MNI US OPEN - Downside Surprise to UK CPI Broad-Based

EXECUTIVE SUMMARY

- GOOLSBEE SAYS FED SHOULD BE ABLE TO CUT RATES FURTHER IN 2026

- TRUMP ORDERS BLOCKADE OF SANCTIONED OIL TANKERS IN VENEZUELA

- US READIES NEW RUSSIA SANCTIONS IF PUTIN REJECTS PEACE DEAL: BBG

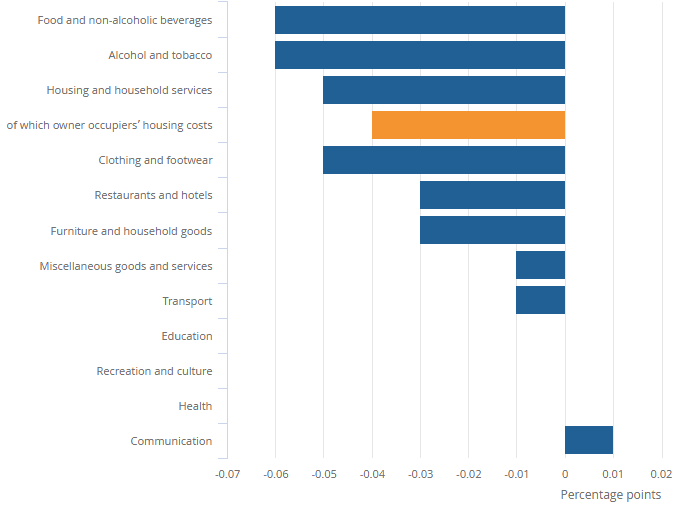

- BROAD-BASED DOWNSIDE SURPRISES ACROSS UK CPI

- CHINA CHIPMAKER METAX JUMPS 693% AFTER SIGNIFICANTLY OVERSUBSCRIBED IPO

Figure 1: Contributions to change in UK CPIH annual inflation rate

Source: ONS

MNI PREVIEWS

MNI US CPI PREVIEW: Handle With Care

The latest delayed CPI update from the Bureau of Labor Statistics threatens to be messy in several regards, muddying the signal for markets and for monetary policy. The government shutdown precluded October data collection, meaning overall CPI aggregates will not be available for the month, and the inflation recorded for November is on a 2-month change basis from Sept. While the M/M data will never be officially available, MNI's usual aggregation of sell-side analyst expectations points to expectations of an average of 0.24% M/M core CPI monthly across October and November.

MNI ECB PREVIEW: Relative Resilience Confirms in a Good Place

The ECB is again fully expected to leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff. This time though the meeting comes against a backdrop of a very mild hiking bias to end-2026, helped by recent rhetoric from Schnabel, which despite having been pared fairly notably in recent days is still a change from a modest easing bias ahead of recent meetings.

MNI BOJ PREVIEW: Hike Fully Priced

The BOJ is widely expected to raise the policy rate by 25bp to 0.75% at the December 18–19 meeting, with Governor Ueda’s recent remarks signalling increased confidence in the outlook for growth, inflation and wage momentum. Ueda has indicated the BOJ will assess the “pros and cons of raising the policy interest rate,” while Policy Board members say conditions for a hike are “gradually falling into place,” though confirmation of spring wage momentum remains key.

MNI NORGES BANK PREVIEW: Dovish Revisions, No Commitment

Norges Bank is unanimously expected to hold the policy rate at 4% on Thursday, in a quarterly decision which includes an updated MPR and rate path projection. The rate path will be the primary focus for markets, and we expect a downward revision relative to September. The downward revision we anticipate may shift the balance of risks in favour of 2x25bp cuts next year, versus the single cut embedded in the September rate path.

MNI RIKSBANK PREVIEW: No Policy Pivot Yet

The Riksbank is expected to hold the policy rate at 1.75% on Thursday, in a quarterly decision which includes an updated MPR and rate path projection. We expect the policy statement to re-iterate that the policy rate will be kept at 1.75% for “some time”. The main focus should be on the first three quarters of the updated rate path. This is the part of the curve that is “owned” by the Executive Board, and therefore constitutes a policy signal (beyond that is a staff forecast).

MNI BANXICO PREVIEW: Cut Seen, Hawkish Risks Prevalent

Banxico is expected to deliver another 25bp rate cut to 7.0% on Thursday as it continues to respond to weak activity data, which revealed a contraction of the economy in the third quarter. However, recent stronger-than-expected CPI inflation data have significantly increased the risk of a pause in the easing cycle, if not this week, then more likely early in the new year, keeping focus on the forward guidance.

MNI CNB PREVIEW: Repo Rate to End 2025 at 3.50%

The Czech National Bank will almost certainly deliver a well-telegraphed unanimous decision to keep the two-week reference rate unchanged at 3.50% at the final meeting of this year as concerns about familiar inflationary risks continue to linger. Although headline inflation moderated to +2.1% Y/Y in November, the property market is running hot, wages are still growing at pace, and there is considerable uncertainty about the fiscal outlook under the new government.

NEWS

FED (BBG): Goolsbee Says Fed Should Be Able to Cut Rates Further in 2026

Federal Reserve Bank of Chicago President Austan Goolsbee says he expects strong growth in 2026, and that interest rates should be able to fall further if that happens. “As we go into 2026, I’m still pretty optimistic that the economy will sustain at a stabilized rate that’s pretty decent, and if it can do that and inflation is headed down to something like 2%, I think rates can go down,” Goolsbee says Tuesday in an interview on CNN.

US/VENEZUELA (BBG): Trump Orders Blockade of Sanctioned Oil Tankers in Venezuela

President Donald Trump ordered a blockade of sanctioned oil tankers going into and leaving Venezuela, ratcheting up pressure on Caracas as the US builds up its military presence in the region. “Venezuela is completely surrounded by the largest Armada ever assembled in the History of South America,” Trump wrote on social media Tuesday. “It will only get bigger, and the shock to them will be like nothing they have ever seen before.” The move threatens to choke off the economic lifeblood of a country that was already under severe financial pressure. But it will have a less profound impact on global markets due to the diminished status of Venezuela’s oil industry.

US/RUSSIA (BBG): US Readies New Russia Sanctions If Putin Rejects Peace Deal

The US is preparing a fresh round of sanctions on Russia’s energy sector to increase the pressure on Moscow should President Vladimir Putin reject a peace agreement with Ukraine, according to people familiar with the matter. The US is considering options, such as targeting vessels in Russia’s so-called shadow fleet of tankers used to transport Moscow’s oil, as well as traders who facilitate the transactions, said the people who spoke on condition of anonymity to discuss private deliberations. The new measures could be unveiled as early as this week, some of the people said.

US (WSJ): Warner Is Preparing to Tell Shareholders to Reject Paramount Offer

Warner Bros. Discovery is preparing to tell its shareholders to reject Paramount’s latest offer as soon as Wednesday, people familiar with the matter say, and plans to recommend they support its existing deal with Netflix instead. That would leave Paramount and its chief executive, David Ellison, to decide whether to sweeten its offer.

GERMANY (MNI): Government Enacts Commission on Second Pension Reform

The German government today is enacting a commission to come up with suggestions for additional pension reform. Scope is in particular to put under review the retirement age, private pension options, and the question of whether other groups, such as civil servants, should contribute to the pay-as-you-go statutory scheme according to media reports. Results are to be published by mid-2026. This follows German labour minister Bas (SPD) floating earlier this month to change the pension system to map the pension age to the number of contribution years.

CHINA (BBG): China Chipmaker MetaX Jumps 693% After Wildly Oversubscribed IPO

MetaX Integrated Circuits Shanghai Co. soared in its first day of trading on Wednesday, the latest outsized debut by a Chinese chipmaker after similar gains by Moore Threads Technology Co. earlier this month. MetaX surged 693% in Shanghai after raising $585.8 million in an initial public offering. The gains made it the top performing debut for IPOs between $500 million and $1 billion in China over the past decade. Like Moore Threads, MetaX makes graphics processing units for artificial intelligence developers — a red-hot industry that’s growing at a rapid clip as consumers and businesses adopt AI services.

CHINA (BBG): Vanke to Meet With Insurers, Banks in Shenzhen as Crisis Deepens

China Vanke Co., once the nation’s biggest homebuilder and now at the epicenter of the years-long property crisis, is set to meet in Shenzhen with some insurance firms and commercial banks on Wednesday, people familiar with the matter said. The gathering will take place in the afternoon and it’s unclear what Vanke is going to discuss with them, according to the people, who asked not to be identified. Insurers have been among investors who have held private debt in Vanke, which has delayed interest payments on some of those borrowings previously.

THAILAND (BBG): Thailand Cuts Rate as Currency Surge Adds to Growth Headwind

The Bank of Thailand cut its key interest rate to the lowest since 2022 to bolster a fragile economy weighed down by a stubbornly strong currency and renewed political uncertainty, while leaving the door open for more easing. The central bank’s Monetary Policy Committee voted unanimously Wednesday to cut the one-day repurchase rate by 25 basis points to 1.25%, the fifth cut in 14 months. The move was predicted by 23 of 24 economists surveyed by Bloomberg. Only one forecast no change.

INDONESIA (BBG): Indonesia Holds Rate as Exodus of Foreign Funds Sinks Rupiah

Bank Indonesia held its benchmark interest rate at its last meeting for the year to head off pressure on the rupiah amid persistent foreign capital outflows. The central bank also offered more incentives for banks to ramp up lending, as past rate cuts fail to make their way through Southeast Asia’s largest economy. The BI-Rate was kept at 4.75% on Wednesday as forecast by 22 of 35 economists in a Bloomberg survey. The rest expected a quarter-point rate cut.

INDIA (BBG): India Rupee Roars Back on RBI’s Support, Up Most in Seven Months

India’s central bank stepped in forcefully to support the rupee, propelling it to the biggest gain in seven months in a move that some analysts said was intended to punish those betting on a one-way slide in the currency. The rupee rose as much as 1%, the most since May 23, to 90.0963 on Wednesday, after closing at a record low in the previous session. The Reserve Bank of India is intervening through dollar sales in the local market, according to people familiar with the transactions.

DATA

EUROPEAN INFLATION (MNI): Package Holidays Behind Higher Services HICP in November

- EUROZONE NOV HICP 2.1% Y/Y (2.2% FLASH, 2.1% OCT)

- EUROZONE NOV CORE HICP 2.4% Y/Y (2.4% FLASH, 2.4% OCT)

- EUROZONE NOV SERVICES HICP 3.5% Y/Y (3.5% FLASH, 3.4% OCT)

Looking into the details of the final November Eurozone HICP print, all in Y/Y terms: The services increase to 3.47% (3.46% flash, 3.36% Oct) was due to (often volatile) package holidays, which accelerated to 4.42% after October's 0.91%, something that had been suspected after flash data but couldn't be fully confirmed until today's release. Accommodation HICP was also higher than before, at 3.41% (3.14% Oct) whilst airfares dropped after national data was unclear on the extent to which October strength had unwound (-2.74% Nov vs 1.66% Oct).

UK DATA (MNI): Broad-Based Downside Surprises Across UK CPI

- UK NOV CPI 3.25% Y/Y (MNI MED 3.5%, BOE 3.41%, OCT 3.56%)

- UK NOV CORE CPI 3.18% Y/Y (MED 3.4%, OCT 3.38%)

- UK NOV SERVICES CPI 4.39% Y/Y (MED 4.53%, BOE 4.5%, OCT 4.49%)

Downside surprises from services, core goods and food inflation all behind the UK CPI miss. Core goods the big downside driver here - so it may be an early Black Friday sales driver helping here. Clothing as well as furniture and household goods look soft at first. Within services, accommodation looks soft at -0.95% Y/Y (+0.82% Y/Y in Oct) as well as cultural services. This looks like a pretty soft print across the board and seems to very much reinforce the expectation that we will see a cut tomorrow. One question now is will there be enough in this data to convince any additional "hawkish" member in addition to Bailey to support a cut here. The market is very much looking for 5-4 so a 6-3 vote tomorrow would be a surprise (5-4 remains our base case, however).

UK DATA (MNI): Brightmine Pay Deals Fall Back to 3.0%, Continued Stability Seen Ahead

- UK SEP-NOV BRIGHTMINE MEDIAN PAY AWARDS +3.0% (VS +3.3% AUG-OCT)

Brightmine median pay awards for the three months to November fell back to 3.0% from 3.3% in September. Most pay awards this year are lower than in 2024, and pay freezes are more common. Brightmine's outlook for 2026 points to continued stability around the 3% level seen ahead, with potential downward pressures from high costs and national insurance contributions. The Sep-Nov data highlights that 65% of pay deals are below those agreed for the same employees in 2024. Also, almost all pay deals in this period sat between 2.0% and 4.2% (except for freezes).

GERMANY DATA (MNI): Broad-Based Decline for the Last IFO Survey of the Year

- GERMANY DEC IFO BUSINESS CLIMATE INDEX 87.6

Contrary to expectations, Germany's IFO Business Climate Index fell for the second consecutive time in December, to 87.6 (88.2 consensus, 88.0 prior). The expectations component was the driver behind the deterioration, falling to 89.7, the joint lowest reading since May (90.5 cons; 90.5 prior), while the current assessment was little changed this time (85.6 vs 85.8 cons; 85.6 prior). This lets the gap between the two readings decline (but of course in the "wrong" direction) after expectations outperformed earlier this year.

MNI CHINA MONEY MARKET INDEX: Modest Rate Cuts Seen in 2026

- MNI CHINA MONEY MKT INDEX DEC LQDTY OUTLOOK 47.0 VS NOV 51.0

MNI (Beijing) Chinese interbank money market traders expect only limited further central bank cuts to the policy rate and reserve requirements in 2026 as policy focus moves to addressing economic structural issues, while ample liquidity will be maintained to ensure market stability, MNI’s China Money Market Index indicated on Wednesday. The next-six-month policy outlook sub-index showed less expectations for further easing, with only 52.0% of traders seeing additional policy moves, the lowest this year though above the 50% threshold and taking the index to 24.0, the highest in 2025.

JAPAN DATA (MNI): Nov Exports Rise, Despite Auto Drop

- JAPAN NOV EXPORTS +6.1% Y/Y; OCT +3.6%

Japan’s exports rose for a third straight month in November, up 6.1% year on year following a 3.6% increase in October, driven by stronger shipments of semiconductors and medical products, although automobile exports declined, Ministry of Finance data released Wednesday showed. The data are unlikely to immediately prompt the Bank of Japan to revise its assessment that exports have remained more or less flat as a trend. Automobile exports fell 4.1% in November, the first decline in two months, following a 0.4% increase in October.

JAPAN DATA (MNI): BOJ Nov Real Export Index to Rise 6.6% M/M

The Bank of Japan’s real export index calculated using Ministry of Finance trade data rose 6.6% m/m in November for the first rise in two months following a 3.7% decline in October, data released by the BOJ showed on Wednesday. The figures were calculated by MNI based on BOJ data and confirmed by bank officials. The BOJ will release details of the index on Monday. The average of the index for the October-November period rose 1.4% from the previous quarter for the first rise in three quarters following -1.4% for the third quarter.

JAPAN DATA (MNI): Japan Household Financial Assets at Record High at End-Sept

The balance of financial assets held by Japanese households rose to a record JPY2,286 trillion at the end of September, up 4.9% year on year for an 11th consecutive quarterly increase, preliminary flow of funds data released by the Bank of Japan on Wednesday showed. A BOJ official told reporters that rising stock prices and the weak yen were the main drivers behind the increase in household financial assets. The balance of cash and deposits held by households stood at JPY1,122 trillion at the end of September, up 0.5% from a year earlier, indicating that households remained cautious about sharply increasing exposure to risk assets.

NEW ZEALAND DATA (MNI): Q3 Current Account Deficit, as % of GDP, Continues Improvement

The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. In seasonally adjusted terms we were slightly wider in Q3 at -NZD3.8bn. As a percent of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve, we were at -9.0% of GDP at the end of 2022.

FOREX: UK CPI Pressures GBP Ahead of BOE Decision, DXY Extends Bounce

- The US dollar trades with a much more constructive tone on Wednesday, prompting a near 0.8% recovery for the DXY from the post-NFP lows. It appears the limited market shift in rates expectations has frustrated the weakening dollar trend into the release, with short-term positions potentially getting squeezed ahead of tomorrow’s US CPI release.

- Lower-than-expected UK CPI has weighed on GBP, pressuring cable down to 1.1312 session lows. It’s not pricing for tomorrow's BoE decision that’s shifting spot markets, but policy differentials further down the curve. With tomorrow’s BOE rate cut well priced, the vote split will be in focus. Today’s inflation print could potentially tilt that to 6-3 – a dovish signal that could usher in easier pricing still for next year as the committee would look more proactive on downside inflation surprises.

- For GBPUSD, support sits at 1.3290, the 50-day EMA. A breach of this EMA would highlight a bearish development and signal a possible reversal. To the upside, attention is on 1.3452 (pierced), a Fibonacci retracement. In EURGBP, 0.8802-10 could provide intraday resistance, but a close above this mark today would open gains toward November’s 0.8865 high.

- USDJPY stands a notable 110 pips above yesterday’s lows at 155.50. Spot traded to within 5 pips of the Dec 05 lows of 154.35 yesterday, bolstering the significance of this area of support ahead of the US data and the BOJ on Friday. Furthermore, the 50-day EMA has also held, intersecting just above the 154.00 handle. A clear breach of this average is required to undermine the bull theme and signal scope for a deeper corrective pullback.

- Weekly MBA mortgage applications and September housing starts highlight the US data calendar before focus turns to tomorrow's central banks, with the Riskbank, Norges Bank, BOE and ECB decisions all due.

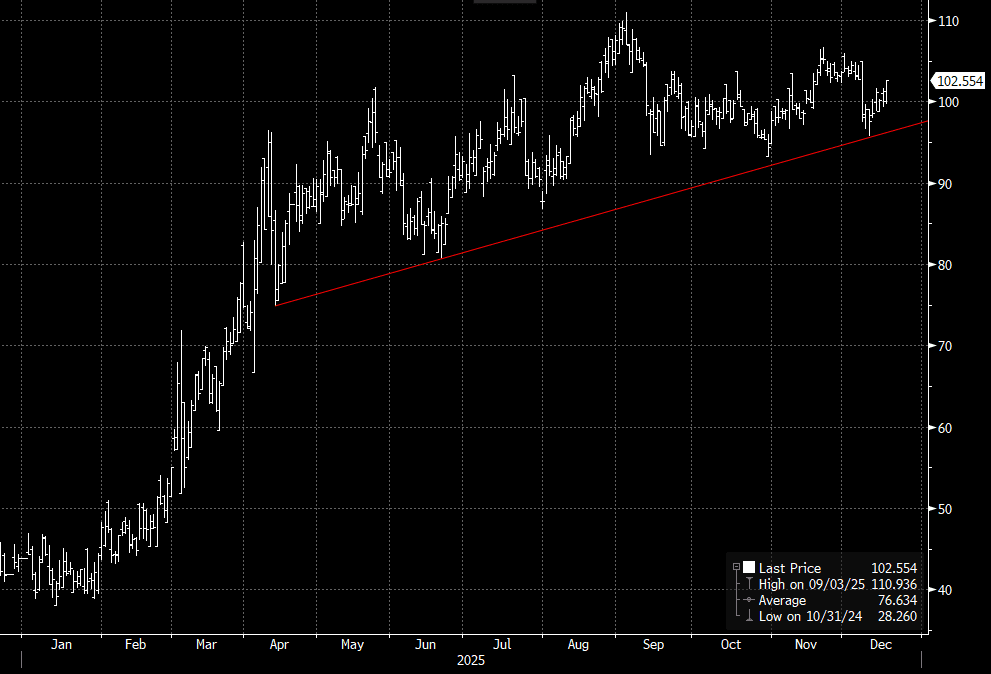

EGBS: Retrace in German 5s30s Suggests Underlying Steepening Theme Intact

The German 5s30s curve has retraced around 60% of the early December flattening, keeping an underlying steepening theme intact. The curve is back above 100bps at 102.4bps, up just over 1bp on the session. Tomorrow’s Eurozone risk events will be key for the direction of the spread into year-end, with the front of the curve eyeing the ECB decision and press conference, and the mid/long-end cognisant of Germany’s 2026 issuance plan.

- Intraday, the curve has twist flattened, with 2-year yields down almost 1bp after spillover from the softer-than-expected UK inflation report this morning.

- An uptick in crude oil futures on reports that the US is preparing fresh sanctions on Russia if Putin rejects the Ukraine peace deal (alongside overnight developments in Venezuela) looks to have helped yields away from session lows.

- Bund futures are + 7 ticks at 127.63, down from earlier highs of 127.79. Initial resistance at 128.08 (Dec 8 high) remains untested.

- 10-year EGB spreads to Bunds are little changed on the session.

- Eurozone final November core HICP inflation confirmed flash estimates at 2.41% Y/Y (vs 2.37% prior). The German December IFO survey was weaker-than-expected, led by the expectations component.

Figure 2: German 5s30s (Source: Bloomberg Finance L.P)

GILTS: CPI-Driven Outperformance Holds Despite Pullback From Highs

This morning’s soft UK CPI data drives outperformance for gilts, as wider core global FI markets pull back from session highs alongside a recovery rally in oil.

- Gilt futures last +45 at 91.39 vs. early session highs of 91.78.

- Initial resistance at 91.64 has been pierced, fresh upside would target more meaningful resistance at 91.93. Conversely, initial support is located at yesterday’s low (90.50).

- Yields 3-5bp lower, 5s outperform.

- Initial yield support levels of note went untested across the curve.

- A reminder that 10-to 30-Year yields registered fresh month-to-date highs yesterday.

- The gilt/Bund spread briefly traded below the September ’24 closing low (162.01bp) before moving back above. Attempted breaks lower failed in recent weeks.

- GBP STIRs fade from dovish session extremes, with BoE terminal rate pricing once again failing to hold moves below 3.30%.

- BoE-dated OIS prices 23.5bp of easing for tomorrow and ~66.5bp of cuts through December ’26. Liquid contracts are 1.5-7.5bp more dovish on the day.

- SONIA futures 2.5-7.0 higher. Fresh cycle highs for SFIZ6 and cycle lows for SFIZ5/Z6 seen following the CPI data.

- With a cut BoE at tomorrow’s decision effectively cemented by this morning’s data, one question now is will there be enough in the data to convince any additional "hawkish" MPC member, in addition to Governor Bailey, to support a cut.

- Expect our full preview of that event later today.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.741 | -23.4 |

Feb-26 | 3.676 | -29.8 |

Mar-26 | 3.574 | -40.1 |

Apr-26 | 3.460 | -51.5 |

Jun-26 | 3.414 | -56.1 |

Jul-26 | 3.353 | -62.2 |

Sep-26 | 3.333 | -64.2 |

Nov-26 | 3.312 | -66.2 |

Dec-26 | 3.310 | -66.4 |

EQUITIES: Latest Pullback for E-Mini S&P Corrective, 50-Day EMA Support Holds

A bull cycle in Eurostoxx 50 futures remains intact. Price is trading above the 20- and 50-day EMAs, and has recently cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this latter price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5649.07, the 50-day EMA. A clear break of the EMA would highlight a potential short-term reversal. A bull cycle in S&P E-Minis remains intact and the latest pullback - for now - is considered corrective. Initial support to watch is 6831.93, the 50-day EMA. It has been pierced, a clear break of this average would signal scope for a deeper retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls, a resumption of gains would refocus attention on the key resistance and bull trigger at 7014.00, the Oct 30 high.

- Japan's NIKKEI closed higher by 128.99 pts or +0.26% at 49512.28 and the TOPIX ended 1.11 pts lower or -0.03% at 3369.39.

- Elsewhere, in China the SHANGHAI closed higher by 45.466 pts or +1.19% at 3870.278 and the HANG SENG ended 233.37 pts higher or +0.92% at 25468.78.

- Across Europe, Germany's DAX trades higher by 27.94 pts or +0.12% at 24104.79, FTSE 100 higher by 145.44 pts or +1.5% at 9830.33, CAC 40 down 5.12 pts or -0.06% at 8101.04 and Euro Stoxx 50 up 10.56 pts or +0.18% at 5728.39.

- Dow Jones mini up 70 pts or +0.15% at 48201, S&P 500 mini up 18 pts or +0.26% at 6819.25, NASDAQ mini up 77.5 pts or +0.31% at 25216.5.

Time: 10:00 GMT

COMMODITIES: WTI Futures Bounce Well Off Tuesday's Lows

A bearish theme in WTI futures remains intact. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $55.99, the Oct 20 low has been breached. Clearance of this level resumes the downtrend and opens $53.53. Key short-term resistance to watch is $61.84, the Oct 24 high. First resistance is at $59.27, the 50- day EMA. A bullish theme in Gold remains intact. The bear phase between Oct 20 - 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4087.6. Clearance of this EMA would signal scope for a deeper retracement. Attention is on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $1.29 or +2.33% at $56.53

- Natural Gas up $0.09 or +2.24% at $3.978

- Gold spot up $15.25 or +0.35% at $4318.89

- Copper up $4.6 or +0.86% at $540.4

- Silver up $1.99 or +3.12% at $65.7637

- Platinum up $82.02 or +4.44% at $1928.66

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 17/12/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/12/2025 | 1405/0905 | New York Fed's John Williams | ||

| 17/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 17/12/2025 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 17/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/12/2025 | 2145/1045 | *** | GDP | |

| 18/12/2025 | - | Bank of Japan Meeting | ||

| 18/12/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 18/12/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 18/12/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 18/12/2025 | 1000/1100 | ** | EZ Construction Output | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 18/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 18/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 18/12/2025 | 1330/0830 | * | Payroll Employment | |

| 18/12/2025 | 1330/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1345/1445 | ECB Press Conference | ||

| 18/12/2025 | 1445/1545 | ECB Staff Macroeconomic Projections | ||

| 18/12/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 18/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 18/12/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 18/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/12/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/12/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 18/12/2025 | 2100/1600 | ** | TICS | |

| 19/12/2025 | 2330/0830 | *** | CPI |