MNI US MARKETS ANALYSIS: USD Off Highs, BoE Eyed

Highlights

- Near-term Fed rate path back to only marginally below pre-FOMC levels, 45bp cuts to year-end.

- Treasuries pare some post-Powell losses to remain within ranges after TY came close to support.

- USD bid stalls as London morning progresses.

- The BoE decision headlines today, supplemented by US Philly Fed and jobless claims data.

MNI BOE Preview: September 2025 - QT Decision Key

For the full MNI BOE Preview including summaries of over 20 sell side views, click here.

- The outcome for this week’s MPC meeting can be boiled down to two discrete topics: the vote surrounding the pace of APF reduction and any updates on communications and the vote surrounding Bank Rate. The biggest uncertainty and market reaction is expected around the former, with much less focus being placed upon the latter – but neither aspect should be ignored.

- If the APF decision was down to us, we would favour a target of GBP60-65bln with active sales in line with this year but with a change to the maturity buckets to re-align with the DMO. That would see short remaining at 3-7 years, medium to 7-15 years (rather than BOE’s 7-20 years) and long 15+ years (rather than 20+ years).

- Around 70% of analysts look for the decision to be between GBP60-75bln - but the range is wide from ending active sales (GBP49bln total reduction) to continuing with the total reduction of GBP100bln.

- A 7-2 vote split is widely expected (by us and the analyst previews we have read) with both Dhingra and Taylor dissenting for a 25bp cut.

- We would be surprised by a change in guidance - given that it was tweaked at the last meeting.

FED: MNI Fed Review-Sept 2025: No Risk-Free Paths Now

- The Fed resumed its easing cycle with the first cut of the year on September 17, of 25bp to a range of 4.00-4.25%. That decision was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference.

- Despite a lower rate path signaled in the new Dot Plot, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

- See PDF report for:

- MNI View

- Market Reaction

- MNI Instant Answers

- Press Conference Transcript

- FOMC Meeting Links

- Policy Statement Changes

- Dot Plot/Econ Projections

BOC: MNI BoC Review-Sept 2025: Balancing Risks, Open To Cut Further (1/2)

- The Bank of Canada resumed easing on September 17 after a 3-meeting hold, with a 25bp rate cut to the overnight rate to 2.50%. There was limited market reaction on net to the decision and press conference, with the BOC as expected keeping the door open to further easing as soon as the next meeting in October, but falling short of any firm guidance to that effect.

- The future path of rates repriced slightly to reflect the implemented cut (which had not quite been fully priced going into the meeting, reflecting a slightly hawkish move going into the release).

- While rate cut expectations diminished slightly early in the press conference after headlines reported Gov Macklem saying that they considered holding rates, this didn’t appear to be a signal as he was merely citing a formality (“I there was a clear consensus to cut our policy rate by 25 basis points. You know we as we have for the last couple of meetings, we considered two alternatives, hold the policy rate where we are, or cut the policy rate.”)

- Otherwise, attention was on whether the BOC would signal further cuts. July’s guidance suggesting that there may be a “need” to cut rates in future was removed, but overall the BOC maintained its easing bias.

- Macklem entertained press questions about what would trigger a further cut, and the overall communications highlighted risks to growth and employment alongside what the BOC sees as better-contained inflationary pressures than had been feared in the summer.

- He continually mentioned the need for a balanced approach to future rate-setting, moving meeting-by-meeting and keeping the next decision in October live.

- This was summed up by his comment: “what we can do is help the economy adjust while maintaining well-controlled inflation. That's what we're focused on... it's going to be about balancing those risks. If the risks tilt, if the risks shift, we're prepared to take action, and if the risks tilt further, we're prepared to take more action, but we're going to take it one meeting at a time. We are taking a shorter horizon. We're being a little less forward looking than usual, and we'll make that risk assessment in October when we get there."

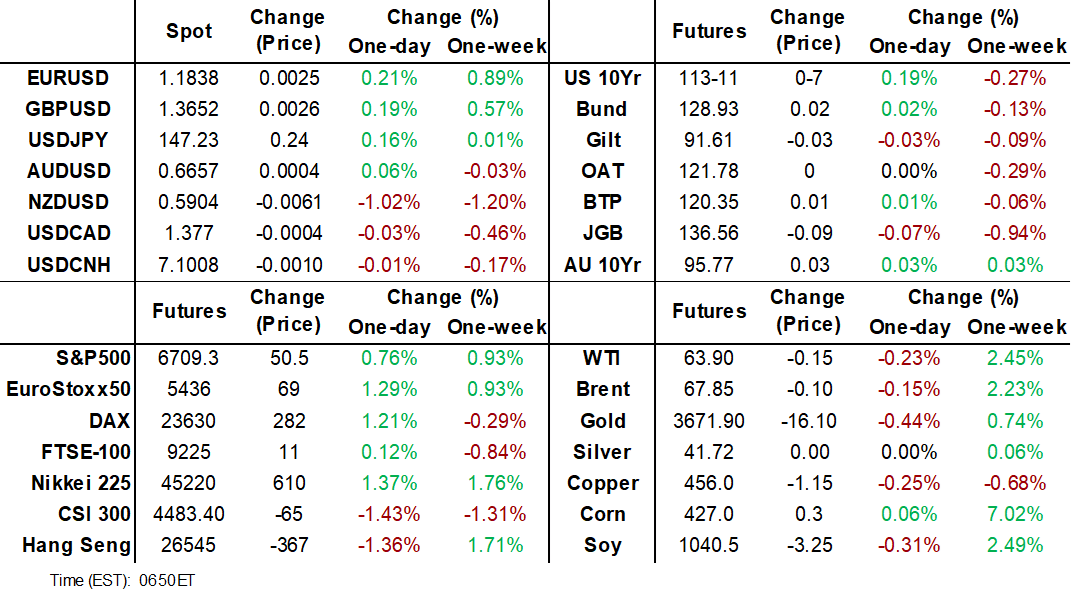

US TSYS: Post-Powell Losses Pared, Jobless Claims & Trump-Starmer Presser Ahead

- Treasuries have pared around half of yesterday’s sell-off, which had on balance continued after Fed Chair Powell’s press conference following after an initially sharp dovish reaction to the SEP.

- Jobless claims headline the data docket, with last week’s Texas-driven spike since linked at least partly to ID fraud, whilst President Trump has a press conference with UK PM Starmer at 0920ET on the final day of his trip.

- Cash yields are 3-4bp lower on the day with the front end lagging slightly.

- 10Y yields are at 4.049% (-3.8bps) having yesterday briefly cleared 4.00% for the first time since Sep 11 and before that early April around reciprocal tariff announcements.

- TYZ5 has lifted to 113-10+ (+06+) off an overnight low of 113-00, on limited cumulative volumes of 285k considering it will include Asian and European reflection of Fed communications.

- Yesterday saw a fleeting high of 113-25+ on the initial dovish reaction to the dot plot although it didn’t trouble resistance at cycle highs of 113-29 (Sep 11 high). The overnight low of 113-00 did however come close to support at 112-28 (20-day EMA) after which lies 112-05+ (50-day EMA).

- Data: Weekly jobless claims (0830ET), Philly Fed mfg Sep (0830ET), Leading index Aug (1000ET), TIC Flows Jul (1600ET)

- Fedspeak: Media blackout remains until Friday 0001ET

- Coupon issuance: US Tsy $19B 10Y TIPS auction (1300ET)

- Bill issuance: US Tsy $100B 4W & $85B 8W bill auctions (1130ET)

- Politics: Trump in Business Leaders Reception with UK PM Starmer (0745ET), Trump-Starmer press conference (0920ET), Trump departs UK en route to White House (1205ET)

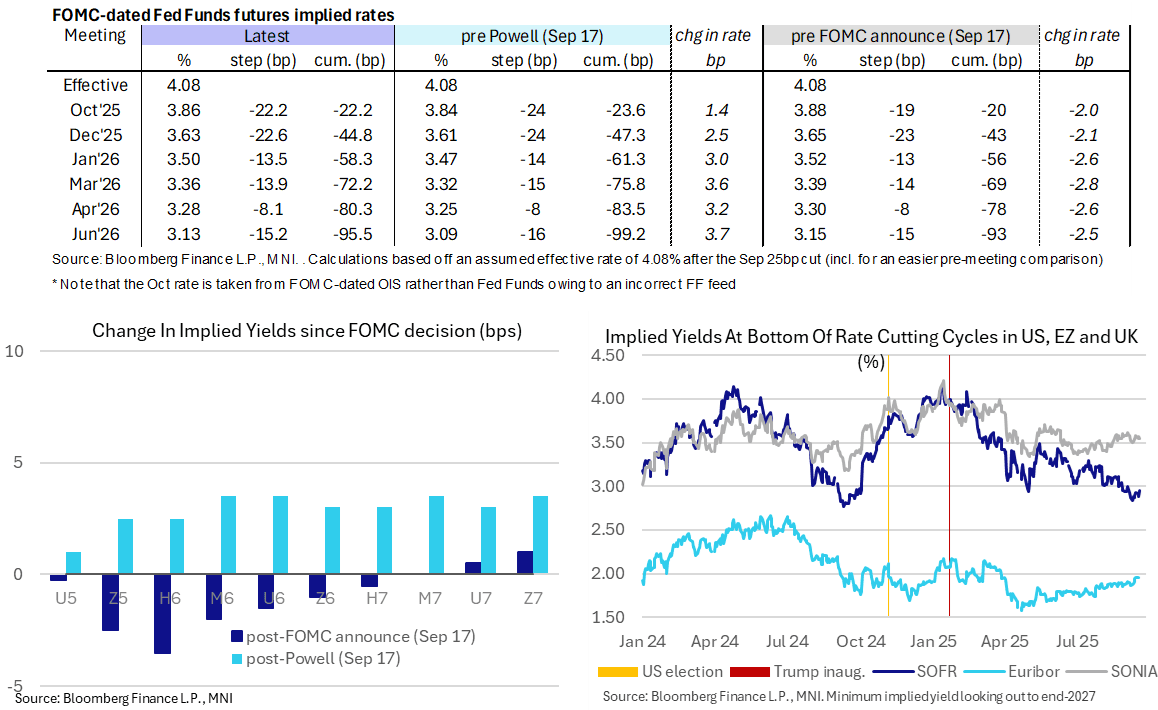

STIR: Fed Rate Path Only Marginally Lower Than Pre-FOMC Levels

- Fed Funds implied rates are up 0.5-2.5bp lower overnight looking out to the next six meetings, leaving rates only 2-2.5bp lower compared to levels shortly before yesterday’s FOMC decision.

- The lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. Despite a lower rate path signalled in the new Dot Plot (which was mostly as expected by analysts), a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

- Cumulative cuts from 4.33% effective: 22bp Oct, 45bp Dec, 58.5bp Jan, 72bp Mar, 80.5bp Apr and 95.5bp Jun.

- SOFR futures are 0.5-2.5 ticks higher on the day looking out to end 2027.

- The SOFR implied terminal yield of 2.925% (SFRH7) is 2.5bp lower on the day for just 0.5bp lower since the FOMC announcement (and 3bp higher since Powell look to the podium).

- Today sees data focus on weekly jobless claims after last week’s Texas driven spike has since been linked at least partly to ID fraud.

- MNI Fed Review: https://media.marketnews.com/Fed_Review_SEP_2025_7605364ee6.pdf

US TSY FUTURES: Net Short Setting Most Prominent On Wednesday

OI data points to a mix of net short setting (TU, UXY, US & WN) and long cover (FV & TY) as contracts ultimately settled lower on Wednesday, in the wake of the latest FOMC decision.

- There was a bias towards net short setting in curve-wide terms.

- Volatile, two-way trade surrounding the FOMC decision and Fed Chair Powell's comments seemed to make for fairly low-committal trade.

| 17-Sep-25 | 16-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,492,826 | 4,486,589 | +6,237 | +215,962 |

FV | 6,749,635 | 6,756,177 | -6,542 | -290,626 |

TY | 5,399,881 | 5,408,626 | -8,745 | -577,036 |

UXY | 2,373,592 | 2,373,575 | +17 | +1,505 |

US | 1,831,772 | 1,823,229 | +8,543 | +1,228,249 |

WN | 2,027,194 | 2,018,560 | +8,634 | +1,638,985 |

|

| Total | +8,144 | +2,217,040 |

SOFR: Mix Of Positioning Swings In Futures On Wednesday

OI data points to mixed positioning moves in the DOFR whites on Wednesday, with net long setting (SFRU5) and net short setting (SFRH6 & M6) seen before a mix of net long cover and short setting came to fore through in the reds through blues.

| 17-Sep-25 | 16-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,481,236 | 1,473,552 | +7,684 | Whites | +49,970 |

SFRZ5 | 1,681,573 | 1,676,521 | +5,052 | Reds | -16,082 |

SFRH6 | 1,201,505 | 1,199,302 | +2,203 | Greens | -34,090 |

SFRM6 | 1,040,647 | 1,005,616 | +35,031 | Blues | -4,417 |

SFRU6 | 960,896 | 953,801 | +7,095 |

|

|

SFRZ6 | 1,025,715 | 1,036,932 | -11,217 |

|

|

SFRH7 | 753,128 | 758,116 | -4,988 |

|

|

SFRM7 | 816,132 | 823,104 | -6,972 |

|

|

SFRU7 | 670,627 | 686,603 | -15,976 |

|

|

SFRZ7 | 698,958 | 703,149 | -4,191 |

|

|

SFRH8 | 439,206 | 443,895 | -4,689 |

|

|

SFRM8 | 355,936 | 365,170 | -9,234 |

|

|

SFRU8 | 271,976 | 281,896 | -9,920 |

|

|

SFRZ8 | 289,175 | 284,826 | +4,349 |

|

|

SFRH9 | 186,814 | 184,107 | +2,707 |

|

|

SFRM9 | 178,341 | 179,894 | -1,553 |

|

|

EUROPEAN ISSUANCE UPDATE

German DFA Q4 issuance plan: E10.5bln more bonds:

- Bond issuance increased by E10.5bln (smaller than the E12-13bln we expected and below the E15bln of Q3). Bubill issuance to increase E4.5bln (versus E4.0bln in Q3).

- Schatz: E2.5bln higher issuance (we had pencilled in E2.0bln): The launch auction of the new Dec-27 Schatz will be increased by E0.5bln to E5.5bln, the two Schatz taps then increased by E1.0bln each to E5.0bln and E4.5bln respectively (the taps we had expected).

- Bobl: Extra E0.5bln for the November auction - we had not anticipated this thinking there would be two 7-year Bund auctions.

- 7-year Bund: We saw the smaller E3.0bln auction size we expected, but there will only be one auction rather than the two we expected. This will be on 22 October.

- 10-year Bund auctions taps increased by E0.5bln each to E5.0bln and E4.5bln respectively (we had expected both to increase to E5.0bln).

- 15-year Bund: A second auction added to the quarter (as we expected). The existing single ISIN auction of E1.5bln has been replaced with a multi-ISIN E2.0bln auction while the additional auction is also a E2.0bln multi-ISIN auction.

- 30-year Bund: The October and November multi-ISIN auctions will both be increased by E0.5bln to E2.5bln (we hadn't expected this).

- 11-month Bubill auctions of E1.5bln each have been added to each month of Q4 (bringing total bubill increase to E4.5bln - slightly above the E4.0bln we pencilled in).

German 15/30-year Q4 auction schedule:

- 8 October: 15-year: E1bln of the 2.60% May-41 Bund (ISIN: DE000BU2F009) alongside E1.0bln of another Bund.

- 15 October: 30-year: E1.5bln of the 2.90% Aug-56 Bund (ISIN: DE000BU2D012) alongside E1.0bln of another Bund.

- 5 November 15-year: E1bln of the 2.60% May-41 Bund (ISIN: DE000BU2F009) alongside E1.0bln of another Bund.

- 12 October: 30-year: E1.5bln of the 2.90% Aug-56 Bund (ISIN: DE000BU2D012) alongside E1.0bln of another Bund.

Spain auction results:

- E2.08bln of the 2.40% May-28 Bono. Avg yield 2.212% (bid-to-cover 1.91x).

- E1.976bln of the 3.20% Oct-35 Obli. Avg yield 3.23% (bid-to-cover 1.93x).

- E1.38bln of the 4.00% Oct-54 Obli. Avg yield 4.074% (bid-to-cover 1.98x).

France MT auction results:

- E2.105bln of the 0.75% May-28 OAT. Avg yield 2.26% (bid-to-cover 3.56x).

- E2.871bln of the 2.40% Sep-28 OAT. Avg yield 2.34% (bid-to-cover 4.01x).

- E4.428bln of the 2.70% Feb-31 OAT. Avg yield 2.79% (bid-to-cover 2.84x).

- E2.096bln of the 3.50% Nov-33 OAT. Avg yield 3.22% (bid-to-cover 3.91x).

France IL auction results:

- E641mln of the 0.60% Jul-34 OATei. Avg yield 1.37% (bid-to-cover 3.44x).

- E448mln of the 0.10% Jul-38 Green OATei. Avg yield 1.7% (bid-to-cover 3.81x).

- E246mln of the 0.55% Mar-39 OATi. Avg yield 1.85% (bid-to-cover 4.68x).

FOREX: NZD Weakness Extends Following Particularly Soft Q2 GDP

The lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. This prompted the USD’s bearish momentum to stall on Wednesday and aggressively reverse higher. This theme was also on display early Thursday, with the USD index briefly extending its recovery from fresh cycle lows to 1.15% before easing back to unchanged levels on the session.

- The New Zealand dollar is the standout in the G10 space, following a particular weak set of Q2 GDP data. The -0.6% annual read has weighed heavily on the Kiwi, currently down 1.05% against the dollar and testing back below 0.5900. The data trumped the weaker-than-expected Aug employment change figure out of Australia, which has notably seen AUDNZD rise above 1.12 for the first time since late 2022. The cross has extended to its next target of 1.1250 in recent trade, the 76.4% Fibonacci retracement of the 2022 price swing.

- USDJPY tracks 0.3% higher on Thursday, extending the strong bounce following the FOMC. Notably for the pair, yesterday is a hammer candle formation - a bullish reversal signal. If correct, it signals scope for a recovery, with pivot support now established at 145.49, Wednesday’s low.

- Strong performance for equities has supported a significant move higher for EURJPY, breaking above key resistance at 173.97 and rising to a high of 174.31. The break higher opens 174.86, a Fibonacci projection, and 175.43, the Jul 11 ‘24 high and a key medium-term resistance.

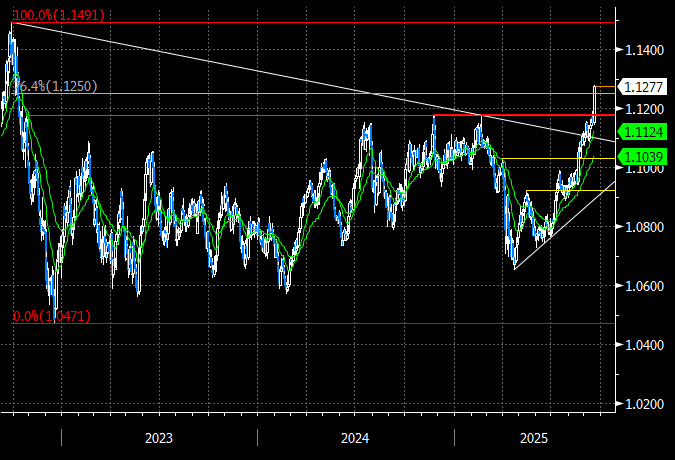

- Support for the single currency has seen EURUSD bounce around 50 pips from the overnight 1.1781 lows. As a reminder, spot traded at fresh multi-year highs following the fed decision, printing 1.1919 and trading to within 4 pips of touted resistance. Support to watch is the 50-day EMA, at 1.1659.

- The September Bank of England decision headlines Thursday’s event risk, while the August US leading index, September Philly Fed and jobless claims data are all scheduled.

FOREX OPTIONS: Expiries for Sep18 NY cut 10000ET (Source: DTCC)

- EURUSD: 1.1800 (2.51bn), 1.1806 (211mnl), 1.1850 (787mln), 1.1900 (2.1bn)

- EURGBP: 0.8675 (404mln), 0.8690 (249mln)

- USDJPY: 146.60 (535mln), 146.75 (386mln), 147.00 (290mln), 147.20 (503mln), 147.22 (400mln), 147.25 (334mln), 147.30 (210mln), 147.40 (265mln)

- USDCAD: 1.3790 (228mln), 1.3800 (331mln)

- AUDUSD: 0.6600 (1.08bn), 0.6615 (308mln), 0.6650 (725mln), 0.6660 (580mln)

- NZDUSD: 0.5935 (738mln), 0.5940 (261mln)

FOREX: AUDNZD Extends Intra-Day Gains to 1.1%

- The New Zealand dollar is the standout underperformer in the G10 space, following a particular weak set of Q2 GDP data. The much weaker-than-expected data has weighed heavily on the Kiwi, currently down 1.05% against the dollar having tested back below 0.5900.

- The NZ data trumped the weaker-than-expected August employment change figure out of Australia, which has notably allowed AUDNZD to extend its impressive rally from the April lows to 5.88%.

- Price action today has seen the cross rise above 1.12 for the first time since late 2022 and steady appreciation has now seen spot eclipse the next target for the move of 1.1250, the 76.4% Fibonacci retracement of the 2022 price swing. Above here, resistance appears scant until the 2022 highs, located at 1.1491.

- Both the production and expenditure-based NZ GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. However, with two votes for a 50bp cut in August, the risk of a larger move before year end is material.

EQUITIES: Fresh S&P E-Minis Cycle High

A bull cycle in S&P E-Minis remains intact and the contract has today resumed its uptrend. Price has traded through the 6700.00 handle and this signals scope for an extension towards 6748.50, a 1.236 projection of the Aug 1 - 15 - 20 price swing. Initial support to watch lies at 6578.36, the 20-day EMA.

- EUROSTOXX 50 futures recently traded through resistance around the 20-day EMA - a bullish development for now. The move higher undermines a recent bearish theme and signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support has been defined at 5302.00, the Sep 2 low.

| Date | GMT/Local | Impact | Country | Event |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS | |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly |