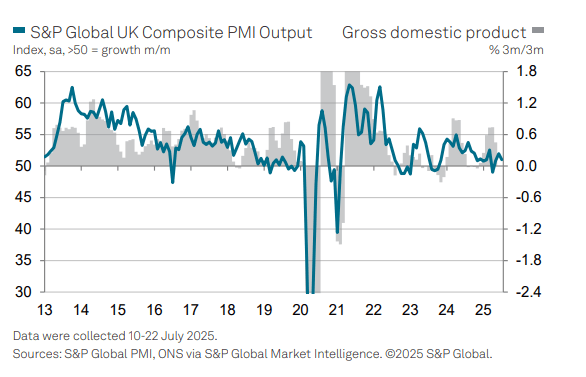

UK DATA: Jul Flash PMI: Keeps Weakening Labour Market In Focus

Weaker-than-expected July flash PMI (composite 51.0 vs 51.8 cons, 52.0 prior) driven by the services sector (51.2 vs 52.9 cons, 52.8 prior), which saw a sharp fall in new orders and reduction in employment. Worth noting however that the services print remains above May’s 50.9 reading.

The manufacturing PMI was 48.2 (vs 48.0 cons, 47.7 prior), with the underlying details also quite disappointing, particularly with respect to new export orders.

Overall, the survey will keep concerns around the weakening labour market at the fore. However, an uptick in input cost and output charge inflation will complicate the readthrough for the BOE.

Key notes from the release:

- “Output growth was driven by the service economy in July, with some survey respondents commenting on an uptick in consumer spending”….“Manufacturing production meanwhile stabilised in July, which ended an eight-month period of contraction. Goods producers nonetheless widely commented on challenging business conditions, especially in major export markets as US tariffs resulted in delayed spending decisions”.

- “July data indicated a renewed decline in total new work received by UK private sector firms, following a marginal rise in the previous survey period. This was driven by the sharpest fall in new orders across the service economy since April”.

- “Lower volumes of new work contributed to a reduction in private sector employment for the tenth consecutive month during July”

- “Average cost burdens increased sharply across the private sector economy, with the overall rate of input price inflation accelerating from June' s six-month low”.

- “Meanwhile, prices charged by private sector businesses increased at a robust pace in July…. This was driven by a faster increase in selling prices at service providers”.

- “Looking ahead, private sector firms on balance continue to anticipate a rise in business activity during the next 12 months. The degree of confidence edged up since June, but remained subdued in comparison to the post-pandemic trend”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: USDJPY tests 145.00, Cable targets 1.3600

- The Yen is extending gains against the USD and the EUR, the GBP and the Aussie are lagging for now.

- The USDJPY is testing just below the 145.00 figure, but is finding some underlying demand here.

- Immediate support comes at 144.80 20-day EMA.

- Cable is edging back towards the 1.3600 handle, and the next resistance will be eyed at 1.3632 High Jun 13 and the bull trigger.

SWAPS: German ASWs Off Lows After DFA Funding Plan

The lack of upside surprise in the German issuance plan, with over half the move being allocated to the 7-Year introduction, means that long end German ASWs see a bit of a relief rally.

- Spreads vs. 3-month Euribor are still 0.5-1.0bp are still lower on the day, with the front end under the most pressure.

- This is presumably on initial reaction to the Iran-Israel ceasefire developments (spreads didn’t rally after news of an Iranian missile launch/promises of Israeli retaliation) and interplay between lower oil and ECB pricing.

SWEDEN: Government 2025 GDP Projections More Pessimistic Than Riksbank

The Swedish Government has released its updated macroecnomic projections:

- 2025 GDP growth is seen at 0.9%, down from 1.8% in the May projections and 2.1% in April. The Riksbank is more optimistic, expecting 1.7% 2025 growth in the June MPR projections.

- 2026 GDP growth is expected at 2.6%, up from 2.3% in May but down from 2.8% in April. The Riksbank expected 2.4% in the June MPR.

From the press release:

- "The economic recovery is expected to accelerate in 2026, as GDP growth is expected to be higher, driven by increased household consumption and an increased rate of investment. The Ministry of Finance's new forecast is that the recession will persist until 2027, and thus be more prolonged than the assessment made in the spring budget bill in April".

- "Unemployment is high in Sweden, and demand for labor remains weak. Employment appears to have started to turn around at the beginning of the year, but general uncertainty about the economic situation is expected to dampen this development in the near future. A gradual recovery in the labor market is expected to begin in 2025 but especially gain momentum in 2026.