MNI US OPEN - Data Postponements Loom as US Shutdown Begins

EXECUTIVE SUMMARY

- PAYROLLS, CPI DATA POSTPONEMENTS LOOM AMID FEDERAL GOVERNMENT SHUTDOWN

- FED'S LOGAN CAUTIOUS ON CUTS GIVEN STILL-HIGH INFLATION

- BENCHMARK BUSINESS SENTIMENT ROSE SLIGHTLY IN BOJ TANKAN SURVEY

- RBI ON HOLD AGAIN, NEUTRAL STANCE RETAINED

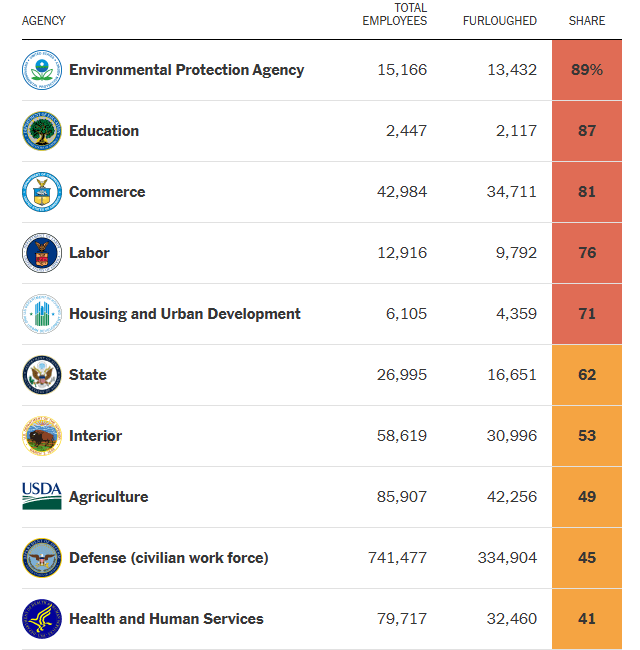

Figure 1: How the shutdown is affecting federal services and workers

Source: New York Times

NEWS

US (MNI): Federal Government Shutdown: Payrolls, CPI Data Postponements Loom

Amid the US federal government "shut down" starting today, we answer some of the most frequently asked questions we've received.

- How long will it last? Prediction markets yesterday were signalling there's a higher than 50% market-implied chance that it lasts more than 5 days, and 40% it lasts more than 10 days.

- How will this impact data releases? With only essential government services being performed during a shutdown, this would effectively mean that any data from federal agencies including the Bureau of Labor Statistics, Bureau of Economic Analysis, and other agencies (commodities data via Dept of Agriculture and Dept of Energy) would be postponed until after the end of the shutdown.

- What are the data releases that are set to be postponed? The two key data releases that would be impacted by a shutdown through mid-month are Friday's Employment report for September, and the CPI report on Oct 15 (and PPI the next day).

- What data will we get? Private-sector compiled data will still be released after September 30, and this will serve as an alternative of sorts to the official government data to gauge economic developments.

- Will Treasury auctions be affected? These are considered "essential" and will be conducted as normal.

FED (MNI): Fed's Logan Cautious on Cuts Given Still-High Inflation

U.S. inflation is still too high and persistent for the Federal Reserve to comfortably cut interest rates much further, Dallas Fed President Lorie Logan said Tuesday. "I will be cautious about further rate cuts," Logan said. "Even setting aside temporary effects of this year’s increases in tariff rates, inflation is not convincingly on track to return all the way to 2%."

US (BBG): White House Pulls Antoni’s Nomination for Head of BLS

The White House pulled the nomination of EJ Antoni to lead the Bureau of Labor Statistics, throwing the leadership of the critical data agency into further disarray after President Donald Trump fired the former commissioner. A White House official said that the administration looked forward to nominating a new candidate soon. Antoni did not immediately respond to a request for comment.

US/MIDEAST (BBG): Hamas Said to Meet With Qatar, Turkey Officials Over Trump Plan

Members of Hamas’s political wing met officials from Qatar, Egypt, and Turkey in Doha on Tuesday as part of the militant group’s deliberations over a US peace plan for Gaza, according to a person familiar with the matter. The Hamas delegation told the officials it was carefully reviewing the 20-point plan announced by US President Donald Trump on Monday, and is seeking clarity on some technical aspects, the person said. It is preparing its response once its consulted with other Palestinian factions about the plan, which is meant to end the almost-two year war in Gaza between Hamas and Israel.

US/S.KOREA (BBG): South Korea Agrees to Share Monthly FX Intervention Data With US

South Korea agreed to provide the US with monthly data on foreign-exchange interventions and publish the annual currency composition of its reserves, under a new accord aimed at boosting transparency while reaffirming commitments to avoid currency manipulation. The US Treasury Department and South Korean Finance Ministry said the deal was reached alongside ongoing tariff talks, according to a joint statement Wednesday, emphasizing that any intervention should be limited to curbing excessive volatility or disorderly market moves.

EU (RTRS): EU Plans to Cut Steel Import Quotas, Hike Tariffs

The European Commission will propose cutting steel import quotas by nearly half and hiking duties on volumes above those quota levels to as high as 50%, similar to tariffs imposed by the United States and Canada, a source briefed on details told Reuters on Wednesday. The measures will be part of a new safeguards package for the steel sector, which is set to be officially unveiled on October 7.

ECB (MNI): Fiscal Policy Could Prompt Market Correction - Guindos

Loose fiscal policy in both Europe and the U.S. could be the factor that triggers a correction in financial markets which could be overvalued, European Central Bank Vice President Luis de Guindos said in an event organised by Politico on Wednesday. Markets are taking a lot of risks and an important correction could arrive that could also be amplified by looser regulation of non-banks, de Guindos said.

BOE (BBG): BOE’s Mann Says UK Policy is ‘Loose,’ Backs Keeping Rates at 4%

UK monetary policy is “relatively loose” and interest rates need to remain on hold, according to Bank of England official Catherine Mann. Speaking in an interview with Bloomberg TV on Wednesday, Mann warned of the threat from high household inflation expectations and said US tariffs are yet to weigh on price pressures in the UK.

BOJ (MNI EXCLUSIVE): BOJ's Tankan Raises Hike Odds, Ueda Speech Eyed

MNI discusses the BOJ's hiking strategy following key sentiment data. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (MNI): LDP Favourite Talks Up Gov't/BoJ Cooperation, Touts Supplementary Budget

In an interview with Nikkei, Agriculture, Forestry and Fisheries Minister Shinjiro Koizumi says that "It is important for the government and the Bank of Japan to share the same overall direction", and that "the government's economic policy and the Bank of Japan's monetary policy will work together to realise a virtuous cycle in the economy." Koizumi is viewed as the strong frontrunner for the leadership of the governing Liberal Democratic Party (LDP) ahead of the 4 October election.

INDIA (MNI): RBI on Hold, Neutral Stance Retained

The Central Bank in India, the RBI, kept its key rate unchanged at 5.5% today. The unanimous vote, consistent with the last meeting, sees the central bank retaining its neutral stance . Inflation remains subdued yet the tariff situation remains and the focus on India by the US and EU for purchases of Russian oil creates uncertainty which it seems the Central Bank wants to see play out.

DATA

EUROZONE DATA (MNI): HICP Broadly In Line With Consensus

- EUROZONE SEP FLASH HICP +2.2% Y/Y, +0.1% M/M

- EUROZONE SEP FLASH CORE HICP +2.3% Y/Y, +0.1% M/M

- EUROZONE SEP FLASH SERVICES HICP +3.2% Y/Y, -0.9% M/M

Eurozone HICP came in at a little below the MNI tracking of 2.3% with 2-way risks at 2.23%Y/Y, but broadly in line with the market consensus. Core and services both rounded down to consensus expectations, although core at 2.35%Y/Y was almost 2.4%. It appears as though FAT (food, alcohol and tobacco) is the only notably surprise, coming in softer than expected at 3.04%Y/Y (down from 3.19%Y/Y where it was expected to remain). No substantial market reaction, given that the data was broadly in line with expectations.

SPAIN DATA (MNI): Manufacturing PMI Downward Surprise

- SPAIN SEP MANUF PMI 51.5 (53.8 FCAST, 54.3 AUG)

The Spanish Manufacturing PMI notably underperformed in September, coming in at 51.5 (53.8 cons; 54.3 August) in its first decline from the prior since April. This marks a three month low: "Weaker gains in both output and new orders signalled", the release concludes. Key highlights: "Weaker gains in both output and new orders. Notably, the rise in production was the softest for four months. Despite weakening, new order book growth remained solid amid reports of firm demand and new product introductions."

ITALY DATA (MNI): Manufacturing PMI Joins Spain and Surprises to Downside

- ITALY SEP MANUF PMI 49.0 (49.9 FCAST, 50.4 AUG)

The Italian manufacturing PMI slipped back into contraction in September, at 49.0 (49.9 cons; 50.4 August). Taking into account the Spain miss, we watch for any revisions on Germany for a potential downward revision for the Eurozone-wide release (scheduled for 09:00 BST / 10:00 CEST, flash at 49.5). Key highlights: "Contributing to the contraction in operating conditions was a renewed drop in new orders. September data indicated a solid decrease in new sales, and one that was the fastest since June. The reduction in new business was attributed by firms to hesitancy among customers amid economic uncertainty."

UK DATA (FT): UK House Prices Rise More Than Expected in September

UK house prices increased more than expected in September as still-low unemployment and rising wages underpinned growth, lender Nationwide said on Thursday. The group, whose monthly index provides the first indications of the health of the housing market, said house prices rose 0.5 per cent between August and September, taking the average cost to £271,995. The annual rate edged up to 2.2 per cent in September, from 2.1 per cent the previous month.

SWITZERLAND DATA (MNI): August Retail Sales Weak But Broader Picture Solid So Far

Swiss (real) retail sales were rather weak in August on a sequential comparison, at -0.2% M/M. Looking at the drivers of the release shows that weakness was centred in the "remaining" category (which contains a lot of durable goods). The August data was the first incorporating the 39% US tariffs levied on Swiss goods. The question is if this filtered through to consumer scepticism here already.

JAPAN DATA (MNI): BOJ Tankan: Key Sentiment Rises, Solid Capex Plans

- BOJ SEPT TANKAN LARGE MFG INDEX 14; JUNE 13; MEDIAN 15

- BOJ TANKAN LARGE NON-MFG INDEX 34; JUNE 34; MEDIAN 34

Japanese benchmark business sentiment rose slightly in September for the second straight quarter, while non-manufacturers’ sentiment remained flat, the Bank of Japan’s Tankan survey showed Wednesday. The diffusion index for major manufacturers climbed to +14 from +13 in June, the highest since December 2024, though it is projected to ease to +12 in December. Sentiment among major non-manufacturers was steady at +34, but is expected to slip to +28 three months ahead. For smaller firms, the index for manufacturers held at +1 in September and is seen dipping into negative territory at -1 by December.

JAPAN DATA (MNI): BOJ Tankan: Business Inflation Expectations Solid

Japanese firms’ one-, three- and five-year inflation expectations, closely watched by the Bank of Japan, were largely unchanged from June and remained solid, the BOJ’s September Tankan survey showed Wednesday. On average, companies expect consumer prices to rise 2.4% over the next year, the same as in June. They also see inflation at 2.4% three years ahead, unchanged, and 2.4% five years ahead, slightly above the previous 2.3%.

FOREX: Government Shutdown Tips USD Lower for 4th Session, JPY Main Beneficiary

- The initial impact of the US government shutdown have proved negative for the USD: the USD Index is lower for a fourth consecutive session, pressing prices toward the late September lows of 97.221, but still has someway to go before any test of the cycle and pullback low into 96.218.

- How the government shutdown impacts markets more broadly may be defined by availability of data and the longevity of such a shutdown. Given the higher-than-expected current run rate for growth in the US, a prolonged shutdown will almost certainly have a slowing effect on the economy in early Q4. While this Friday's NFP data will almost certainly be delayed (and possibly the US CPI print on October 15th), the scarcity of data is unlikely to steer the FOMC away from a further 25bps rate cut in October, currently priced at ~24bps.

- The JPY is the strongest currency in G10, gaining amid the uncertainty stemming from the US government shutdown as well as the drift off highs for global equities. A stronger-than-expected Tankan manufacturing sentiment index overnight adds a further tailwind, endorsing BoJ tightening in the medium-term. The e-mini S&P is off just over 0.5% at pixel time, putting futures over 50 points off the alltime high. CAD/JPY is through several key levels as a result, clearing clustered horizontal support layered between 105.95 - 106.01.

- Focus for the session ahead rests on any confirmation from the Federal Government that incoming data releases will be delayed - a very likely outcome - but also any clues on the longevity of the current shutdown.

BONDS: EGBs & Gilts Off Lows

Core global FI markets have stabilised after an early sell off, a downtick in oil provides cross-market support.

- Presence of the impending German 10-Year supply applied some pressure through early trade, while U.S. government shutdown headlines continue to dominate.

- A reminder that the U.S. NFP release, scheduled for Friday, is set to be delayed on the back of the shutdown.

- Bund futures trade as low as 128.24, before recovering to ~128.40. Initial support at the 128.26-29 zone was pierced, but not convincingly.

- German yields are 1-3bp higher curve steeper.

- Presence of the German supply and a recovery from worst levels in equities leaves major EGB spreads vs. Bunds flat to 1bp tighter.

- The NTMA confirmed that it will conduct one IRISH auction in Q4. No real reaction in IRISH spreads, although we think that the market would have been looking for no auctions in Q4, given precedent set in recent years.

- Gilts have also recovered from session lows, futures 90.70, bouncing from 90.54.

- Bears remain in technical control in that contract. Initial support and resistance located at 90.26 & 91.28, respectively.

- UK yields flat to 2.5bp higher, curve steeper.

- Ongoing UK fiscal deterioration helps keep the steepening technical trend intact. The latest round of reporting reaffirmed that Chancellor Reeves is set to scrap the two-child benefit limit, albeit with the potential for limitations given the potential for spiralling costs to cover larger families.

- ECB-dated OIS pricing little changed, showing ~8bp of further easing for the current cycle, while BoE-dated OIS shows less than 5bp of easing through year-end.

EQUITIES: EuroStoxx 50 Futures Maintain a Bullish Theme

Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance and the bull trigger at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend and paves the way for a climb towards 5564.82, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Initial firm support lies at 5452.19, the 20-day EMA. A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, initial support to watch lies at the 20-day EMA, at 6656.22. It has been pierced, a clear break of it would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6541.51.

- Japan's NIKKEI closed lower by 381.78 pts or -0.85% at 44550.85 and the TOPIX ended 42.86 pts lower or -1.37% at 3094.74.

- Across Europe, Germany's DAX trades higher by 5.74 pts or +0.02% at 23886.54, FTSE 100 higher by 61.63 pts or +0.66% at 9412.07, CAC 40 up 7.5 pts or +0.1% at 7903.44 and Euro Stoxx 50 down 2.46 pts or -0.04% at 5527.5.

- Dow Jones mini down 250 pts or -0.54% at 46441, S&P 500 mini down 42 pts or -0.62% at 6697, NASDAQ mini down 181 pts or -0.73% at 24720.75.

Time: 10:00 BST

COMMODITIES: Gold at Fresh Record High, Fibonacci Resistance at $3909.4

WTI futures have pulled back from their recent gains. The contract has recently breached $65.43, the Sep 2 high and this has potentially improved the S/T condition for bulls. However, the next key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. For bears, a clear reversal lower would refocus attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend. The trend condition in Gold is unchanged and a bull cycle remains in play. The yellow metal has traded to a fresh cycle high this week, confirming a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3646.3, the 20-day EMA. A pullback would be considered corrective.

- WTI Crude down $0.17 or -0.27% at $62.2

- Natural Gas up $0.07 or +2.18% at $3.375

- Gold spot up $33.96 or +0.88% at $3893.53

- Copper up $0.35 or +0.07% at $485.8

- Silver up $0.73 or +1.57% at $47.38

- Platinum up $16.35 or +1.04% at $1593.46

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 01/10/2025 | 0955/1055 | BOE Mann In Bloomberg Interview | ||

| 01/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 01/10/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/10/2025 | 1215/0815 | *** | ADP Employment Report | |

| 01/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/10/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 01/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 01/10/2025 | 1730/1330 | BOC Summary of Deliberations | ||

| 01/10/2025 | 1805/1405 | BOC Sr Deputy Rogers speaks at competition panel | ||

| 02/10/2025 | 0130/1130 | ** | Trade Balance | |

| 02/10/2025 | 0630/0830 | *** | CPI | |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University |