MNI CHINA MONEY MARKET INDEX: Modest Rate Cuts Seen In 2026

Chinese interbank money market traders expect only limited further central bank cuts to the policy rate and reserve requirements in 2026 as policy focus moves to addressing economic structural issues, while ample liquidity will be maintained to ensure market stability, MNI’s China Money Market Index indicated on Wednesday.

The next-six-month policy outlook sub-index showed less expectations for further easing, with only 52.0% of traders seeing additional policy moves, the lowest this year though above the 50% threshold and taking the index to 24.0, the highest in 2025. (the lower it reads, the easier the expected policy stance) However, participants believed the central bank will remain accommodative, with the sub-index for current policy bias falling to 30.0 from 31.0 last month. (See MNI PBOC WATCH: Rate Cuts Pushed Out, Structural Tools Eyed)

The PBOC’s seven-day reverse repo rate outlook sub-index fell to 55.0, with 90%% of participants expecting a steady policy rate in the coming month, compared with 82% last month. Some 82.0% thought the seven-day repo rate for deposit-taking institutions (DR007) will remain steady, with the sub-index rising to 51.0 from 49.0. DR007 is benchmarked by the PBOC’s seven-day reverse repo.

Next year, demand for upgrading China’s economic structures is likely to outweigh any need for quantitative easing, so the People’s Bank of China is likely to rely on existing policies rather than rolling out large-scale new moves, a Beijing trader said. A trade in Zhejiang Province predicted the central bank could cut its rate once in 2026, by around 10 basis points, and that monetary policy would place greater emphasis on structural tools rather than broad-based cuts.

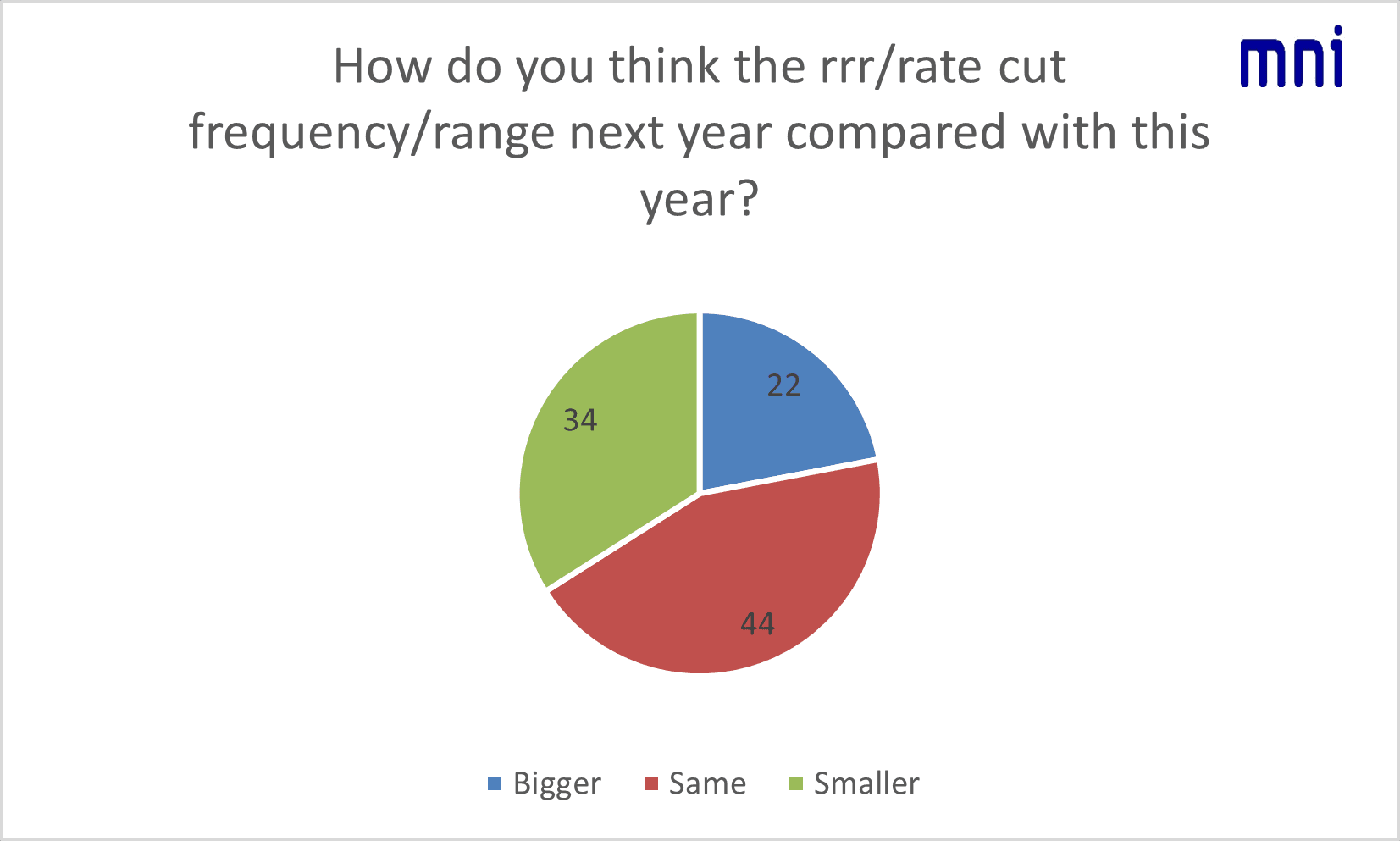

So far this year, the PBOC has only cut its rate once, by 10bp in May, and also reduced reserve requirements just once by 50bp, disappointing market players. MNI’s special question about the possibility of rate and RRR cuts next year showed only 22% of traders thought the pace of rate cuts would be “bigger than 2025,” and 34% thought the pace would be “smaller”.

Even if there is a cut, it would likely aim more at boosting market confidence, with its magnitude expected to be modest, said a Jiangsu trader, though a Beijing trader said monetary policy will have to be strengthened to offset headwinds after November data showed downward pressures rising. (See MNI: China's GDP Faces H2 Growth Challenges)

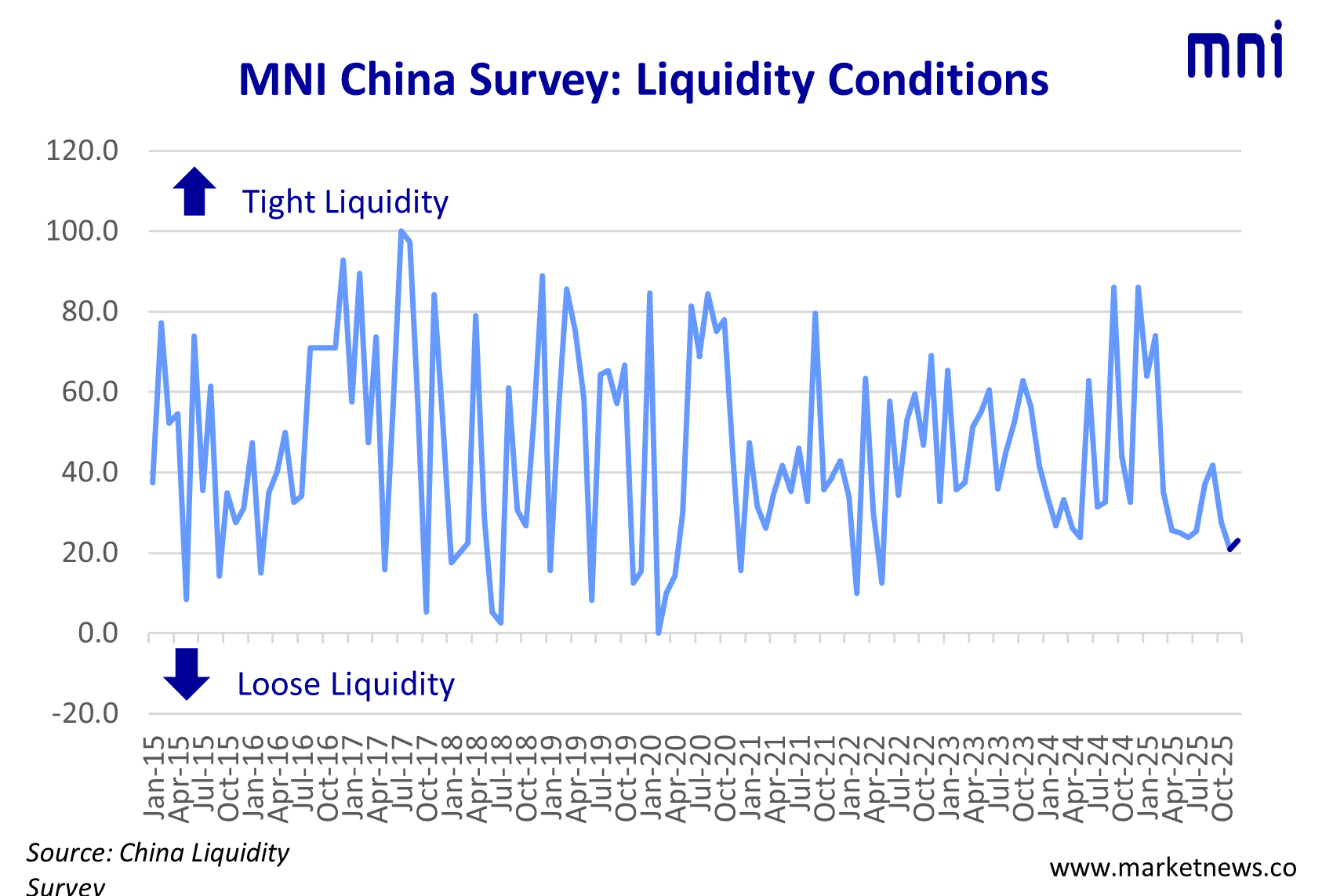

Another special question this month showed traders believed the central bank will meet liquidity needs in the interbank market to limit volatility next year, with 46% of participants seeing “loose liquidity conditions” while 54% expect “neutral conditions.”

There could be short-term liquidity fluctuations, such as during peak periods of government bond issuance or bond market volatility, but overall conditions should be benign, a Tianjin trader noted.

China’s liquidity outlook sub-index fell to 47.0 from 51.0, with 78.0% expecting the same comfortable conditions next month thanks to the PBOC’s accommodative bias. The overall sub-index for the PBOC’s Open Market Operations outlook rose to 47.0 from 45.0, with 26% of participants seeing “net drains" next month, the highest since June as the PBOC could withdraw liquidity after increasing injections this month to meet seasonal demand.

The sub-index covering current liquidity conditions edged up to 23.0 from 21.0 last month, with 54.0% of participants seeing looser liquidity than last month. The sub-index covering the PBOC’s current open market operations showed 94% of participants assessed OMOs as being “in line with demand,” compared with 100% last month.

Despite large year-end cash demand and maturities of negotiable certificates of deposit, increased central bank operations signal its accommodative stance, with narrower fluctuations in funding rates compared to previous quarter-ends, said a Jiangsu trader.

A trader in Shanghai told MNI two outright reverse repos operations had been conducted this month, with a net injection of CNY200 billion in medium-term liquidity, demonstrating a clear easing intent.

The coming-month outright reverse reps operations outlook sub-index slipped to 23.0% from 27.0%, indicating more traders expected the PBOC would increase operations.

The MNI China Money Market Index (MMI) survey was conducted from Dec 1 to Dec 12, with participation of 50 traders from both state-owned and joint-venture banks.

MNI's China Money Market Index official press release is attached:

Hidden PDF