MNI US OPEN - ECB Poised for 25bp Rate Cut, Unanimity in Focus

EXECUTIVE SUMMARY

- MNI ECB PREVIEW - THE LAST CONSECUTIVE CUT?

- KASHKARI SAYS FED WELL POSITIONED TO WAIT FOR TARIFF IMPACT

- ECONOMISTS RAISE QUESTIONS ABOUT QUALITY OF U.S. INFLATION DATA

- JAPANESE REAL WAGES STAY NEGATIVE FOR FOURTH CONSECUTIVE MONTH

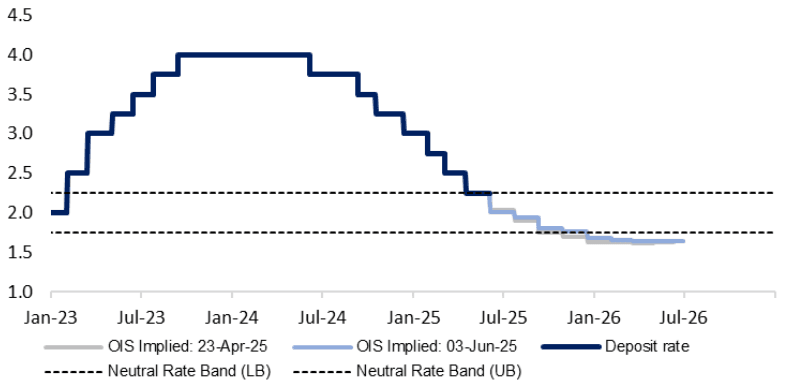

Figure 1: ECB deposit rate and OIS implied rates

Source: MNI/Bloomberg

NEWS

MNI ECB PREVIEW - JUNE 2025: The Last Consecutive Cut?

The ECB is fully expected to cut its three key rates by 25bp this week, taking its deposit rate to 2.00%. That would be the mid-point of the neutral estimated range of 1.75-2.25% according to ECB staff, although senior ECB leadership including Lagarde last meeting have been keen to downplay neutral discussions when faced with significant shocks. Nearing the perceived end of the easing cycle, focus will be on any clues around the willingness or lack thereof to highlight a potential pause in July. A July cut is only about 25% priced, perhaps vulnerable to dovish surprises.

FED (BBG): Kashkari Says Fed Well Positioned to Wait for Tariff Impact

Federal Reserve Bank of Minneapolis President Neel Kashkari said the US central bank is well positioned to wait and see how tariff policies impact the economy before adjusting interest rates. “The economy is seeming like it’s pretty resilient so far, and so for me right now is the time to get data, see how the tariff negotiations shake out before we reach any firm conclusions about the direction of interest rates,” Kashkari said Wednesday in an interview on CNN. Kashkari said a pullback in business investment amid tariff uncertainty is an overhang for the US economy. “The longer it goes on, the bigger negative effect it has,” Kashkari said.

FED (MNI): Senate Confirms Bowman as New Fed VC for Regulation

The U.S. Senate Wednesday confirmed Federal Reserve Governor Michelle Bowman as the central bank's new vice chair for supervision in a narrow 48-46 vote along party lines with six abstentions. Bowman will now play a crucial role as the Fed's leading supervisor, helping to direct everything from setting rules for how major banks operate to monitoring risks across the financial system to ensure a safe and stable environment.

US (WSJ): Economists Raise Questions About Quality of U.S. Inflation Data

Some economists are beginning to question the accuracy of recent U.S. inflation data after the federal government said staffing shortages hampered its ability to conduct a massive monthly survey. The Bureau of Labor Statistics, the office that publishes the inflation rate, told outside economists this week that a hiring freeze at the agency was forcing the survey to cut back on the number of businesses where it checks prices. In last month’s inflation report, which examined prices in April, government statisticians had to use a less precise method for guessing price changes more extensively than they did in the past. Economists say the staffing shortage raises questions about the quality of recent and upcoming inflation reports.

US (WaPo): Trump Administration Reinstates and Expands Travel Ban

President Donald Trump on Wednesday restricted the entry of travelers to the United States from more than a dozen countries, resurrecting and expanding sweeping restrictions from his first term that are expected to draw swift legal challenges. The presidential proclamation, slated to go into effect June 9, fully restricts the entry of individuals from Afghanistan, Myanmar, Chad, Republic of Congo, Equatorial Guinea, Eritrea, Haiti, Iran, Libya, Somalia, Sudan and Yemen. It also partially restricts the entry of travelers from Burundi, Cuba, Laos, Sierra Leone, Togo, Turkmenistan and Venezuela.

US (WSJ): Trump Is Losing Patience With Musk’s Outbursts Over Megabill

A senior White House official said Trump wasn’t happy about Musk’s decision to lambaste his signature legislation, describing the president as confused as to why the Tesla chief executive decided to ratchet up his criticism after working so closely with the president for four months. The official said senior Trump advisers were caught off guard by Musk’s latest offensive.

US/UKRAINE (WSJ): U.S. Is Redirecting Critical Antidrone Technology From Ukraine to U.S. Forces

The Trump administration is redirecting a key antidrone technology earmarked for Ukraine to American forces, a move that reflects the Pentagon’s waning commitment to Kyiv’s defense. The Pentagon quietly notified Congress last week that special fuzes for rockets that Ukraine uses to shoot down Russian drones are now being allocated to U.S. Air Force units in the Middle East.

US/JAPAN (BBG): Japan to Seek Tariff Review in Latest Negotiations Ahead of G-7

Japan will stick to its stance of seeking a review of all US tariffs in what could be the final ministerial-level talks ahead of a leaders’ summit this month, the nation’s top trade negotiator Ryosei Akazawa said. “Japan will continue to strongly urge the US to reconsider its series of tariff measures,” Akazawa said Thursday in Tokyo as he left for Washington. He added that he’s not sure which US officials will meet him for the fifth round of trade negotiations. Akazawa is set to return to Japan on Sunday, about a week before the Group of Seven gathering convenes in Canada.

NATO (MNI): Def Mins Meeting Underway as Members Face Up to US’ 5% Spending Demands

The final NATO defence ministers' meeting before the alliance's leaders' summit later in June is underway in Brussels. Opening the meeting, Secretary General Mark Rutte said, "To make NATO a stronger, a fairer and a more lethal alliance, we need to spend more to reach these targets. But for today, the main focus is on the targets, and then, of course, the summit will decide on the spending." Speaking alongside Rutte earlier, Hegseth laid out a hard line on spending from the US, saying, "We're here to continue the work that President Trump started, which is a commitment to 5% [of GDP equivalent] defence spending across this alliance, which we think will happen. It has to happen by the summit at The Hague later this month."

BOE (MNI): DMP Leans Dovish, But Not Enough to Materially Impact BOE Outlook

BOE May DMP here. While the forward looking responses around inflation and wage growth lean dovish, it doesn't seem enough to materially change the outlook for the BOE. The SONIA Dec '25 future has gained one tick since the data was released, now +1.5 ticks today at 96.24. The questions around the impact of US tariffs are also not too surprising, with the UK known to be more insulated from the trade war than the likes of the EU - more so given the recent trade agreement made with the US.

UK (FT): UK to Unveil Pension Reform Aimed At Boosting Retirement Savings

Ministers will unveil a sweeping overhaul of Britain’s pensions system on Thursday aimed at unpicking problems created by previous rules and boosting the retirement savings of millions of people. The pensions bill will cover six areas of reform and include a “reserve” power to force pension schemes to invest more in the UK if they fail to meet a voluntary commitment. One of the most notable features of the bill — announced in the King’s Speech last July and the first since 2021 — will be the merging of defined contribution pension pots worth £1,000 or less into one scheme.

RUSSIA/N.KOREA (BBG): Kim Vows Full Backing for Putin as Ties With Russia Deepen

North Korean leader Kim Jong Un reiterated his pledge to unconditionally support Russian President Vladimir Putin, state media said, as the sanctions-defying alliance between the two countries raises security concerns in the region. In a meeting with a top security aide to Putin, Sergei Shoigu, in Pyongyang, Kim said North Korea will “unconditionally support” Russia and “its foreign policies in all the crucial international political issues,” the official Korean Central News Agency reported on Thursday.

DATA

EUROZONE DATA (MNI): April PPI Weakness Driven by Energy But Softer Elsewhere Too

- EUROZONE APR PPI -2.2% M/M, +0.7% Y/Y

Eurozone PPI inflation was softer than expected in April, at 0.7% Y/Y (1.1% consensus) after 1.9% in March for its softest Y/Y rate since December. Energy drove the lower print, falling 7.7% M/M for -0.3% Y/Y after 4.0% Y/Y in March. That said, PPI ex-energy also eased to 1.1% Y/Y after 1.3% in March, for also the lowest since December. Across the non-energy categories, Y/Y rates tapered off across intermediate, capital and durable consumer goods, which are all sitting at their lowest since December. Further downside momentum here would be eyed against the backdrop of potential re-routing of Chinese goods towards Europe amid a firmer US tariff stance.

UK DATA (MNI): ONS Identifies Error With April Y/Y Inflation Data

From the ONS: "An error has been identified in the Vehicle Excise Duty (VED) data provided to the ONS by the Department for Transport, which is used to calculate consumer prices inflation. The incorrect data overstate the number of vehicles subject to Vehicle Excise Duty (VED) rates applicable in the first year of registration. This has the effect of overstating the headline Consumer Price Inflation (CPI) and Retail Prices Index (RPI) annual rates by 0.1 percentage points for the year to April 2025 only. No other periods are affected. In line with our consumer prices revisions policy, these statistics will not be amended. However, we are reviewing our quality assurance processes for external data sources in light of this issue.

UK MAY FINAL CONSTRUCTION PMI 47.9 (46.6 APRIL) (MNI)

SWEDEN DATA (MNI): Softer-Than-Expected May Flash Inflation Keeps June Cut on Cards

- SWEDEN FLASH MAY CPIF +2.3% Y/Y

The slightly softer-than-expected May flash CPIF-ex energy reading (2.47% Y/Y vs 2.6% cons, 2.68% Riksbank March MPR) was worth about 10 pips of upside in NOKSEK, which has already partially been pared. As always, no details are provided in the flash release. It certainly keeps a June cut on the cards, and supports the Riksbank's view that the Q1 acceleration in inflationary pressures was likely temporary. We think the Riksbank's June 10 Business Survey (alongside the final CPIF report on June 13) will be most important for the Executive Board ahead of the June 18 decision.

SWISS MAY UNEMPLOYMENT RATE +2.9% (MNI)

JAPAN DATA (MNI): Japanese Real Wages Stay Negative in April

Japan’s inflation-adjusted real wages fell 1.8% in April from a year earlier, marking the fourth consecutive month in negative territory, unchanged from March’s pace and 20 basis points below expectations, preliminary data from the Ministry of Health, Labour and Welfare showed Thursday. Bank of Japan officials expect real wages to remain negative for now, as consumer prices stay elevated due to ongoing cost pass-through. However, they anticipate a gradual narrowing of the negative gap from April onward, helped by strong nominal wage gains following this year’s spring wage negotiations. Nominal wages rose 2.3% y/y in April, unchanged from March, while scheduled earnings increased 2.2%, up from 1.4%.

AUSTRALIA DATA (MNI): Softer Exports But Capex Imports Up, Surplus Within Recent Range

- AUSTRALIA APR TRADE BALANCE A$+5413

The April merchandise trade surplus narrowed $1.5bn to $5.4bn but remained above the Q1 average and in line with the levels seen since the end of the post-Covid rebound. There was some payback in the month for the strong increase in March exports, while imports rose at their highest monthly rate since December.

FOREX: EUR Trades the Range Headed into ECB

- The single currency is rangebound ahead of the ECB meeting, with EUR/USD holding the late rally Wednesday to consolidate above 1.1400. For EUR/GBP, the price remains inside the broad downtrend drawn off the mid-April highs, however S/T momentum has stalled slightly, with the price gravitating toward the 100-dma.

- The JPY is softer against all others in G10 as the USD/JPY rate mean reverts. EUR/JPY continues to trade just above the 50-dma of 162.63, a key level of support that should remain in focus into the ECB decision. Meanwhile, the trend structure in GBPUSD is unchanged, it remains bullish and the pair continues to trade closer to its recent highs. Initial support to watch lies at 1.3431, the 20-day EMA.

- The carry profile across G10 remains a key driver as low levels of vol pervade across spot markets. This continues to favour the relative high yielders in G10 FX, namely AUD and NZD which are higher intraday, and aiding AUD/USD toward recent cycle highs at 0.6537.

- The ECB rate decision takes focus going forward, and anything other than a 25bps rate cut to all three major rates would be a surprise for markets. Focus for the press conference will be on the unanimity (or lack thereof) of the governing council toward their decision on rates, particularly as the benchmark deposit heads toward the midpoint of the bank's assessment of 'neutral'.

EGBS: European Yields Reverse Lower; Supply Digested Smoothly

European yields have reversed lower over the last 90 minutes, with 10-year maturities generally leading the rally. That sees the German 2s10s curve turn 2bps flatter on the session at 70.5bps. The 70bp handle has contained downside in the spread since the start of April. German 10s30s is 0.5bps steeper at 47bps.

- There hasn’t been an obvious headline trigger for the reversal in yields, which likely accounts for the smooth passing of Spanish/French supply and possible pre-positioning ahead of this afternoon’s ECB decision.

- A 25bp ECB cut is unanimously expected and fully priced. The market reaction will likely hinge on the balance of risks and updated economic forecasts, with the few clear signals expected in the policy statement.

- Short-end Spanish supply saw decent results, while LT OAT supply was also digested smoothly. There was still some evidence of softening long-end demand though, with the 3.75% May-56 OAT bid-to-cover ratio quite a bit below the April re-opening (2.29x vs 2.82x prior), despite a smaller amount being sold.

- Bund futures are +39 ticks at 131.28, up from an earlier session low of 130.79 and testing resistance at the June 3 high. The next topside target is 131.50 (May 7 high).

- BTPs outperform Bunds, with futures up +45 ticks at 121.20. The 10-year BTP/Bund spread has tightened another 1bp to a new multi-year low of 95bps.

- German April factory orders were stronger-than-expected at 0.6% M/M (vs -1.5% prior), while April PPI was soft.

GILTS: Futures Through Next Resistance Cluster

Gilts rally alongside EGBs, with solid to strong demand at this morning’s French & Spanish bond auctions driving the move.

- Upticks in crude oil & European equity futures, as well as the presence of the aforementioned EGB supply, weighed early today.

- Futures trade through yesterday’s highs to 92.45.

- A cluster of resistance levels in the contact have been pierced, presenting a stronger reversal.

- Next upside level of note located at Fibonacci resistance (92.79).

- Yields are 3-4bp lower, 30s outperform.

- 10s last 4.57%, still above long-term uptrend support drawn off the Dec ’21 low (4.504% today).

- 2s10s consolidates the close below 60bp, while 5s30s prints below 120bp for the first time since mid-April.

- Dovish move in GBP STIRs alongside the rally in gilts.

- BoE-dated OIS shows 16.5bp of cuts through August, 21bp through September, 36bp through November and 43.5bp through year-end. Contracts little changed to 2bp more dovish on the day.

- SONIA futures flat to +4.5. Implied terminal policy rate pricing on the strip has moved to 3.56%, ~22bp off May’s hawkish extreme.

- The ONS revealing that it overstated April Y/Y CPI by 0.1ppt seemingly fed into a dovish move at the open, with long end swings driving things since.

- No comments of note seen from BoE’s Greene & Breeden.

- The UK calendar is thin for the remainder of the day, which should leave focus on broader macro drivers.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.214 | +0.2 |

Aug-25 | 4.048 | -16.4 |

Sep-25 | 3.999 | -21.2 |

Nov-25 | 3.852 | -35.9 |

Dec-25 | 3.776 | -43.5 |

Feb-26 | 3.667 | -54.4 |

Mar-26 | 3.647 | -56.4 |

EQUITIES: Trend Cycle in Eurostoxx 50 Futures Unchanged and Bullish

The trend cycle in Eurostoxx 50 futures is unchanged, it remains bullish and a recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5268.58, the 50-day EMA. A clear break of this average is required to signal a possible reversal. The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract is trading just ahead of its recent high. A print above 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. An extension would open 6057.00 next, the Mar 3 high. Key support lies at 5774.07, the 50-day EMA.

- Japan's NIKKEI closed lower by 192.96 pts or -0.51% at 37554.49 and the TOPIX ended 28.66 pts lower or -1.03% at 2756.47.

- Elsewhere, in China the SHANGHAI closed higher by 7.895 pts or +0.23% at 3384.098 and the HANG SENG ended 252.94 pts higher or +1.07% at 23906.97.

- Across Europe, Germany's DAX trades higher by 97.12 pts or +0.4% at 24373.43, FTSE 100 higher by 7.56 pts or +0.09% at 8808.85, CAC 40 up 25.43 pts or +0.33% at 7830.1 and Euro Stoxx 50 up 20.37 pts or +0.38% at 5425.52.

- Dow Jones mini up 90 pts or +0.21% at 42590, S&P 500 mini up 11 pts or +0.18% at 5992, NASDAQ mini up 52.25 pts or +0.24% at 21818.75.

Time: 09:55 BST

COMMODITIES: WTI Futures Bear Threat Remains Present

WTI futures continue to trade closer to their recent highs. A bear threat remains present and the recovery since Apr 9 still appears corrective. A key resistance area to monitor is $62.52, the 50-day EMA. It has again been pierced. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. A bullish theme in Gold remains intact and recent gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Sights are on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, key support and the bear trigger to watch has been defined at $3121.0, the May 15 low.

- WTI Crude up $0.19 or +0.3% at $63.05

- Natural Gas down $0.03 or -0.81% at $3.686

- Gold spot up $3.84 or +0.11% at $3376.14

- Copper up $4.55 or +0.93% at $493.2

- Silver up $0.33 or +0.97% at $34.8194

- Platinum up $29.24 or +2.67% at $1123.08

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech | ||

| 06/06/2025 | 2330/0830 | ** | Household spending | |

| 06/06/2025 | 0600/0800 | ** | Trade Balance | |

| 06/06/2025 | 0600/0800 | ** | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Foreign Trade | |

| 06/06/2025 | 0830/1030 | ECB Lagarde Video Message For CIBP Anniv | ||

| 06/06/2025 | 0900/1100 | ** | Retail Sales | |

| 06/06/2025 | 0900/1100 | *** | GDP (final) | |

| 06/06/2025 | 0900/1100 | * | Employment | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1900/1500 | * | Consumer Credit |