EQUITIES: EuroStoxx 50 Futures Reversing Some of the Week's Earlier Gains

Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance and the bull trigger at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend and paves the way for a climb towards 5564.82, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Initial firm support lies at 5452.19, the 20-day EMA. A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, initial support to watch lies at the 20-day EMA, at 6656.22. It has been pierced, a clear break of it would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6541.51.

- Japan's NIKKEI closed lower by 381.78 pts or -0.85% at 44550.85 and the TOPIX ended 42.86 pts lower or -1.37% at 3094.74.

- Across Europe, Germany's DAX trades higher by 5.74 pts or +0.02% at 23886.54, FTSE 100 higher by 61.63 pts or +0.66% at 9412.07, CAC 40 up 7.5 pts or +0.1% at 7903.44 and Euro Stoxx 50 down 2.46 pts or -0.04% at 5527.5.

- Dow Jones mini down 250 pts or -0.54% at 46441, S&P 500 mini down 42 pts or -0.62% at 6697, NASDAQ mini down 181 pts or -0.73% at 24720.75.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

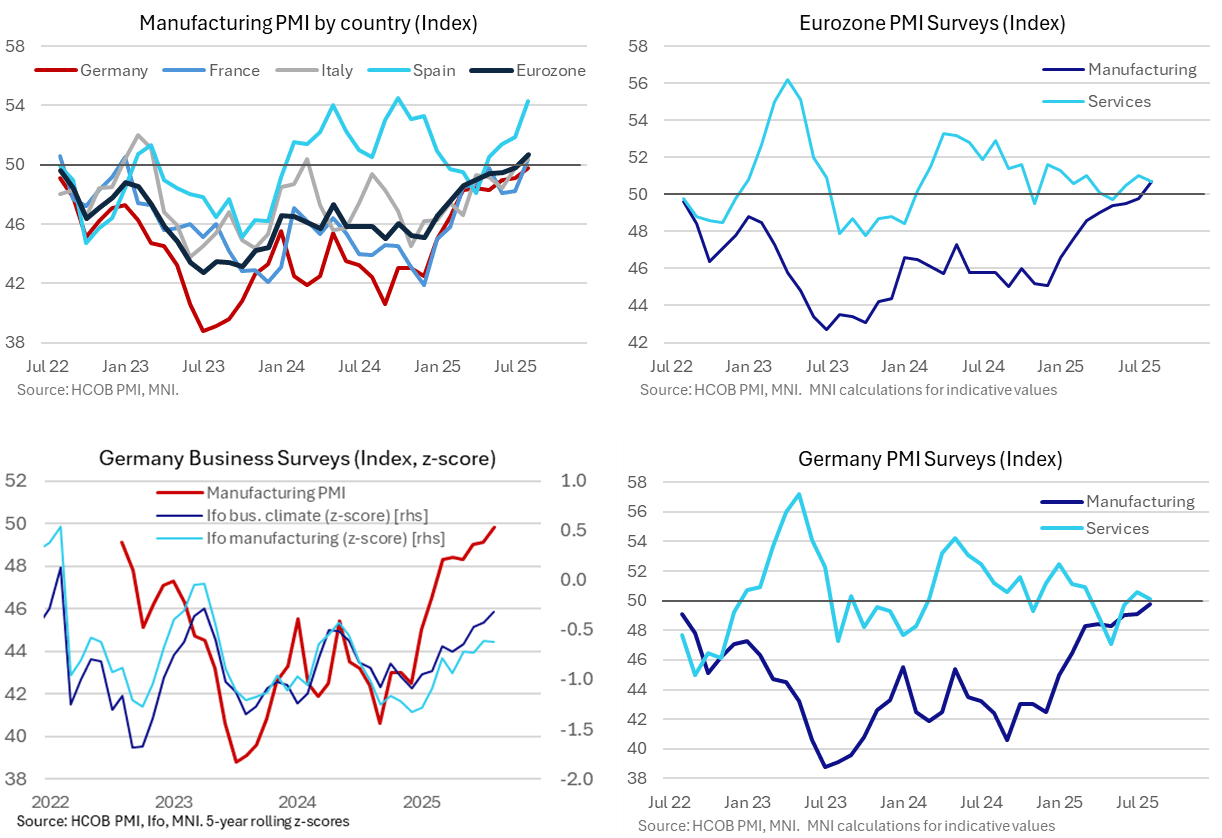

EUROZONE DATA: German Mfg PMI Lags Further Despite August Improvement

The Eurozone final August manufacturing PMI release was revised higher to further confirm a 38-month high. Despite a string of improvements it is still only just above the 50 breakeven line, although has closed a sizeable gap to services (ahead of Wednesday's revisions for the latter). Latest manufacturing improvements were seen across the board although Germany continues to lag France and Italy modestly, whilst Spain is an even clearer outperformer.

- The Eurozone manufacturing PMI was revised up to 50.7 in the final August release (prelim 50.5) to extend the increase to what was its first above-50 (i.e. expansionary) reading in the three-year lookback for publicly available data and a 38-month high per the press release.

- Within that, factory output was revised up from 52.3 to 52.5, a solid improvement from the 50.6 in July for still a 41-month high.

- The press release also confirmed that “eurozone manufacturers saw operating expenses increase for the first time in five months, although the uptick was only marginal.” However, prices “charged were discounted fractionally.”

- Germany was revised down a tenth to 49.8 (prelim 49.9) to trim an increase from 49.1 in July, with the EZ upward revision itself helped by a larger than first thought bounce in France to 50.4 (prelim 49.9) from 48.2.

- Our rough calculations also point to stronger than first implied manufacturing readings elsewhere, with our Eurozone ex Germany & France estimate revised up to 51.6 (prelim 51.2) after 51.0 in July.

- As we noted earlier, today’s first details for Spain were particularly robust at 54.3 (cons 52.1) after 51.9 for just shy of cycle highs of 54.5 in Oct 2024. Italy meanwhile increased to 50.4 after 49.8.

USD: Broader selling going through

- Another round of Dollar selling here, EUR is heading towards the initial resistance of 1.1743 High Aug 22.

- The AUD, GBP, CAD, SEK, PLN, MXN, INR, CZK, NOK, NZD are all lifted.

- AUDUSD now targets the next immediate resistance at 0.6569, 14th Aug high.

STIR: Danske Recommend Paying June '26 Vs. Dec '25 & Dec '26 ECB On Fly

Danske Bank recommend tactically paying the June ‘26 ECB meeting vs. receiving the Dec ‘25 and Dec ‘26 meetings on an ECB-dated OIS fly structure.

- They note that their “baseline is for the pricing of additional rate cuts from the ECB to move closer to zero as the economy has proven surprisingly resilient and downside risks to the outlook have faded. However, the prospects of inflation moving below 2% and wage indicators remaining soft also dampen the likelihood of the ECB kicking off rate hikes in late ‘26”.