FOREX: AUDNZD Extends Intra-Day Gains to 1.1%

Sep-18 10:46

- The New Zealand dollar is the standout underperformer in the G10 space, following a particular weak set of Q2 GDP data. The much weaker-than-expected data has weighed heavily on the Kiwi, currently down 1.05% against the dollar having tested back below 0.5900.

- The NZ data trumped the weaker-than-expected August employment change figure out of Australia, which has notably allowed AUDNZD to extend its impressive rally from the April lows to 5.88%.

- Price action today has seen the cross rise above 1.12 for the first time since late 2022 and steady appreciation has now seen spot eclipse the next target for the move of 1.1250, the 76.4% Fibonacci retracement of the 2022 price swing. Above here, resistance appears scant until the 2022 highs, located at 1.1491.

- Both the production and expenditure-based NZ GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. However, with two votes for a 50bp cut in August, the risk of a larger move before year end is material.{AU}{NZ}FX: AUDNZD Extends Intra-Day Gains to 1.1%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Aug19 NY cut 1000ET (Source DTCC)

Aug-19 10:32

- EUR/USD: $1.1600(E731mln), $1.1620-25(E2.3bln), $1.1650-65(E682mln), $1.1700(E1.3bln)

- USD/JPY: Y148.30-35($709mln)

- AUD/USD: $0.6515(A$745mln)

- USD/CAD: C$1.3750-70($646mln)

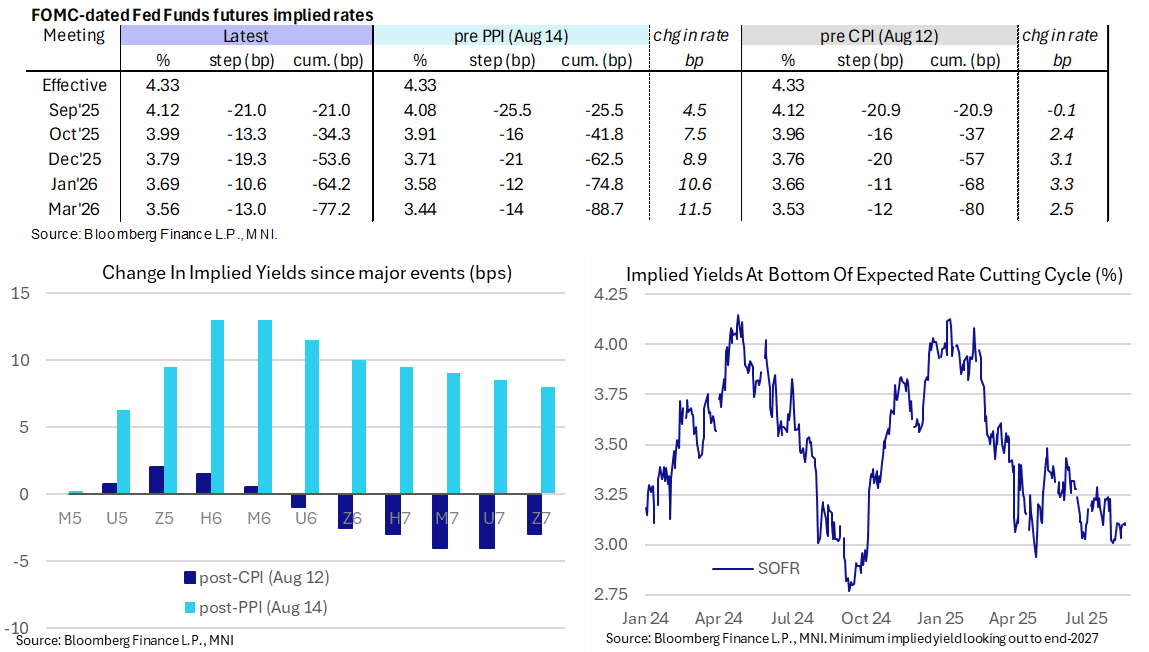

STIR: Sept Fed Cut Still No Longer Fully Locked In, A Dovish Bowman Ahead

Aug-19 10:32

- Fed Funds implied rates are unchanged on the day, with 21bp of cuts priced for next month’s FOMC meeting.

- Cumulative cuts from 4.33% effective: 21bp Sep, 34.5bp Oct, 53.5bp Dec, 64bp Jan and 77bp Mar.

- The SOFR implied terminal yield of 3.11% (SFRH7) is essentially unchanged from the past two closes, holding the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Fed VC Supervision Bowman (permanent voter, dove) speaks on Bloomberg TV at 1000ET before at a Blockchain Symposium at 1410ET (text only), with greater scope for market moving comments at the former. We suspect it might be hard to generate a dovish reaction though unless she canvasses larger cuts, something other FOMC colleagues have pushed back on.

- These will be her first remarks since last week’s mixed inflation data. She said on Aug 9 that she favors three cuts this year (unsurprising having dissented in July) and saw recent labor data as reinforcing this view.

- Tomorrow then sees the FOMC minutes before Powell’s Jackson Hole address on Friday. However, when it comes to Sept cut prospects, the August payrolls and CPI releases plus QCEW details (for preliminary payroll benchmark revision estimates) are all still to come before the next FOMC decision on Sep 17.

ESM ISSUANCE: 6-month ESM-Bill

Aug-19 10:32

| Type | 6-month bills |

| Maturity | Feb 19, 2026 |

| Amount | E1.082bln |

| Target | E1.1bln |

| Previous | E1.089bln |

| Avg yield | 1.947% |

| Previous | 1.923% |

| Bid-to-cover | 2.64x |

| Previous | 2.41x |

| Previous date | Jul 15, 2025 |