MNI US OPEN - BOE Rate Cut, ECB Hold Widely Anticipated

EXECUTIVE SUMMARY

- BOE RATE CUT AND A 5-4 VOTE SPLIT EXPECTED

- ECB AGAIN FULLY EXPECTED TO LEAVE KEY RATES ON HOLD

- US CPI THREATENS TO BE MESSY RELEASE

- RIKSBANK TO HOLD POLICY RATE "FOR SOME TIME"

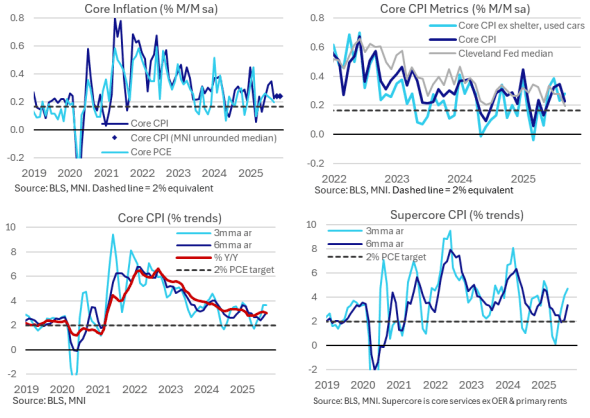

Figure 1: Recent US inflation developments

MNI PREVIEWS

MNI US CPI PREVIEW: Handle With Care

The latest delayed CPI update from the Bureau of Labor Statistics threatens to be messy in several regards, muddying the signal for markets and for monetary policy. The government shutdown precluded October data collection, meaning overall CPI aggregates will not be available for the month, and the inflation recorded for November is on a 2-month change basis from Sept. While the M/M data will never be officially available, MNI's usual aggregation of sell-side analyst expectations points to expectations of an average of 0.24% M/M core CPI monthly across October and November.

MNI BOE PREVIEW: What Follows a Christmas Cut?

Governor Bailey is almost unanimously expected to join the four dovish dissenters and deliver a Christmas BOE 25bp rate cut at tomorrow's meeting (expected unanimously by the sell side and priced over 23bp at the time of writing). The market will be looking for more nuance at this meeting so we look at our top 7 things to watch in the meeting (assuming we do get the expected cut; if we don’t then the market isn’t going to pay much attention to the details!). We also summarise over 20 sellside previews - a 5-4 vote split is expected by the majority but analysts are split over what happens after December.

MNI ECB PREVIEW: Relative Resilience Confirms in a Good Place

The ECB is again fully expected to leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff. This time though the meeting comes against a backdrop of a very mild hiking bias to end-2026, helped by recent rhetoric from Schnabel, which despite having been pared fairly notably in recent days is still a change from a modest easing bias ahead of recent meetings.

MNI BOJ PREVIEW: Hike Fully Priced

The BOJ is widely expected to raise the policy rate by 25bp to 0.75% at the December 18–19 meeting, with Governor Ueda’s recent remarks signalling increased confidence in the outlook for growth, inflation and wage momentum. Ueda has indicated the BOJ will assess the “pros and cons of raising the policy interest rate,” while Policy Board members say conditions for a hike are “gradually falling into place,” though confirmation of spring wage momentum remains key.

MNI BANXICO PREVIEW: Cut Seen, Hawkish Risks Prevalent

Banxico is expected to deliver another 25bp rate cut to 7.0% on Thursday as it continues to respond to weak activity data, which revealed a contraction of the economy in the third quarter. However, recent stronger-than-expected CPI inflation data have significantly increased the risk of a pause in the easing cycle, if not this week, then more likely early in the new year, keeping focus on the forward guidance.

MNI COLOMBIA CB PREVIEW: Hold Seen, Risk of Hike

BanRep is expected to leave its policy rate unchanged at 9.25% for a fifth consecutive meeting on Friday, in another split decision, although risks of a hike have increased significantly amid mounting concerns over the inflation outlook. Rising inflation expectations, strengthening domestic demand and increasing fiscal pressures have prompted the majority of the BanRep board to strike a more hawkish tone recently, with the market now pricing in over 150bp of rate hikes over the next year.

MNI CNB PREVIEW: Repo Rate to End 2025 at 3.50%

The Czech National Bank will almost certainly deliver a well-telegraphed unanimous decision to keep the two-week reference rate unchanged at 3.50% at the final meeting of this year as concerns about familiar inflationary risks continue to linger. Although headline inflation moderated to +2.1% Y/Y in November, the property market is running hot, wages are still growing at pace, and there is considerable uncertainty about the fiscal outlook under the new government.

MNI CBR PREVIEW: Easing Pace to Be Maintained

The CBR is expected to continue with monetary policy easing following two months of lower-than-expected inflation readings. Governor Elvira Nabiullina has previously advised that further easing is to be approached with caution, and therefore a larger 100bp rate cut is seen only as an outside possibility. According to a poll published by Vedomosti, 17 of 23 analysts expect the central bank to lower its key interest rate by 50bps to 16.00%.

NEWS

RISKBANK (MNI): Riksbank to Hold Policy Rate "For Some Time"

Sweden's Riksbank left its policy rate unchanged at 1.75% on Thursday, and will hold it there "for some time to come," as it assesses the current rate level is helping to strengthen domestic demand and economic activity. The economic outlook appears slightly better compared with the bank's September forecasts, while the inflation outlook is similar, although the bank said that the outlook was marked by geopolitical conflicts, uncertain US policy, high asset valuations in financial markets and weak public finances in several countries.

NORGES BANK (MNI): Norges Bank Holds, Sees Easing in 2026

Norges Bank left its key policy rate on hold at 4% in December, as expected, and its policy committee said that if things evolved as expected that it expected the policy rate to be lowered further in the coming year. Governor Ida Wolden Bache said that "we are not in a hurry to reduce the policy rate" with the forecasts in the December Monetary Policy Report similar to those published in September. The policy rate in the Monetary Policy Report projection was shown at 3.9% in 2026 before declining to 3.4% in 2027 and 3.2% in 2028

EUROPEAN COUNCIL (MNI): High-Stakes Summit Gets Underway w/Ukraine Funding to Dominate

EU leaders are meeting for one of the most contentious European Council summits in years. The major topic of discussion is how to financially support Ukraine in the months and years ahead, with its funding due to expire as soon as spring 2026. With President Volodymyr Zelenskyy in attendance, leaders are split on whether to use frozen Russian assets held in the EU to fund 'reparations loans' or issue joint debt. European Council President Antonio Costa said, "We will never leave this Council without a final decision to ensure the financial needs of Ukraine." However, it remains difficult to see a path to agreement.

US (BBG): Trump Says He’ll Announce New Fed Chair Soon

President Trump says he will announce the next chairman of the Federal Reserve soon. Trump speaks during an address to the nation from the White House. Trump says new chair will be “someone who believes in lower interest rates.” Trump says he will announce “some of the most aggressive housing reform plans in American history” in the new year.

US (BBG): Trump Says Military Members Will Receive ‘Warrior Dividend’

President Trump says more than 1.45 million military members will receive checks for $1,776 before Christmas. Trump speaks during an address to the nation from the White House. Trump calls the checks “warrior dividends.”

US/JAPAN (BBG): US, Japan Panel Convene to Mull Projects for $550 Billion Fund

A US-Japan consultation panel held its first meeting to consider initial projects for a $550 billion investment pledge that is a pillar of the two countries’ trade deal. The panel met online, exchanged views on potential projects for the investment initiative and confirmed ongoing close cooperation, Japan’s Foreign Ministry said Thursday. The meeting was attended by representatives from the US Commerce Department, Energy Department and Japan’s foreign, trade and finance ministries.

CHINA (MNI): China Has Begun Granting Rare Earth General Licenses

MNI (Beijing) Beijing has begun issuing general licenses to compliant rare-earth exporters, He Yadong, spokesperson for the Ministry of Commerce, told reporters on Thursday. The licenses, which are intended to fast-track the export control process, had come after gaining more experience with exports and compliance processes, He added.

CHINA (BBG): China Ships More Rare-Earth Products as Export Controls Ease

China shipped 13% more rare-earth products in November than in the preceding month, a sign that a more relaxed export regime is restoring flows of the critical minerals used in electric vehicles, weapons and high-tech manufacturing. The 6,958 tons of rare-earth products — including magnets — exported in November was the third-highest monthly total on record, according to Bloomberg calculations using official customs data. The numbers suggest that China has stepped up shipments since agreeing a yearlong trade truce with the US.

TAIWAN (BBG): Taiwan Holds Benchmark Rate as Economy Roars on AI Frenzy

Taiwan held its policy rate for the seventh straight quarter — the longest stretch since 2021 — as the economy booms on global demand from AI developers for its tech products. The monetary authority left the benchmark rate unchanged at 2%, according to a statement released after its quarterly meeting on Thursday. All 32 of the economists surveyed by Bloomberg News had predicted the move.

INDIA (BBG): India’s Key Export State Says US Tariffs Decimating Industries

One of India’s richest states that’s heavily reliant on exports said high US tariffs are causing “irreparable damage” to businesses in the region and called on Prime Minister Narendra Modi to urgently seek a trade deal with Washington. M. K. Stalin, the chief minister of Tamil Nadu, said export orders have dried up in some districts, resulting in a daily loss of 600 million rupees ($6.7 million) in revenue.

DATA

GERMANY DATA (MNI): IFO Export Expectations Remain Below Neutral in December

The German IFO Export Expectations index rose marginally in December, to -3.1 points, from -3.8 in November. While the index is off its cycle lows, IFO continues to remain on the pessimistic side regarding German export prospects, commenting "the outlook for the first quarter of 2026 is rather subdued. Any real revival in exports just isn't happening".

FRANCE DATA (MNI): Business Confidence Broadly Stronger, but Employment a Touch Weaker

French business confidence saw a third consecutive 1 point rise to 99 in December, the highest since June 2024. The rise was driven mainly by strength in the manufacturing and retail components, with moderate growth in construction, and stable services. The only downward driver was the employment indicator, which fell 1 point to 94, unwinding November's rise. This release is broadly consistent with recent flash PMIs which showed stronger-than-expected manufacturing and weaker services sentiment.

NEW ZEALAND DATA (MNI): Q3 GDP Beats Expectations, Up 1.1% Q/Q

New Zealand’s economy grew 1.1% quarter on quarter in Q3, rebounding from Q2’s revised 1.0% contraction and exceeding the market forecast of a 0.9% increase, data released by Stats NZ on Thursday showed. The outcome was also stronger than the Reserve Bank of New Zealand’s most recent forecast, which had expected GDP to rise 0.4%. Business services rose 1.6%, driven by gains in computer system design and related services, advertising, market research and management services, and scientific, architectural and engineering services.

FOREX: USD Tilts Higher Ahead of US CPI, NOK Rises Post-Norges Bank

- Despite the initial downside pressure on the USD this week in the lead up to the US employment report, momentum quickly stalled. Short-term positioning dynamics have assisted a moderate dollar squeeze, tilting the USD index into positive territory on the week. Intra-day sentiment and the lack of momentum continue to reflect the limited appetite ahead of a busy central bank calendar as well as the key US CPI data release later today.

- The 0.2% bump higher for the DXY is seeing similar broad-based declines across the rest of the G10. With the Bank of England a particular focus today, GBPUSD has just slipped back below the 1.3350 mark, however, spot remains comfortably above yesterday’s post CPI lows of 1.3312. Initial firm support is 1.3293, the 50-day EMA, and a breach of this average would highlight a possible technical reversal.

- Overnight, New Zealand GDP data rose above expectations in Q3, however, prior downside revisions more than offset the initial beat. This helped NZDUSD slip further back below the 0.5800 pivot point, and spot currently hovers just above its 20- and 50-day EMA’s.

- NOK is a moderate outperformer on the day after Norges Bank remained on hold as expected but revisions to the rate path pushed back on significant easing expectations ahead. This led EURNOK to see a 11.94 session low. Initial support is the prior breakout level of 11.8612 (Nov 25 high). Conversely for SEK, the lack of endorsement for hawkish market pricing amid the expected Riksbank hold may be having some marginal dovish readthrough.

- USDJPY meanwhile extends yesterday's upside, standing just below the 156.00 handle at typing. This means the post-NFP bounce totals around 1.0% as we approach Friday's BOJ meeting, where a 25bp hike to the policy rate remains priced in. Short-term technical parameters appear well defined at 154-158.

BONDS: Yields Flat to Lower Ahead of BoE & ECB, German 20s Lag on Syndi Plans

Wider core global FI markets have drawn support from the late NY-Asia uptick in Tsys and pullback in crude oil futures.

- Bund futures +14 at 127.55.

- Our technical analyst’s initial support and resistance levels (127.05 & 128.16) untouched.

- German yields unchanged to 2bp lower, 5s outperform on the curve. Long end lags with 20s cheapening on the 10s20s30s fly.

- This comes after the DFA’s ’26 funding plan revealed a planned syndication for a new 20-Year line, which was a surprise. Long end bonds have cheapened vs. swaps since.

- The broader funding plan was generally in line with our estimates on the capital markets side (albeit with a greater skew to Bubills and 3 non-green Bund syndications vs. the 2 we had pencilled in, providing a modest undershoot vs. our estimated range).

- EGB spreads to Bunds little changed to 1bp tighter, peripheral compression aided by an uptick in equities.

- STIRs price ~10% odds of any further ECB easing, reaction to last week’s hawkish comments from Schnabel have been tempered, presenting a better balance of risk into today’s decision.

- Gilt futures +15 at 91.59.

- Resistance layered in at 91.78 & 91.93, while initial support comes in at 91.19, followed by 90.50.

- Yields 1.5-3.0bp lower across the curve, flattening seen.

- 10-Year spread to Bunds breaches 160bp, next downside level of note 156.93bp.

- SONIA futures flat to +2.0. BoE-dated OIS pricing 24bp of easing for today’s decision, with terminal rate price once again gravitating to ~3.30%.

- Elsewhere, U.S. weekly jobless claims and CPI data is also due.

EQUITIES: This Week's Pullback for Eurostoxx Futures Considered Corrective

A bull cycle in Eurostoxx 50 futures remains intact and the latest pullback is considered corrective. The first key support to watch lies at 5650.52, the 50-day EMA. A clear break of the average would highlight a potential short-term reversal. This would open 5594.00, the Nov 26 low. For bulls, a resumption of gains would refocus attention on key resistance and the bull trigger at 5825.00, the Nov 13 high. The pullback in S&P E-Minis has resulted in a breach of both the 20- and 50-day EMAs. This strengthens a short-term bear theme and signals scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11. Sights are on 6737.71, a Fibonacci retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls a resumption of gains would refocus attention on key resistance at 7014.00, the Oct 30 high.

- Japan's NIKKEI closed lower by 510.78 pts or -1.03% at 49001.5 and the TOPIX ended 12.5 pts lower or -0.37% at 3356.89.

- Elsewhere, in China the SHANGHAI closed higher by 6.093 pts or +0.16% at 3876.371 and the HANG SENG ended 29.35 pts higher or +0.12% at 25498.13.

- Across Europe, Germany's DAX trades higher by 28.72 pts or +0.12% at 23989.64, FTSE 100 higher by 22.26 pts or +0.23% at 9795.95, CAC 40 up 21.58 pts or +0.27% at 8107.37 and Euro Stoxx 50 up 16.83 pts or +0.3% at 5698.11.

- Dow Jones mini up 61 pts or +0.13% at 47969, S&P 500 mini up 27.25 pts or +0.41% at 6753.75, NASDAQ mini up 188.75 pts or +0.77% at 24858.25.

Time: 10:00 GMT

COMMODITIES: Gold Continues to Trade Just Below Bull Trigger

A bearish theme in WTI futures remains intact. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low has been breached. Clearance of this level resumes the downtrend and opens $53.77, a Fibonacci projection. Key short-term resistance to watch is $61.25, the Oct 24 high. First resistance is at $58.94, the 50- day EMA. The trend structure in Gold remains bullish. The bear phase between Oct 20 - 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4097.5. Clearance of this EMA would signal scope for a deeper retracement. Attention is on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude up $0.19 or +0.34% at $56.08

- Natural Gas up $0.07 or +1.69% at $4.096

- Gold spot down $15.52 or -0.36% at $4322.47

- Copper down $1.65 or -0.3% at $541.75

- Silver down $0.33 or -0.49% at $65.9242

- Platinum up $13.21 or +0.69% at $1914.2

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 18/12/2025 | 1200/1200 | *** | Bank of England Interest Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Main Refinancing Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 18/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 18/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 18/12/2025 | 1330/0830 | * | Payroll Employment | |

| 18/12/2025 | 1330/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1345/1445 | ECB Press Conference | ||

| 18/12/2025 | 1445/1545 | ECB Staff Macroeconomic Projections | ||

| 18/12/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 18/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 18/12/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 18/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/12/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/12/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 18/12/2025 | 2100/1600 | ** | TICS | |

| 19/12/2025 | 2330/0830 | *** | CPI | |

| 19/12/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/12/2025 | 0300/1200 | *** | BOJ Policy Rate Announcement | |

| 19/12/2025 | 0700/0700 | *** | Public Sector Finances | |

| 19/12/2025 | 0700/0800 | ** | PPI | |

| 19/12/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 19/12/2025 | 0700/0800 | ** | Retail Sales | |

| 19/12/2025 | 0700/0700 | *** | Retail Sales | |

| 19/12/2025 | 0745/0845 | ** | PPI | |

| 19/12/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 19/12/2025 | 0830/0930 | ECB Wage Tracker | ||

| 19/12/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/12/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 19/12/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 19/12/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 19/12/2025 | 1200/1300 | ECB Cipollone Remarks, Roundtable at Aspen Institute | ||

| 19/12/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 19/12/2025 | 1330/0830 | ** | Retail Trade | |

| 19/12/2025 | 1400/1500 | ** | BNB Business Confidence | |

| 19/12/2025 | 1500/1000 | *** | NAR existing home sales | |

| 19/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 19/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 19/12/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 19/12/2025 | 1510/1610 | ECB Lane Lecture at Central Bank of Ireland | ||

| 19/12/2025 | 1630/1630 | BOE to announce APF Q4 Sales Schedule | ||

| 19/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |