NEW ZEALAND: Q3 Current Account Deficit, As % Of GDP, Continues Improvement

The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. In seasonally adjusted terms we were slightly wider in Q3 at -NZD3.8bn. As a percent of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve, we were at -9.0% of GDP at the end of 2022.

- The bulk of the deficit remains on the income side, close to -NZD3bn. The goods and services balances remain modestly in deficit.

- The goods balance has improved in recent years. Focus going forward will be on export growth, amid signs that whole milk prices are trending lower, a key NZ export. Imports may also improve if we see a stronger domestic demand impulse.

- Note this Friday delivers Nov trade data.

- The NZD will be influenced by the structural current account deficit trend, with the Kiwi likely to remain sensitive to risk off episodes in global markets. Near term correlations though ware likely to remain strong with NZ-US rate differentials.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Cheaper In Line With US Tsys Close On Friday

NZGBs are 1-3bps cheaper after US tsys finished with a modest bear-steeper on Friday.

- With the US federal government shutdown now over, some postponed data is starting to come into view, with the BLS scheduling September's delayed nonfarm payrolls report for next Thursday, and the Census Bureau set to publish some delayed August data next week. Still, there's no official word on the fate of the October CPI release, which looks very likely to be cancelled altogether.

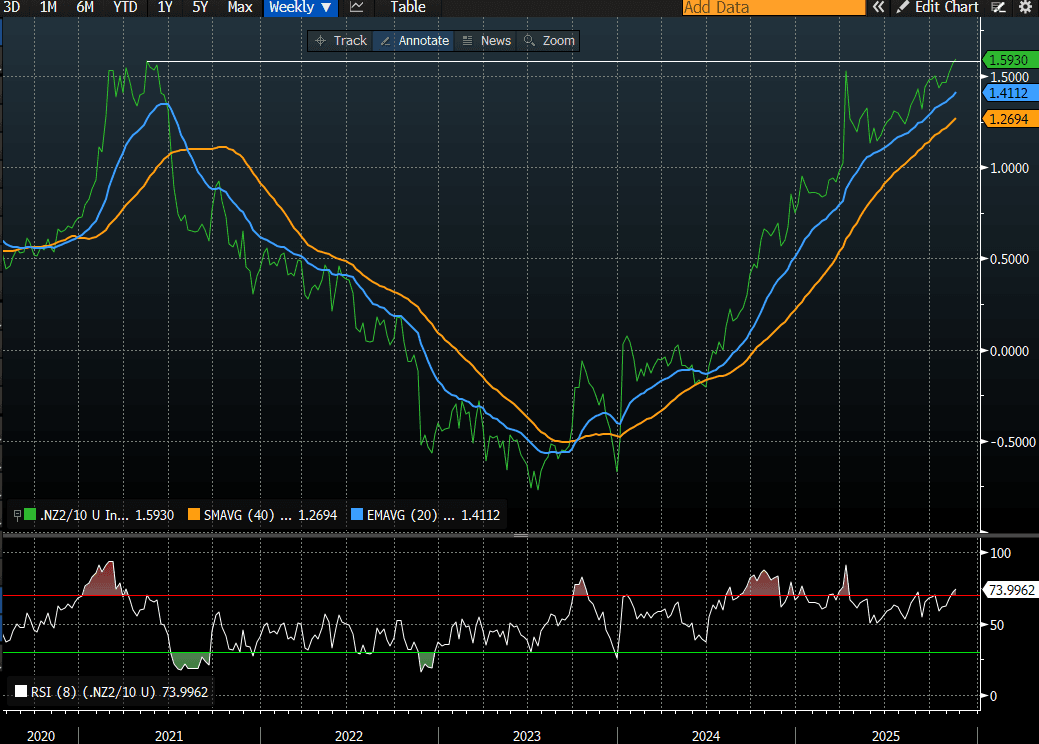

- NZ 2/10 yield curve is back at cycle highs, the highest since 2021. (see chart)

- The Oct services PMI (via BNZ and Business NZ) edged up to 48.7 from 48.3 in Sep. We look to be on a steady improvement trend, but from depressed levels and the index hasn't been above the 50.0 expansion/contraction point since early 2024. The sub indices mostly ticked higher, but also remain under 50.0. Activity was 48.9, versus 48.0 prior, employment up to 48.8, versus 47.9 in Sep. The employment index eased back to 49.5 from 49.7 prior.

- Food prices fell 0.3% m/m in October, while fuel and energy prices rose and airfares cheapened.

- Swap rates are 2-3bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is little changed across meetings. 25bps of easing is priced for November, with a cumulative 34bps by February 2026.

Bloomberg Finance LP

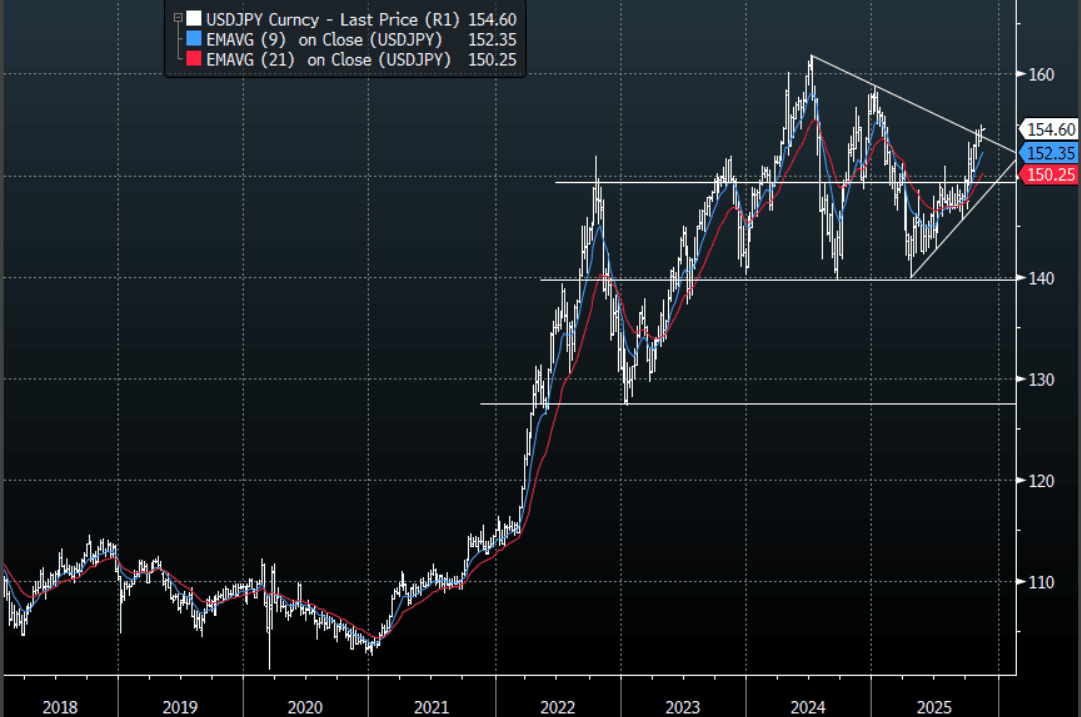

JPY: USD/JPY - Brushes Of Weak Risk Sentiment, Back To Challenging 155.00

The Friday night range was 153.62 - 154.76, Asia is currently trading around 154.60. The pair found solid demand back toward the 153.50 support on Friday night and very quickly erased all the day's losses as risk stabilised into the weekend. The move lower in Crypto this morning could re-inflame the negative sentiment of last week, watch the crosses for signs of Yen demand. Usd/Jpy though itself seems to remain well supported on dips as the market remains wary of the new leadership policies. The price action points to a renewed challenge of the resistance toward 155.00, a sustained break above here and it could start to pick up momentum to the topside again.

- MNI: Japan Q3 GDP - Growth is projected to be negative in the quarter, amid weaker business spending and a drag from next exports. Consumption growth is also forecast to have slowed.

- MNI INTERVIEW: US Job Market Continues To Slow - Glassdoor. The U.S. job market is continuing to slow but there are no signs of a more worrisome decline, Glassdoor chief economist Daniel Zhao told MNI, adding that the Federal Reserve should continue its fight against inflation.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.39b), 154.70($400m). Upcoming Close Strikes : 155.00($1.31b Nov 20), 150.00{$1.3b Nov 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 85 Points

- Data/Event : GDP, Capacity Utilization, Industrial Production

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

NEW ZEALAND: Oct Services PMI Up But Still Sub 50, Pointing To Tepid Recovery

The Oct services PMI (via BNZ and Business NZ) edged up to 48.7 from 48.3 in Sep. We look to be on a steady improvement trend, but from depressed levels and the index hasn't been above the 50.0 expansion/contraction point since early 2024. The sub indices mostly ticked higher, but also remain under 50.0. Activity was 48.9, versus 48.0 prior, employment up to 48.8, versus 47.9 in Sep. The employment index eased back to 49.5 from 49.7 prior.

- The outcome doesn't point a sharp turn higher in early Q4 economic momentum. BNZ noted (via BBG): "Sector continues to struggle for forward momentum with the sub-component gauges all below long-term averages and making for ”dreary reading”.