence comes in below consensus at -21.5 (cons -19.3), down from July's -20.3, against analyst estimates of a recovery. Both the decrease in willingness to buy (-9.2 points vs -6.2 prior) and the continuing increase in willingness to save (16.4 points, highest since February 2024, vs 13.9 prior) drive the Consumer Climate metric's second consecutive fall. The press release notes that "the majority of consumers still consider it ,advisable to hold back", due to general uncertainty, desire for preparedness, and high prices, especially for food.

FRANCE DATA (MNI): Flash Composite PMI Highest Since Aug, But Details Weak

- FRANCE JULY FLASH MANUF PMI 48.4 (48.5 FCAST, 48.1 PRIOR)

Although the French manufacturing and services July flash PMIs were within 0.1 point of consensus estimates, the composite reading was five tenths stronger than expected at 49.6 (49.1). This seems to be due to some inconsistencies with analyst forecast entries - the median services/manufacturing estimates were unchanged even when considering only those that submitted forecasts for the composite reading. Abstracting from this, the data shows a partial rebound in manufacturing sentiment to 48.4 (vs 48.4 cons, 48.1 prior), with services little changed at 49.7 (vs 49.6 cons and prior).

FRANCE JUL MANUF SENTIMENT AT 96 (MNI)

UK DATA (MNI): PMI Keeps Weakening Labour Market in Focus

- UK JULY FLASH MANUF PMI 48.2 (48.0 FCAST, 47.7 PRIOR)

Weaker-than-expected July flash PMI (composite 51.0 vs 51.8 cons, 52.0 prior) driven by the services sector (51.2 vs 52.9 cons, 52.8 prior), which saw a sharp fall in new orders and reduction in employment. Worth noting however that the services print remains above May's 50.9 reading. The manufacturing PMI was 48.2 (vs 48.0 cons, 47.7 prior), with the underlying details also quite disappointing, particularly with respect to new export orders.

JAPAN DATA (MNI): July PMIs Mixed, Manufacturing Back Into Contraction, Services Rise

Japan preliminary July PMIs were mixed. notably manufacturing fell to 48.8 from 50.1 in June. Services rose though to 53.5 from 51.7. This left the composite index at 51.5, unchanged from the June read. For manufacturing the index back in contraction territory but still above recent lows (48.4 from March this year). In terms of the detail, output slumped to 47.6 from 51.2 in June. New orders were also down June levels.

FOREX: GBP/AUD Slips on Contrasting PMIs

- AUD is once again top of G10 FX Thursday, continuing to benefit from the buoyant price action for major equity indices, greater optimism surrounding China and the resumption of dollar weakness this week. Additionally, the July flash composite PMI rose to 53.6 from 51.6 in June, representing the highest reading since April 2022 and offsetting concerns following the weaker-than-expected labour market report last week. RBA Governor Bullock stated in overnight remarks that the labour market has eased only gradually and the rise in the unemployment rate was not a shock for the central bank. She confirmed a measured, gradual approach to policy is appropriate.

- Meanwhile, the weaker-than-expected services PMI in the UK weighs moderately on sterling after the release, prompting a brief test back below 1.3550 for GBPUSD, currently down 0.2% on the session. The renewed dollar weakness this week has allowed cable to recover well from recent pullback lows, negating the prior break below trendline support, drawn from the January lows.

- This keeps more of a focus on EURGBP, which has risen back above 0.8680 and narrows in on a cluster of daily highs across July, just below the 0.8700 handle. A break through here would place the focus on key resistance at 0.8738, the Apr 11 high. A dominant uptrend remains in place for the cross.

- The ECB rate decision takes focus going forward. President Lagarde last month signaled that policy was in a good place after a cut to the mid-point of neutral estimates of 1.75-2.25% - and given there haven't been any significant data surprises in the intervening period and some Governing Council members have talked of a higher bar to cut rates. We expect today’s communication to be as non-committal as possible, maintaining flexibility and buying time for a fresh forecast round in time for the Sep 11 meeting.

- Canadian retail sales, weekly US jobless claims and the prelim US PMI numbers are the data highlights Thursday. The Fed remain inside their pre-meeting media blackout period.

EGBS: Bund Futures Off Lows, But Consolidating Yesterday's Selloff

Although off session lows at typing, Bund futures have broadly consolidated yesterday afternoon’s sharp selloff, which came amid reports of a nearing trade deal between the EU and the US. Monday’s low of 129.73 was pierced earlier this morning, but a pullback in European equity futures has helped futures back to 129.96 (-62 ticks today). A clear breach of 129.73 would be a bearish development and expose the July 14 low at 129.08.

- First reported by the FT, the supposed deal would reduce US tariffs on EU goods to 15%, similar to what was agreed with Japan earlier this week. Note that in subsequent comments, US’ Navarro suggested reports should be taken with a “grain of salt”. However, this hasn’t materially changed the tone for markets.

- There was limited impact from the July flash PMIs. The Eurozone-wide July flash composite PMI reached its highest level in 11 months at 51.0, above the 50.7 consensus and 50.6 prior. However, some of the details were still weak. Overall, the report feels consistent with market expectations for one more 25bp this cycle.

- German yields are 1-2.5bps higher, with the curve lightly bear flattening. The multi-month range (loosely 2.40-2.75%) in German 10s remains intact, benchmark last 2.662%.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s levels, with early tightening fading as alongside equity futures.

- Focus turns to today’s ECB decision at 1315BST. We expect the communication to be as non-committal as possible, maintaining flexibility and buying time for a fresh forecast round at the Sep 11 meeting.

GILTS: Holding Away from Lows After PMIs, Curve Steeper

Gilts hold off lows after the softer-than-expected flash services PMI data allowed the space to move further away from lows in the wake of some pre-data stabilisation.

- Early extension of yesterday’s late move lower followed hopes surrounding reduced EU-U.S. tariff rates.

- Initial support in futures (91.29) held to the tick, with a subsequent recovery to ~91.55.

- Note that bears remain in technical control. Any extension lower would expose the bear trigger at the July 18 low (91.08).

- Yields little 0.5-2bp lower, curve bull steepens.

- 2s10s last 76.5bp. a reminder that the 80bp provided meaningful resistance earlier this month.

- 5s30s move towards 145bp, next upside level of interest located at the ’25 intraday high (147.2bp).

- SONIA futures recovered from lows alongside gilts, last +0.5 to -2.0.

- BoE-dated OIS still shows over 90% odds of a cut for August, with just under 50bp of easing priced through year end.

- The labour market component of the PMIs read dovishly, particularly in light of BoE Governor Bailey’s recent dovish warnings surrounding that area of the economy.

- Little of note on the UK economic calendar through the reminder of the day, leaving focus on cross-market and macro cues, with a particular interest on the language deployed at the latest ECB decision (no change in rates almost universally expected).

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.992 | -22.5 |

Sep-25 | 3.947 | -27.0 |

Nov-25 | 3.789 | -42.8 |

Dec-25 | 3.727 | -49.0 |

Feb-26 | 3.613 | -60.5 |

Mar-26 | 3.580 | -63.7 |

EQUITIES: Eurostoxx 50 Futures Narrow Gap to Key Resistance and Bull Trigger

The trend condition in Eurostoxx 50 futures remains bullish and recent weakness appears to have been a correction. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. Sights are on key resistance and bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00. S&P E-Minis have once again traded to a fresh cycle high this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. With the 6400.00 handle cleared, sights are on 6439.88, a Fibonacci projection. Key support is at the 50-day EMA, at 6131.47. Support at the 20-day EMA is at 6277.23.

- Japan's NIKKEI closed higher by 655.02 pts or +1.59% at 41826.34 and the TOPIX ended 51.17 pts higher or +1.75% at 2977.55.

- Elsewhere, in China the SHANGHAI closed higher by 23.429 pts or +0.65% at 3605.727 and the HANG SENG ended 129.11 pts higher or +0.51% at 25667.18.

- Across Europe, Germany's DAX trades higher by 232.17 pts or +0.96% at 24473.93, FTSE 100 higher by 76.9 pts or +0.85% at 9138.41, CAC 40 up 21.66 pts or +0.28% at 7870.86 and Euro Stoxx 50 up 36.05 pts or +0.67% at 5380.3.

- Dow Jones mini down 139 pts or -0.31% at 45075, S&P 500 mini up 4.25 pts or +0.07% at 6400.5, NASDAQ mini up 76 pts or +0.33% at 23386.75.

Time: 10:00 BST

COMMODITIES: Recent Pullback for Gold Considered Corrective

A bearish theme in WTI futures remains intact and the recovery since Jun 24 still appears corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.70. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. On the upside, Initial resistance to monitor is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range. A bull cycle in Gold that started Jun 30 remains intact, and the latest pullback is - for now - considered corrective. Resistance at $3395.1, the Jun 23 high, has been cleared. A continuation higher would open $3451.3, the Jun 16 high. Note that moving average studies are in a bull-mode position highlighting a dominant uptrend. The bear trigger is $3248.7, the Jun 30 low. An initial firm support to watch is 3282.8, the Jul 9 low.

- WTI Crude up $0.77 or +1.18% at $66.03

- Natural Gas up $0.02 or +0.72% at $3.099

- Gold spot down $17.29 or -0.51% at $3369.61

- Copper up $8.5 or +1.46% at $589.85

- Silver down $0.17 or -0.44% at $39.0898

- Platinum down $35.18 or -2.47% at $1386.86

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 24/07/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/07/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 24/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1245/1445 | ECB Press Conference | ||

| 24/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/07/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/07/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/07/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 25/07/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/07/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/07/2025 | 0600/0800 | ** | PPI | |

| 25/07/2025 | 0600/0800 | ** | Unemployment | |

| 25/07/2025 | 0600/0700 | *** | Retail Sales | |

| 25/07/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/07/2025 | 0800/1000 | ** | M3 | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 25/07/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/07/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |