EUROPEAN COUNCIL: High-Stakes Summit Gets Underway w/Ukraine Funding To Dominate

EU leaders are meeting for one of the most contentious European Council summits in years. The major topic of discussion is how to financially support Ukraine in the months and years ahead, with its funding due to expire as soon as spring 2026. With President Volodymyr Zelenskyy in attendance, leaders are split on whether to use frozen Russian assets held in the EU to fund 'reparations loans' or issue joint debt. European Council President Antonio Costa said, "We will never leave this Council without a final decision to ensure the financial needs of Ukraine." However, it remains difficult to see a path to agreement.

- On his arrival, Hungarian PM Viktor Orban said that the idea of using frozen Russian assets is "dead" as there is a blocking minority against it.

- European High Representative for Foreign Affairs and Security Policy Kaja Kallas says, "I agree with [German Chancellor Friedrich] Merz. It's 50/50", adding that countries would not progress with the idea without Belgium's approval, even if a qualified majority (55% of countries representing 65% of EU population) is reached. She claims that Belgium's concerns about being left financially exposed by legal demands from Russia have been addressed, saying, "We will all take the risk".

The EU-Mercosur trade deal could also feature. It is ostensibly due to be signed on 20 Dec after two decades of negotiation. However, strong opposition from France and Poland, and delaying tactics from Italy, look more likely to scupper the prospect of agreement on the largest trade deal in EU history.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

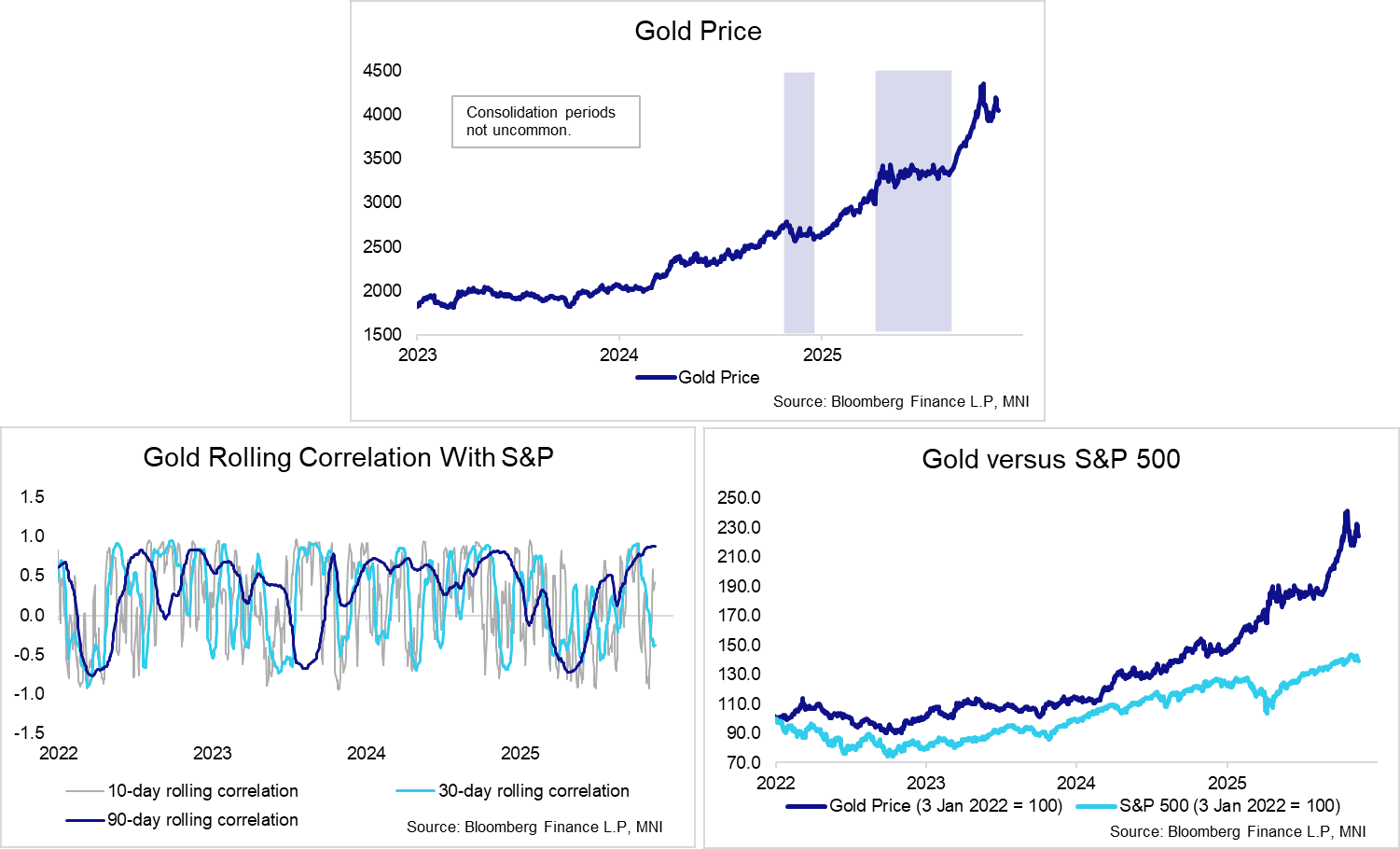

GOLD: 50-day EMA Support Still Intact, Consolidation Phase May Be Healthy

Gold has not acted as a risk hedge during the past week, with spot selling off alongside equities and narrowing the gap to key support at the 50-day EMA ($3,932 today). A clear break of this EMA would signal scope for a deeper retracement, exposing the Oct 28 low at $3,887 and round number support at $3,800. However, provided the 50-day EMA remains intact, a consolidation phase at current levels may be healthy for gold, and lay the groundwork for fresh extension higher. Longer-term bull themes such as central bank buying and debt monetisation continue to be favoured. Goldman Sachs estimate China added 15 tons of gold in September, well above the 1.24 tons officially reported (write-up per Bloomberg).

- In recent weeks, the combination of falling Fed rate cut expectations and a tightening of US liquidity conditions have worked against gold, spurring a fresh bout of profit taking/deleveraging after a solid rally through September/October.

- It’s worth remembering that Gold’s 90-day rolling correlation with the S&P has been positive for most of the last three years, save for isolated periods in early 2022, mid 2023 and Q2 2025 (the latter being Liberation Day fallout). Shorter-horizon rolling correlations are unsurprisingly more volatile.

- Through gold’s 100% rally since the start of 2024, consolidation periods and minor corrections have not been uncommon. Recall that price traded in a horizontal fashion in the four months from mid-April to mid-August.

- In their 2026 outlook, TD Securities write that “lower rates, continued tilt toward debasement narratives, along with supply side dynamics and asset managers looking for diversification are set to make gold, copper and crude oil perform above expectations”. Goldman Sachs still see gold at $4,900/oz by the end of next year.

GILTS: Yields Edge Lower As Equities Soften

Gilt yields little changed to ~1bp lower as global equities weaken, light steepening bias.

- Gilt futures trade +9 at 92.48. Initial support and resistance 91.94 & 92.85. Our technical analyst still deems the recent weakness to be corrective at this stage.

- 2s10s within 1bp of the October closing high (74.26bp) and 5s30s a little over 1bp off its October closing high (140.12bp).

- Gilt/Bunds 183bp after failing to push above 185bp in recent sessions, still holding most of the recent recovery from sub-175bp.

- Immediate focus remains on tomorrow’s inflation data (click for our full preview) and next week’s Budget.

- Comments from BoE’s Pill (voted to leave rates unchanged earlier this month) & Dhingra (the most dovish MPC member) are due today.

- A reminder that we do not expect much market vol. to stem from any non-Bailey BoE comments in the lead up to the December decision, given the entrenched views of the other MPC members (Bailey is deemed the key swing voter).

- On the supply front, the DMO will come to market with GBP1.25bln of the 4.75% Dec-30 gilt via tender this morning

US DATA: Jobless Claims Data For W/E Oct 18 Slightly Above MNI's Estimates

At the time using state-level data, MNI had estimated jobless claims in the week to Oct 18 to be a seasonally adjusted 227k - so 5k below the 232k figure being presented here.

Data for the week-ending Sep 20 and Sep 13 are also available:

- Sep 20: 219k vs MNI estimate of 218k

- Sep 13: 232k vs MNI estimate of 231k

Note that data for the week ending Oct 18 is technically a payrolls reference period, as was the week ending Sep 13 (that's possibly why the Oct 18 is being published now). The DOL source we posted earlier suggests claims data for the week ending Sep 27, Oct 4 and Oct 11 are not yet available.