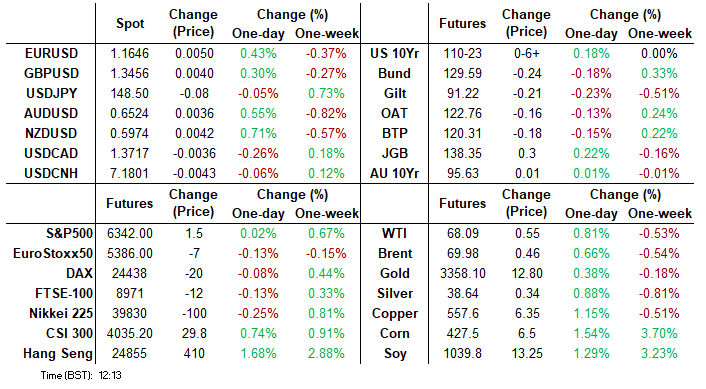

MNI US MARKETS ANALYSIS - USTs Within Range of Mid-Week High

Highlights:

- Treasuries sit mildly firmer on light volumes, with Waller, UMich sentiment next up

- USD Index tilted lower following Waller's dovish interjection yesterday

- Trump renews criticism of the Fed Chair after mid-week furore over Powell's position

US TSYS: Mildly Firmer On Light Volumes Ahead Of A Thinner Docket

- Treasuries are modestly firmer with little meaningful headlines to shift away from dovish Waller comments late yesterday. Volumes are light.

- Today’s docket is lighter than recent heavy sessions, highlighted by housing data and the preliminary U.Mich consumer survey for July. President Trump also participates in a signing ceremony for the Genius Act at 1430ET with pre-credentialed media.

- Cash yields are 1-2bp lower, with 30s lagging declines.

- TYU5 trades at 110-21+ (+05) having kept to a narrow range since lifting in reaction to Waller. It remains within yesterday’s range though and on particularly light volumes of 180k.

- Resistance is seen at 110-30+ (20-day EMA) but the bear threat remains present. Support is seen at 110-08+ (Jul 14/16 lows) before 110-03 (76.4% retrace of May 22-Jul 1 bull leg).

- Data: Housing starts/permits (0830ET), U.Mich consumer survey Jul prelim (1000ET)

- Fedspeak: Waller on Bloomberg TV (0800ET)

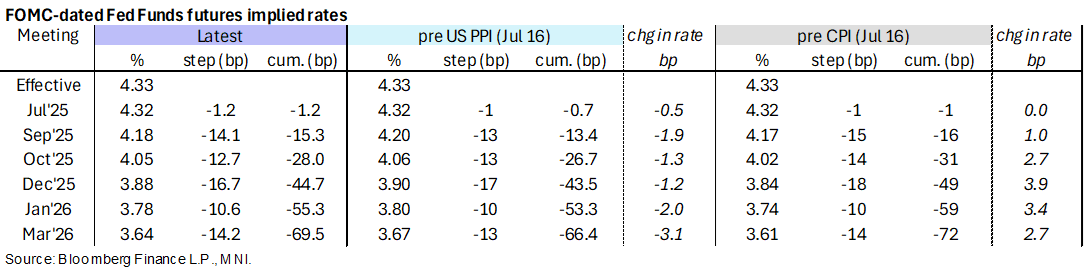

STIR: Dovish Waller Has Some Lasting Impact, FOMC Blackout Starts Tonight

- Fed Funds implied rates are 0.5-2bp lower for 2025 meetings from Friday’s close after Fed Governor Waller’s reiteration of dovish comments late yesterday.

- The near-term path remains a little more hawkish than prior to Tuesday’s CPI report which contained some stronger underlying details for core goods. There have been many developments since then, including a dovish PPI report and Trump-Powell termination back and forth before a strong retail sales report but dovish import prices.

- Cumulative cuts from 4.33% effective: 1bp Jul, 15.5bp Sept, 28bp Oct, 44.5bp Dec, 55bp Jan and 69.5bp Mar.

- The SOFR implied terminal yield of 3.205% (SFRZ6, -3bp) implies roughly 4.5 cuts from current levels.

- Gov. Waller (permanent voter) late yesterday clearly doubled down on his dovish stance, starting his speech with “My purpose this evening is to explain why I believe that the FOMC should reduce our policy rate by 25 basis points at our next meeting.”

- He speaks again on Bloomberg TV at 0800ET and is currently the last scheduled appearance ahead of the FOMC media blackout starting 0001ET Saturday ahead of the Jul 29-30 meeting.

FED: Dovish Waller Doubles Down On July Cut, More Cuts This Year

In case missed late yesterday, Governor Waller (permanent voter, dove) clearly doubled down on his dovish stance, starting his speech with “My purpose this evening is to explain why I believe that the FOMC should reduce our policy rate by 25 basis points at our next meeting.” It’s not a new approach from Waller but continues to stand out along with Bowman amidst the Fed’s independence being threatened by President Trump’s call for 1% rates. For context, see FED: Waller Sees Rate Cuts As Early As July, Pushing Back On Powell (Jun 20) and FED: Bowman And Waller Setting Up For A July Dissent (Jun 23). Waller is seen as very likely one of the two June SEP dots for three cuts this year, with a particularly divided FOMC considering there were also seven dots looking for zero cuts. The market still views July cut calls as posturing, with just 0.5bp priced.

Excerpts from the speech (found in full here):

- "The risks to the economy are weighted toward cutting sooner rather than later. If the slowing of economic and employment growth were to accelerate and warrant moving toward a more neutral setting more quickly, then waiting until September or even later in the year would risk us falling behind the curve of appropriate policy."

- If headline inflation data report modest, temporary increases from tariffs that are not unanchoring inflation expectations and the economy continues to grow slowly, he would support "further 25 basis point cuts to move monetary policy toward neutral" later this year.

- “The data imply the policy rate should be around neutral, which the median of FOMC participants estimates is 3%, and not where we are - 1.25 to 1.50 percentage points above 3%. While I sometimes hear the view that policy is only modestly restrictive, this is not my definition of 'modestly.'"

Subsequent Q&A (from Bloomberg headlines):

- Want to cut rates to give a little more stimulus

- Nothing wrong with taking out an insurance cut

- Evidence suggests the neutral rate isn’t far from 3%

- The Trump administration hasn’t talked to be about the Fed chair job

US TSY FUTURES: Long Cover Dominated On Thursday

OI data points to net long cover through US futures on Thursday, while the unchanged price status of WN futures come settlement makes it hard to provide any real inference when it comes to the modest uptick in OI in that contract.

- The most meaningful round of net long cover came via TY futures.

| 17-Jul-25 | 16-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,365,123 | 4,371,554 | -6,431 | -241,079 |

FV | 6,991,349 | 7,013,388 | -22,039 | -943,187 |

TY | 4,796,545 | 4,834,099 | -37,554 | -2,459,356 |

UXY | 2,394,008 | 2,405,455 | -11,447 | -988,595 |

US | 1,784,232 | 1,793,845 | -9,613 | -1,304,803 |

WN | 1,964,518 | 1,962,331 | +2,187 | +390,724 |

|

| Total | -84,897 | -5,546,296 |

SOFR: Net Short Setting Dominated Through The Greens On Thursday

OI data points to net short setting dominating in pack terms through the SOFR greens on Thursday, albeit with some isolated pockets of net long cover seen.

- Net long cover was slightly more prominent in the blues, where positioning swings were modest.

| 17-Jul-25 | 16-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,239,477 | 1,254,145 | -14,668 | Whites | +26,232 |

SFRU5 | 1,247,959 | 1,230,097 | +17,862 | Reds | +31,898 |

SFRZ5 | 1,305,434 | 1,291,251 | +14,183 | Greens | +23,356 |

SFRH6 | 1,011,368 | 1,002,513 | +8,855 | Blues | -1,333 |

SFRM6 | 882,843 | 862,753 | +20,090 |

|

|

SFRU6 | 836,842 | 829,318 | +7,524 |

|

|

SFRZ6 | 914,256 | 914,465 | -209 |

|

|

SFRH7 | 732,677 | 728,184 | +4,493 |

|

|

SFRM7 | 701,655 | 691,981 | +9,674 |

|

|

SFRU7 | 509,645 | 511,260 | -1,615 |

|

|

SFRZ7 | 455,139 | 448,681 | +6,458 |

|

|

SFRH8 | 316,162 | 307,323 | +8,839 |

|

|

SFRM8 | 229,463 | 231,070 | -1,607 |

|

|

SFRU8 | 208,177 | 207,344 | +833 |

|

|

SFRZ8 | 207,705 | 207,600 | +105 |

|

|

SFRH9 | 150,585 | 151,249 | -664 |

|

|

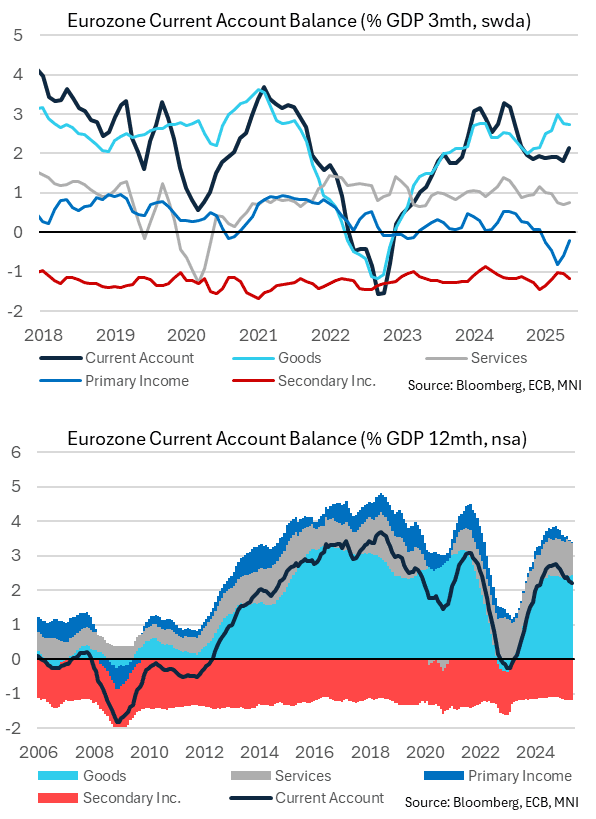

EUROZONE DATA: Stable Trends In CA Components On 12m GDP Basis In May

The Eurozone seasonally adjusted current account surplus increased to E32.3bln in May, driven largely by increases in the services and primary income balances. On a 3m rolling basis to nominal GDP, the CA surplus rose to 2.1%, the highest since September 2024.

- On the other hand, the NSA current account surplus was just E1.0bln (vs E18.0bln prior), with the primary income balance seeing a seasonally regular outflow worth E34.8bln. On a 12-month rolling basis to GDP, the current account surplus fell a touch to 2.2% from 2.3% in April – the lowest since March 2024.

- As noted in our write-up of the May merchandise trade data yesterday, the goods surplus has seen a partial stabilisation after surpluses surged in Feb and Mar primarily on US tariff front-running of Irish pharmaceutical exports. In May, the NSA goods surplus was E30.9bln, up from E27.3bln in April but down from a notable E52.0bln in March. The goods surplus is still worth 2.4% of GDP on a 12-month basis.

- The services surplus similarly still accounts for 1.0% GDP, with the primary income balance at 0.0% and the secondary income deficit at 1.2%.

FOREX: USD Index Tilts Lower Post Waller, But Consolidating Weekly Advance

- Both treasury yields and the dollar track modestly lower on Friday as Fed Governor Waller reiterated his relatively dovish stance and advocated for a 25bp cut at the next FOMC meeting. This dynamic has allowed the likes of AUD (+0.46%) and NZD (+0.56) to outperform on the session, while the Scandies top the G10 FX leaderboard.

- In similar vein, EURUSD (+0.35%) has been steadily edging higher after regaining the 1.16 handle to currently trade at session highs of 1.1644. Despite an ongoing bearish corrective cycle playing out, the ongoing resilience for the single currency has been notable with EURUSD remaining comfortably above its firm support of the 50-day EMA which is located around 1.1510.

- Despite the softer greenback today, the USD index is broadly consolidating a solid weekly advance of around 0.5% and fresh recovery highs this week underpin the more constructive short-term outlook. Both the Australian dollar and the Japanese yen have been particular laggards across the week, as domestic developments weigh.

- In Australia, a much weaker-than-expected jobs report has bolstered RBA easing bets, while the increased volatility surrounding the Trump-Powell spat has likely provided an additional headwind to higher beta currencies. AUDUSD support at the 50-day EMA, at 0.6490, was temporarily breached. A clear break of this EMA would highlight a stronger reversal and signal scope for an extension lower.

- In Japan, the focus remains centred on the upper house elections, which will be held over the weekend. The ruling party is still projected to lose its majority there and associated fiscal concerns have allowed USDJPY to reach fresh 3-month highs this week above 149.00. Above here, attention will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high.

- Preliminary US UMich data, housing starts/building permits and further comments from Fed Governor Waller headline the macro calendar today.

OPTIONS: Sizeable Strikes Could Keep G10 FX Pinned into UMich Sentiment Data

With just housing/building permits data due ahead of the prelim UMich sentiment at 1000ET today, there are a sizeable number of option strikes worth noting for today's NY cut: E1bln at 1.1650 in EUR/USD, $521mln at Y148.50 in USD/JPY, Gbp1.3bln at 1.3395-10 in GBP/USD and A$1.2bln at $0.6480-00 in AUD/USD.

That said, much market focus may be paid to the appearance of Fed's Waller on BBG TV at 1300BST/0800ET - while spoke just yesterday, he continues to stand out along with Bowman amidst the Fed's independence being threatened by President Trump's call for 1% rates.

Full option pipeline:

- EUR/USD: $1.1566-70(E899mln), $1.1600(E2.2bln), $1.1650(E1.0bln),

$1.1700(E1.3bln), $1.1850(E1.2bln) - USD/JPY: Y148.00($597mln), Y148.25($844mln), Y148.50($521mln)

- GBP/USD: $1.3395-10(Gbp1.3bln)

- AUD/USD: $0.6455-60(A$695mln), $0.6480-00(A$1.2bln)

- NZD/USD: $0.5932-50(N$498mln)

- USD/CAD: C$1.3715-30($1.3bln)

COMMODITIES: Bearish WTI Theme Persists

- Gold is unchanged. A bull cycle that started Jun 30, remains intact and the yellow metal is holding on to the bulk of its recent gains - for now. Note that medium-term trend conditions are bullish.

- A bearish tone in WTI futures remains intact and gains are considered corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower.

EQUITIES: Stock Futures Strike New Record Highs

- S&P E-Minis are trading higher today and this has resulted in a fresh cycle high. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows.

- A bull cycle in Eurostoxx 50 futures remains in play and recent weakness appears to have been a correction. Support to watch is 5281.00, the low on Jul 1 and 4. A clear break of this price point would strengthen a bearish threat.

| Date | GMT/Local | Impact | Country | Event |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 18/07/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |